Chains of Gold

Why Remonetising Gold is a Recipe for Economic Suicide

A Graphic Novella

The allure of the gold standard is persistent. In times of fiscal uncertainty, inflationary spikes, or geopolitical tension, a vocal minority argues that the only path to monetary honesty is to re‑anchor our currencies to a physical commodity. The promise is seductive: a money supply immune to political manipulation, disciplined by geology rather than the whims of central bankers.

This view is not merely nostalgic; it is dangerously anachronistic. A rigorous analysis of macroeconomic history, constitutional jurisprudence, and operational reality demonstrates that a return to gold would not bring stability. It would import commodity volatility into the price system, necessitate state confiscation of private assets, and guarantee severe deflationary depressions. The gold standard is not a shield against state power; it is a mechanism that ensures state power will be used more brutally when the system inevitably fractures.

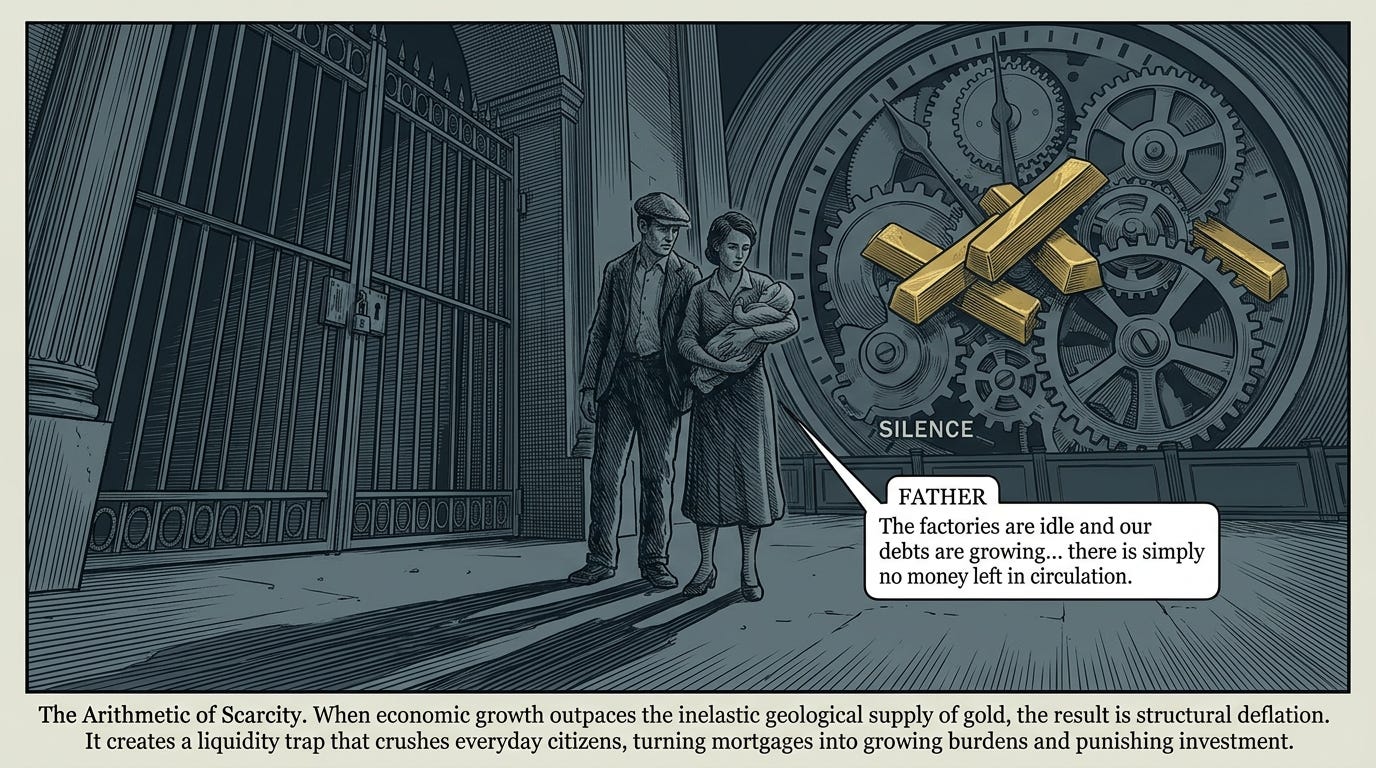

The Arithmetic of Scarcity

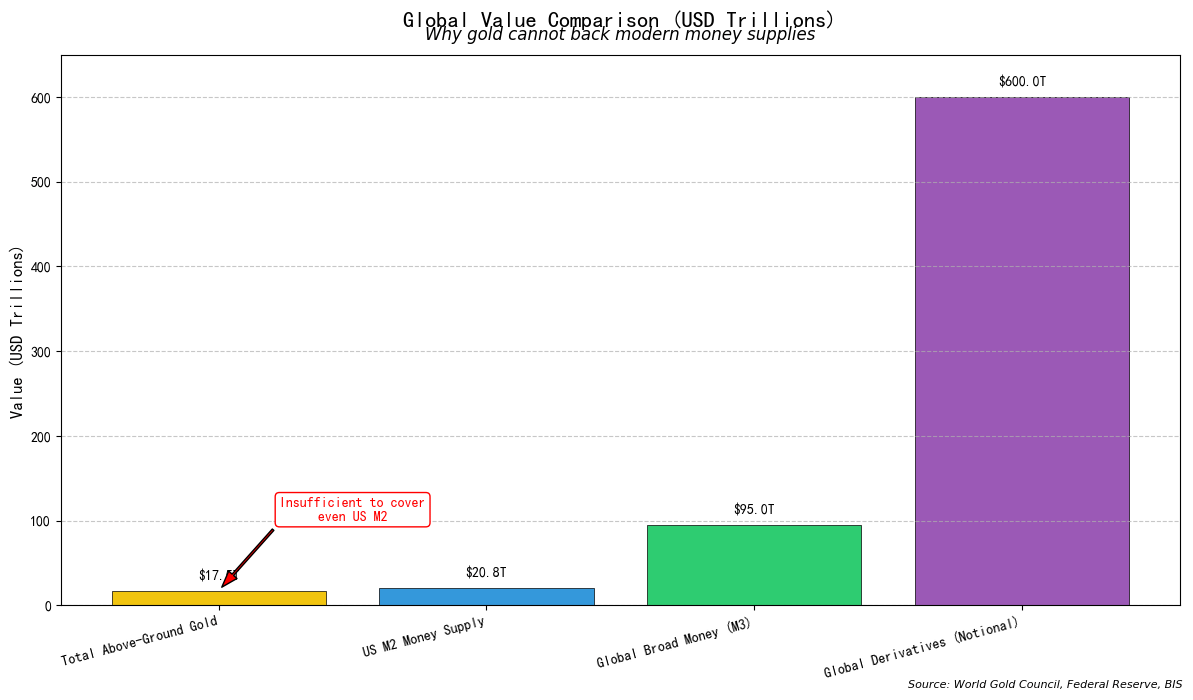

The primary failure of gold as a modern monetary base is simple arithmetic. The total above‑ground stock of gold is estimated at approximately 219,891 tonnes.¹ At current market prices, this represents a global value of roughly $17–18 trillion.² While this sounds substantial, it is negligible compared to the scale of the modern global economy. Global GDP exceeds $110 trillion, and daily foreign exchange turnover alone reaches $9.6 trillion – up 28% from the previous survey in 2022.³

To back even a fraction of today’s broad money supply with gold would require a massive revaluation of the metal – potentially to $10,000 or $20,000 per ounce. Such a revaluation would not occur smoothly. It would trigger violent deflation, wiping out nominal asset prices and increasing the real burden of debt. For every debtor – from homeowners to governments – their obligations would become exponentially harder to repay in real terms. This would be catastrophic.

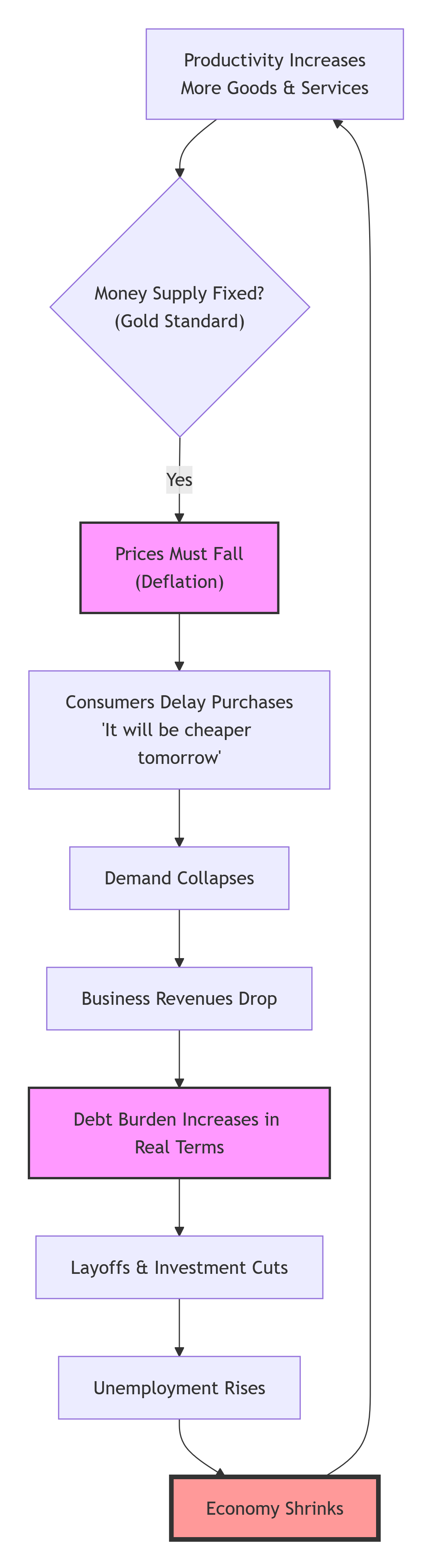

Furthermore, gold supply is highly inelastic. New mines take 10–20 years to develop. Output does not respond to price signals in the short term. If the global economy grows by 3% but gold mining grows by 1%, the result is structural deflation. Prices must fall to match the scarce money supply. This sounds beneficial for consumers, but it crushes economic activity. Why invest in a business if the money you earn next year will be worth more than today? Why borrow to build a home if the mortgage becomes harder to pay every month? This dynamic creates a liquidity trap from which there is no escape without abandoning the standard.

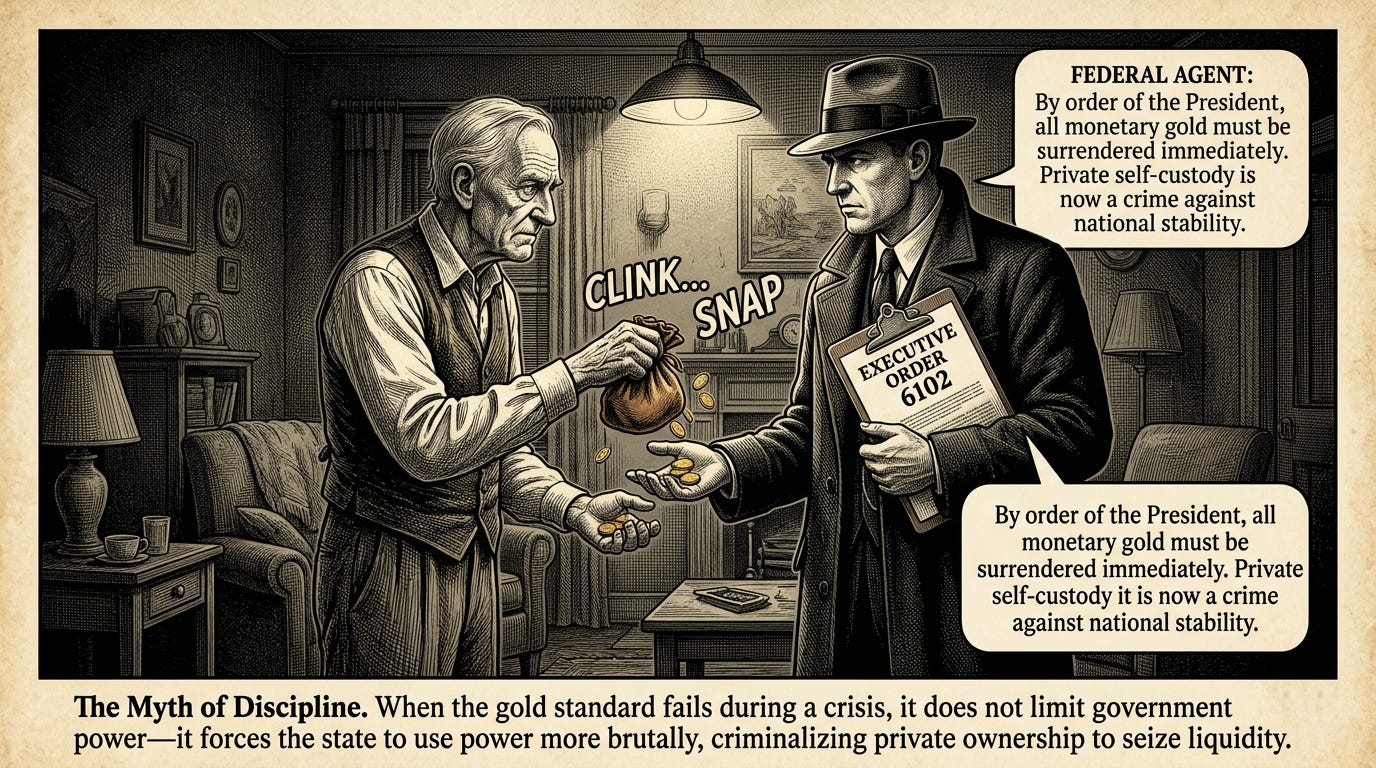

The Myth of Discipline and the Reality of Confiscation

Proponents argue that gold disciplines governments by preventing excessive spending. History suggests the opposite: it disciplines populations by forcing governments to seize private wealth when the system fails.

Under a true gold standard, the government cannot expand the money supply during a crisis without acquiring more gold. In a severe recession or war, private hoarding of gold exacerbates deflation, starving the economy of liquidity. The state’s logical response is confiscation. This is not speculation; it is precedent. In 1933, President Franklin D. Roosevelt issued Executive Order 6102, criminalising the private ownership of monetary gold and forcing citizens to sell their holdings to the Federal Reserve at $20.67 per ounce.⁴

Shortly after, the government revalued gold to $35 per ounce, effectively devaluing the dollar and confiscating 70% of the value of private gold holdings.⁵

The Supreme Court upheld this action in Norman v. Baltimore & Ohio Railroad Co. (1935), ruling that Congress has plenary power over the value of money.⁶ If gold were remonetised today, the same legal logic would apply. Private hoarding would be seen as a threat to national monetary stability. In an era of digital surveillance, where large transactions are reported and bank holdings are transparent, confiscation would be instantaneous and comprehensive. The gold bug’s dream of self‑custody would vanish overnight. You would not be holding gold; you would be holding a liability that the state needs to consolidate.

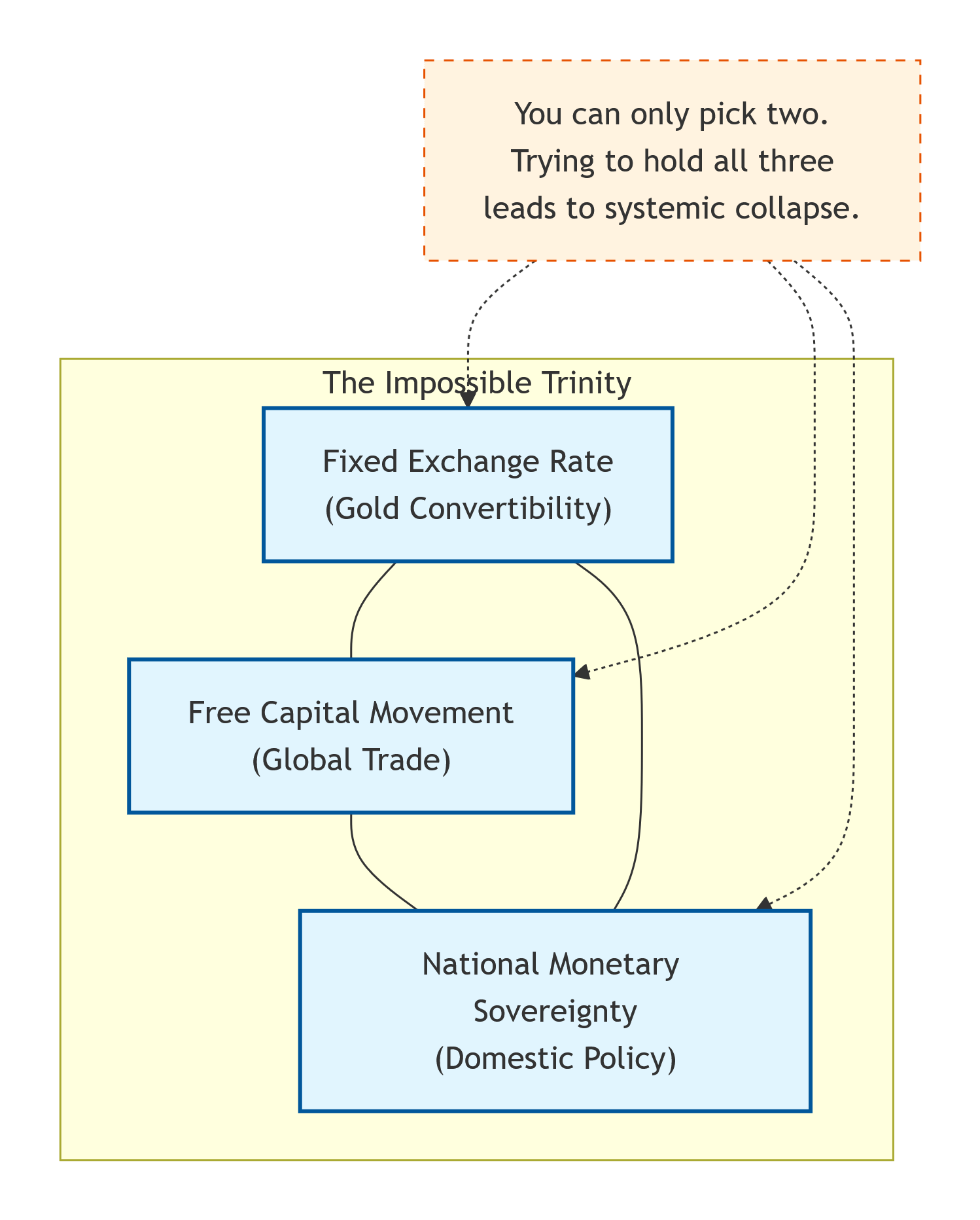

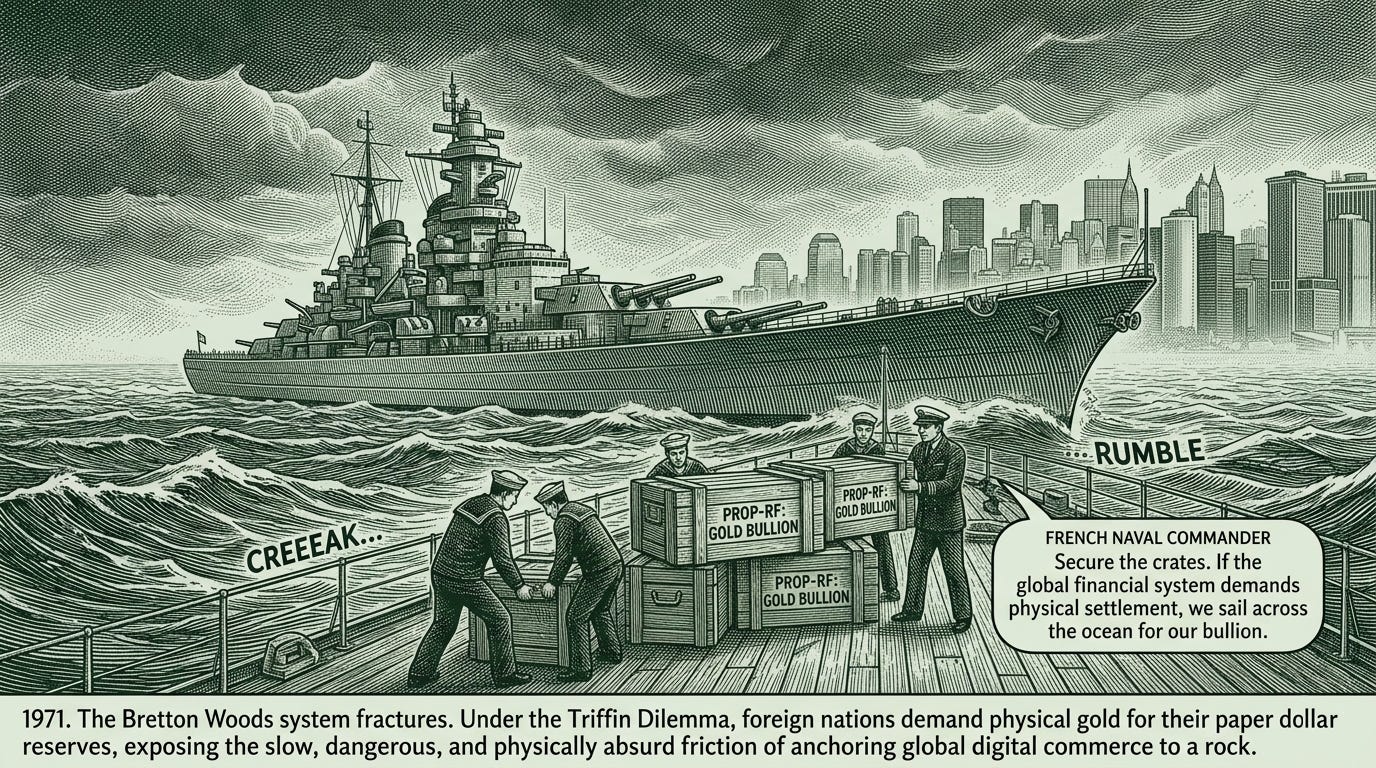

The Triffin Dilemma and International Instability

On the global stage, a gold standard is mathematically insoluble due to the Triffin Dilemma. Identified by economist Robert Triffin in 1960, this paradox states that the country issuing the world’s reserve currency must run trade deficits to provide liquidity for global commerce. However, under a gold standard, those deficits lead to an outflow of gold reserves. As foreign holdings of the currency exceed the issuer’s gold stock, confidence collapses, leading to a run on the gold.⁷

This is precisely what destroyed the Bretton Woods system in 1971. When France and other nations demanded physical gold for their dollar reserves, President Nixon closed the gold window.

The world did not end; instead, it moved to a flexible fiat system that has supported unprecedented global growth.

Moreover, gold settlement is physically absurd in a digital age. The idea that trade imbalances should be settled by shipping bullion across oceans is a relic of the 19th century. It is slow, expensive, and geopolitically risky. During the Cold War, the mere threat of gold shipments influenced diplomatic relations. Today, with supply chains just‑in‑time and finance instant, anchoring trade to physical metal introduces unacceptable friction and risk.

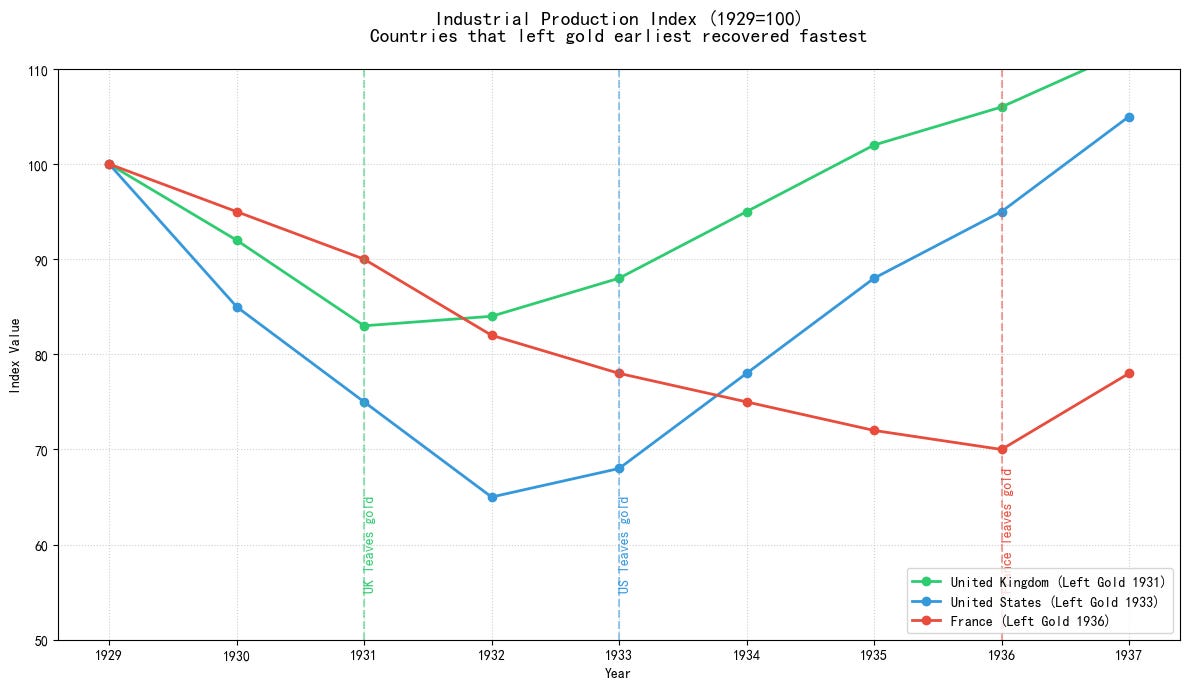

Historical Failure: The “Golden Fetters”

The empirical record of the gold standard is one of repeated failure. Economic historians Barry Eichengreen and Peter Temin have demonstrated that countries that abandoned gold earliest during the Great Depression recovered fastest. Britain left gold in 1931 and began to recover. The United States, which clung to it until 1933, suffered deeper and longer stagnation. France, which remained on gold until 1936, experienced prolonged economic misery.⁸

The interwar gold standard also poisoned international relations. It forced countries to engage in competitive devaluations and trade wars as they struggled to maintain convertibility. It created currency blocs that fragmented global trade. No major economy has returned to a gold standard since 1971 – not even Switzerland, which abolished its last constitutional link to gold in 1999.⁹

The MMT Perspective: Sovereignty vs. Servitude

From a Modern Monetary Theory (MMT) perspective, the gold standard is a voluntary surrender of national sovereignty. A government that issues its own fiat currency is not financially constrained in the same way a household is. It does not need to “find” money to spend; it creates money by spending. The real constraint is not gold, but real resources: labour, energy, materials, and technology.

Inflation occurs when demand exceeds these real productive capacities, not when the money supply grows. Fiat money allows policymakers to target full employment and price stability by adjusting fiscal and monetary policy. Gold targets neither. It ties the hands of government, preventing it from responding to crises. It forces internal devaluation (cutting wages and prices) instead of allowing exchange rate adjustments. This is socially devastating and politically unstable, as seen in the Eurozone crisis, which operated as a quasi‑gold standard for peripheral nations like Greece.

A Note from Milton Friedman

Nobel laureate Milton Friedman, often celebrated by free‑market advocates, was notably sceptical of a pure gold standard. In his 1982 article “Monetary Policy: Theory and Practice,” he wrote that “if a domestic money consists of a commodity, a pure gold standard or cowrie bead standard, the principles of monetary policy are very simple. There aren’t any. The commodity money takes care of itself.”¹⁰

More systematically, in Capitalism and Freedom (1962), Friedman concluded that “an automatic commodity standard is neither a feasible nor a desirable solution to the problem of establishing monetary arrangements for a free society.” He offered two reasons: “It is not desirable because it would involve a large cost in the form of resources used to produce the monetary commodity. It is not feasible because the mythology and beliefs required to make it effective do not exist.”¹¹

Friedman estimated that all the efforts associated with mining and processing gold would amount to, on average, 2.5% of GDP – today, hundreds of billions of dollars annually.¹² Moreover, he argued that the gold standard produced “long term relative stability in prices at the cost of a great deal of short term instability.”¹³ For a thinker devoted to economic freedom, the gold standard’s short‑term volatility was a decisive liability.

Be Careful What You Wish For

To those who argue that gold brings honesty, consider the alternative. Gold does not eliminate state power; it redirects it. It shifts power from democratic institutions to gold miners, foreign governments, and those lucky enough to hold the metal before confiscation. It replaces the flexibility of fiat with the rigidity of geology.

The next banking panic under a gold standard would be horrific. With no lender of last resort capable of creating liquidity, banks would fail en masse. Depositors would find their “gold certificates” worthless as the system froze. The government would declare a bank holiday, seize private gold, and revalue the currency, leaving most citizens with nothing.

Gold is not money. It is a commodity with industrial and aesthetic uses. Its value as a monetary anchor is a historical artefact, not an economic necessity. In the 21st century, we have the tools to manage money responsibly. We do not need to chain ourselves to a rock dug from the ground.

References

World Gold Council. “Gold Demand Trends Q4 2023.” Total above-ground stocks estimated at ~212,582 tonnes (end-2023), rising to ~219,891 tonnes in subsequent updates.

World Gold Council. “Gold Valuation Calculator.” Based on ~$2,300–$2,400/oz pricing.

Bank for International Settlements (BIS). “Triennial Central Bank Survey 2025.” Daily FX turnover reached $9.6 trillion.

National Archives. “Executive Order 6102.” April 5, 1933.

Federal Reserve History. “The Gold Reserve Act of 1934.” Revaluation from $20.67 to $35/oz.

Cornell Law School, Legal Information Institute. Norman v. Baltimore & Ohio Railroad Co., 294 U.S. 240 (1935).

International Monetary Fund (IMF). “Robert Triffin’s Testimony to Congress, 1960.”

Eichengreen, Barry. Golden Fetters: The Gold Standard and the Great Depression, 1919–1939. Oxford University Press, 1992. See also NBER Working Paper No. 3994.

Swiss National Bank. “The End of the Gold Clause in the Swiss Constitution.” 1999.

Friedman, Milton. “Monetary Policy: Theory and Practice.” Journal of Money, Credit and Banking, Vol. 14, No. 1 (1982), pp. 98–118.

Friedman, Milton. Capitalism and Freedom. University of Chicago Press, 1962, Chapter 6.

Friedman, Milton. “The Resource Cost of Irredeemable Paper Money.” Journal of Political Economy, Vol. 80, No. 3 (1972).

Friedman, Milton. A Program for Monetary Stability. Fordham University Press, 1960.

Steve Keen's Ravel software can model how debt deflation is an inevitable outcome in an economy with a fixed money supply, see chapter 3 of his excellent book "Money and Macroeconomics from First Principles" for a demonstration.

Note a key difference to look at is government “base money” vs bank liabilities- usually in the past a muddle on redeemability and these