From Monetary Muddle to Monetary Mystique

Taxonomy of a Conceptual Inheritance

A Graphic Novella

The analytical distinction between government-issued base money and privately created bank liabilities is one of the most neglected fault lines in monetary economics. When the distinction collapses in public understanding, it gives rise to what might be termed a monetary muddle — a conceptual fog in which causal relationships are misattributed, historical lessons are misread and policy myths acquire durable traction. This article traces the muddle from its historical origins in commodity-based monetary systems, through its role in recurrent financial panics under the gold standard, to its modern manifestations in two prominent economic misconceptions: the reductionist reading of the 97 per cent money-creation figure and the persistent belief that government spending is numerically constrained by prior tax revenue. Then I’ll argue that the persistence of such muddles is not merely accidental. A substantial body of literature documents a monetary mystique — a deliberate or structurally inherited culture of opacity surrounding central banking that impedes public accountability while affording political insulation. This essay concludes by considering whether greater conceptual transparency is feasible without destabilising the functional independence that central banking requires.

The Analytical Distinction and Its Historical Obscurity

At the most elementary level of monetary analysis, two qualitatively different categories of money can be identified. The first — variously termed base money, outside money, or high-powered money — consists of liabilities of the central bank: currency in circulation and commercial bank reserves held at the central bank. The second — broad money, inside money, or simply bank deposits — consists of liabilities of commercial banks to their depositors.

The difference is not quantitative but qualitative. Outside money represents a net financial asset for the private sector as a whole: no private agent owes an offsetting liability. Inside money, by contrast, is simultaneously an asset for one private agent (the depositor) and a liability for another (the bank). Its value depends on the credibility of the bank’s promise to convert it on demand into outside money — which, in a fiat system, means into central bank reserves or currency.

The historical record of gold-based monetary systems reveals that this distinction was never consistently maintained in institutional practice, nor clearly grasped by the public. In a representative gold standard, the pyramid of monetary instruments comprised several layers: gold coin (outside money, redeemable only into itself); gold-convertible banknotes issued by the central bank or treasury (outside money insofar as government-guaranteed, but historically ambiguous); and bank deposits (private inside money, theoretically convertible into coin or notes). The “muddle on redeemability” to which the opening comment refers was the persistent public and institutional confusion about which layers were convertible into which — and under what conditions.

This ambiguity was not an accidental design flaw but a structural feature. As economic historian Barry Eichengreen argued in his seminal work, the gold standard of the 1920s “was the mechanism transmitting the destabilisation from the USA to the rest of the world” and “set the stage for the Depression of the 1930s by heightening the fragility of the international financial system” Eichengreen, B. (1992). Eichengreen’s metaphor of “golden fetters” captures precisely the self-defeating rigidity of a system whose ostensible anchor — physical gold — introduced rather than resolved the problem of convertibility confidence.

The Muddle in Motion

Panics, Central Banking, and Divergent National Experiences

The conceptual muddle had concrete, devastating institutional consequences. Under the classical gold standard, the lack of a clear functional separation between government base money and private bank liabilities converted local bank distress into systemic panics with alarming regularity.

In the United States, the National Banking Era (1863–1913) witnessed a parade of severe financial crises. Contemporary observers and subsequent scholars have identified major panics in 1873, 1884, 1890, 1893, and 1907. The structural vulnerabilities were well understood at the time. As later summarised by economic historian Elmus Wicker, the conventional wisdom held that “an inelastic stock of paper currency coupled with the pyramiding of the nation’s ultimate banking reserve in New York made the central money market especially vulnerable to external shocks” Wicker, E. (2006). The National Monetary Commission’s commissioned history, O. M. W. Sprague’s History of Crises under the National Banking System (1910), remains a landmark documentation of this pattern.

The economic toll was severe. The panic of 1893 triggered bank runs and 400 bank failures in six months, precipitating the worst depression the United States had seen to that point. The panic of 1907 was so acute that the government turned to private banker J. P. Morgan to orchestrate a rescue — an episode widely understood as the proximate impetus for the creation of the Federal Reserve in 1913.

The United Kingdom presented a markedly different trajectory — not because it lacked the underlying conceptual muddle, but because it developed an institutional remedy. The decisive turning point came with the panic of 1866, triggered by the failure of Overend, Gurney & Company, one of the largest bill brokers in the City of London. Observers described an “earthquake” tearing through London as a massive bank run spread. Some two hundred banks and companies collapsed.

In the aftermath of 1866, the Bank of England — not yet formally a central bank in the modern sense, and still a private joint-stock company with a public charter — began adopting the practices that would become known as lender-of-last-resort operations. The canonical formulation came from Walter Bagehot in his 1873 treatise Lombard Street. Bagehot’s dictum, subsequently summarised by Charles Goodhart, is deceptively simple: lend freely, at a high rate of interest, on good banking securities. The logic was that only a lender of last resort could break the self-fulfilling dynamic of a run by credibly offering liquidity against sound collateral.

The critical point for present purposes is that the Bank of England’s evolving lender-of-last-resort function did not eliminate the underlying conceptual muddle. Rather, it substituted institutional authority for conceptual clarity. A sufficiently powerful and credible central bank could stop a panic by acting as the ultimate source of liquidity, even if the public remained confused about the relationship between bank deposits and government base money. In the United States, by contrast, the absence of a central bank meant that no such authority existed to perform this function. The muddle ran its full destructive course.

The Muddle in Modern Guise

Two Persistent Myths

If the historical muddle gave rise to financial panics, its modern legacy is more subtle but no less consequential. Two economic myths, widely circulated in public discourse, derive their plausibility from the same underlying confusion between government base money and bank liabilities.

The 97 Per Cent Figure and the Elision of Reserves

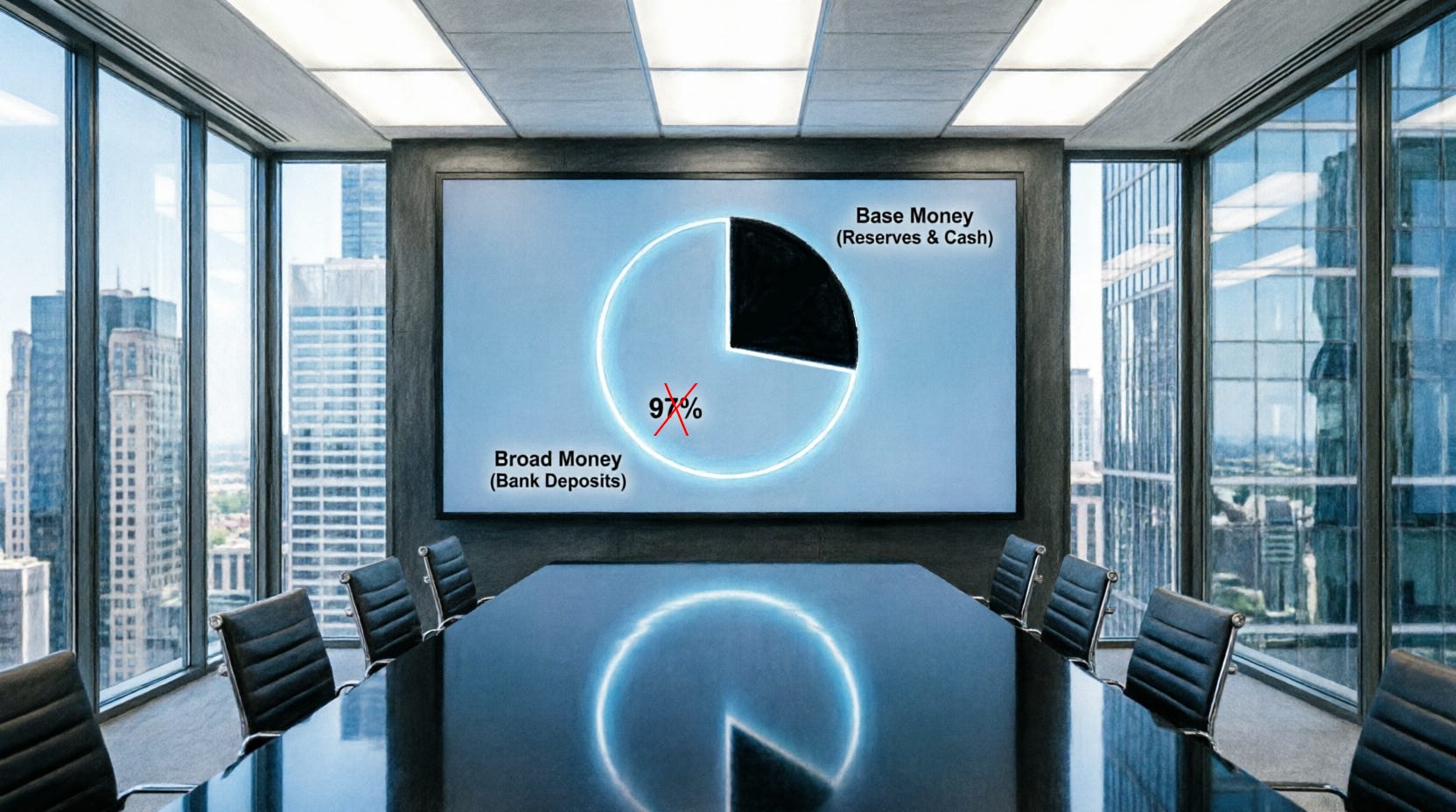

A frequently cited statistic holds that approximately 97 per cent of the money supply in advanced economies is created by commercial banks rather than by the central bank. The Bank of England’s own research has noted that “97% of the money held by the public is in the form of deposits with banks, rather than currency” Bank of England (2014).

This figure is often deployed as evidence that private banks exercise near-total control over monetary conditions, with the state reduced to a peripheral player. However, the interpretation of this statistic often suffers from a critical error. Observers who conclude that banks “create money out of nothing” without constraint fail to recognise the regulatory and capital limits on lending. More importantly, the focus on the 97 per cent distracts from the nature of the remaining 3 per cent.

The conceptual error is twofold. First, it implies a mechanical link between reserves and lending that does not exist in modern fiat systems. As the Bank of England clarified in 2014, banks do not wait for deposits or reserves before making loans; they create deposits when they lend, and then seek reserves afterwards to meet settlement needs. The central bank supplies these reserves elastically to maintain its interest rate target. Therefore, the quantity of reserves does not constrain the creation of broad money; rather, lending is constrained by capital adequacy, risk appetite, and borrower demand.

Second, and more critically, the 97 per cent figure obscures the unique status of the 3 per cent. Base money (reserves and cash) is the only form of money that is a direct liability of the state. By conflating the two, the public fails to see that the state’s spending capacity is not operationally constrained by the stock of broad money, but by real resources. The 97 per cent figure describes the composition of broad money, not the distribution of monetary authority.

Reserves, Gold, and the 97%

A Comparison of Two Anchors

The previous section introduced a balance‑sheet measure – commercial banks’ holdings of reserves plus government bonds – to show that a substantial fraction of broad money (often a third or more) is ultimately state‑backed. This finding runs directly counter to the impression, often drawn from the 97% statistic—that private banks operate almost entirely independently of the state. However, a deeper question remains: how do reserves actually anchor the 97% of bank deposits, and how does that compare to the role that gold once played?

Reserves as the Operational Anchor of Bank Deposits

When a commercial bank creates a new deposit – say, a £200,000 mortgage – it simultaneously creates a new liability to the borrower. That deposit is broad money, part of the 97%. For the borrower to spend that money, the bank must be able to settle payments with other banks. Settlement occurs in central bank reserves, which are a liability of the state. If the borrower writes a cheque to a customer of another bank, the first bank loses reserves to the second bank. Consequently, a bank that creates too many deposits without also acquiring sufficient reserves will find itself unable to meet its settlement obligations.

This is not a trivial technicality. The entire system of private bank money depends on the existence of a sufficient stock of reserves to clear payments. Without reserves, the 97% would be a set of mutually incompatible IOUs that could not be reliably exchanged between banks. In this sense, reserves are not merely a “backing” in a static accounting sense; they are the daily settlement asset that makes the 97% function as a unified means of payment.

The balance‑sheet measure described earlier (reserves + bonds) captures the stock of state liabilities that banks hold as assets. But the functional role of reserves goes beyond the stock: it is the flow of reserves through the real‑time gross settlement system that gives finality to every large‑value payment. A bank deposit that is never used for interbank settlement may never “touch” reserves directly, but its usability depends on the credible promise that it could be converted into reserves if needed.

Gold as a Historical Apex

Similarity and Difference

Before the modern system of fiat reserves, gold played a comparable role as the ultimate settlement asset under the classical gold standard. A bank deposit was a promise to pay gold coin on demand. Interbank settlements were conducted by transferring gold bullion or gold‑backed claims. In that era, the 97% figure would have been even more lopsided: gold coin (the apex) was a tiny fraction of total money, with the vast majority consisting of bank deposits and private banknotes.

In both systems – gold‑backed and reserve‑backed – we see the same hierarchical structure: a narrow base of “outside money” (gold or reserves) supports a wide pyramid of “inside money” (bank deposits). The 97% statistic is not a discovery of the fiat era; it was equally true, in proportionate terms, under the gold standard. What has changed is the nature of the apex.

The critical functional difference lies in elasticity and trust.

Elasticity

Under the gold standard, the supply of gold was determined by mining and trade balances. It was highly inelastic. When a banking panic struck and depositors raced to convert deposits into gold, the central bank could not create new gold. It could only lend its existing gold reserves, which were finite. This inelasticity was the mechanism that turned local bank distress into systemic panics, as famously described by Walter Bagehot and documented by O. M. W. Sprague. By contrast, in a fiat system with a central bank, reserves are perfectly elastic at the policy interest rate. The central bank can create as many reserves as needed to settle payments and to act as lender of last resort. This elasticity is not a flaw; it is the feature that has eliminated the convertibility panics that plagued the gold standard.

Trust

Gold’s value rested on its physical properties and its historical acceptance as a commodity money. Reserves have no intrinsic value; their value rests on the fact that the state accepts them as the sole means of settling tax obligations and interbank payments. That is a different foundation – legal and fiscal rather than metallurgical – but it has proven operationally robust. The question is not whether reserves are “better” than gold, but whether a state‑backed fiat apex can perform the same settlement and store‑of‑value functions without the fragility that gold introduced.

What the Comparison Reveals About the 97% Statistic

The 97% figure is often presented as if it were a unique feature of modern fiat money – an argument that private banks have seized control of money creation. In fact, the proportion of inside money to outside money has always been large. The innovation of the twentieth century was not the 97% but the replacement of an inelastic gold apex with an elastic reserve apex.

This substitution had a profound effect on the 97% itself. Under gold, the inside money pyramid was perpetually vulnerable to a run on the apex. Under reserves, that specific vulnerability has been removed. The 97% of bank deposits are now backed, operationally, by a state‑issued asset that can be created in unlimited quantities to prevent a systemic collapse. That does not make bank deposits risk‑free – they remain private liabilities, subject to solvency and liquidity risks – but it does mean that the convertibility panic that destroyed so many banks under gold is no longer a feature of modern systems.

In summary, reserves play a major part in the 97% not because reserves themselves are a large component of the money stock (they are not – typically 5‑10% of broad money in normal times) but because they are the indispensable settlement asset that allows the 97% to circulate. Gold played the same functional role in its era, but with a fatal design flaw: it could not be created in a panic. Recognising this difference is essential for any honest reading of the 97% statistic. It is not evidence of private dominance; it is evidence of the enduring necessity of an apex – whether gold or reserves – and of the superior elasticity of the modern state‑issued alternative.

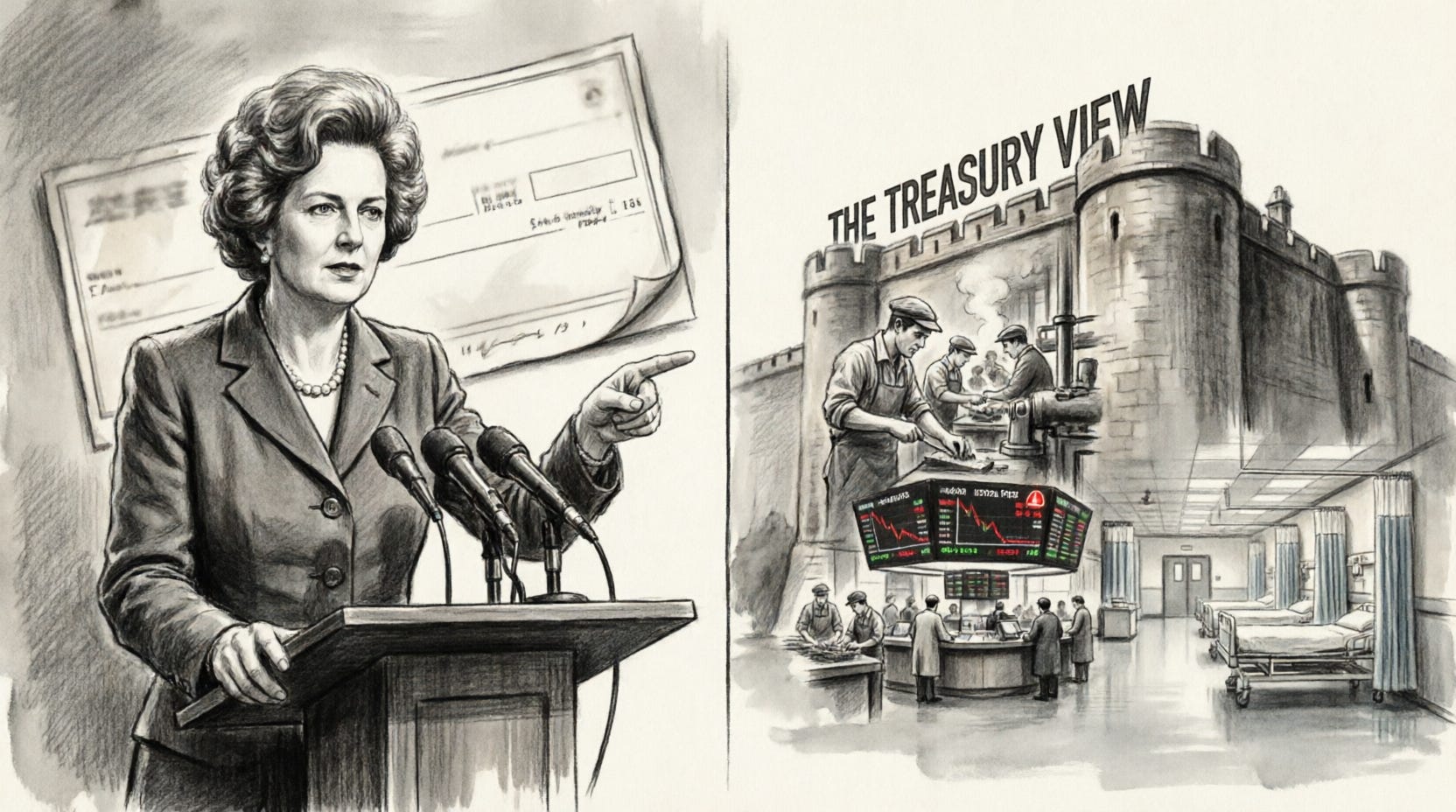

The “Only Taxpayers’ Money” Myth

The second persistent myth appears most starkly in political rhetoric about public finance. Margaret Thatcher frequently articulated the view that “There is no such thing as public money; there is only taxpayers’ money”, a sentiment she expressed in various forms, including her 1975 Conservative Party Conference speech from the Margaret Thatcher Foundation Archive. The statement has been repeatedly invoked by subsequent political figures and has entered the common sense of fiscal discourse.

From the perspective of monetary operations, the statement is false — but its falsehood is not immediately obvious to anyone lacking a clear distinction between base money and bank deposits. The government spends by instructing the central bank to credit private bank accounts; it taxes by instructing the central bank to debit them. The sequence in a sovereign currency system is not tax-then-spend, as the household analogy suggests, but spend-then-tax. The Treasury cannot draw down tax revenue that has not yet been collected, but nor does it need to. As Modern Monetary Theory scholars have argued, a sovereign government with its own currency faces no numerical constraint on its spending prior to taxation — though it does face real constraints on inflation and resource allocation.

The myth persists precisely because it exploits the muddle. To the average citizen, money resides in a bank deposit. The government taxes that deposit and spends it elsewhere. The conclusion that the government must therefore have taken the money from taxpayers appears unarguable. The missing premise is that when the government spends, it does not “spend” existing deposits. It creates new deposits — new inside money — ex nihilo, balanced by an equal and opposite entry on the central bank’s balance sheet. The deposit that the citizen loses to taxation and the deposit that the recipient gains from government spending are not the same deposit. They are two distinct entries, separated in time and in the sequence of accounts.

Monetary Mystique

Why the Muddle Endures

The persistence of the monetary muddle across centuries and institutional regimes raises a further question: why does it not dissipate under sustained scrutiny? One influential answer, developed most systematically by the economist Karl Brunner, is that central banking has cultivated a culture of deliberate or emergent secrecy — a monetary mystique — that protects its operational autonomy while impeding public understanding.

Brunner’s formulation has been widely cited. In a much-quoted paragraph from 1981, he wrote that central banking “has been traditionally surrounded by a peculiar and protective political mystique”. He elaborated: “The mystique thrives on a pervasive impression that central banking is an esoteric art. Access to this art and its proper execution is confined to the initiated elite” Verified via Brunner, K. (1981). “The Case Against the Fed.” The Cato Journal, Vol. 1, No. 2, as cited in Goodfriend (1986). The esoteric nature of the art, in Brunner’s account, is “revealed by an inherent impossibility to articulate its insights in explicit and intelligible words and sentences. Communication with the uninitiated breaks down”.

Subsequent research has refined and extended Brunner’s insight. Marvin Goodfriend’s 1986 article “Monetary Mystique: Secrecy and Central Banking” (published in the Journal of Monetary Economics) remains a foundational treatment. A 2022 assessment described Goodfriend’s work as “an extremely well-written, meticulous, and fair analysis and critique of the Federal Reserve’s defence of its practice of secrecy,” noting that “when Marvin wrote and published his paper, central banking was generally cloaked in mystery” Svensson, L. E. O. (2022).

The motives for maintaining monetary mystique are not necessarily malign. Central banks face a genuine trade-off between transparency and operational effectiveness. As one study of political pressures and monetary mystique observed, a central bank could use monetary mystique to obtain greater insulation from political pressures, even if the government faces no direct cost of overriding. A degree of opacity may be a rational institutional response to the danger that short-term political pressures will overrule sound monetary policy.

As one former Federal Reserve official stated bluntly in testimony later cited by Frederic Mishkin, “secrecy is designed to shield the Fed from political oversight” Mishkin, F. (2004). This was not from malign motives, but from the legitimate but short-term pressures that elected officials necessarily bring to bear.

Nevertheless, the trade-off is increasingly contested. The trend over recent decades has been toward greater central bank transparency, a development that some scholars interpret as a gradual erosion of the monetary mystique. The transition “from secretiveness to transparency and accountability” has been characterised as “a reluctance to give out any information at all to the belief in communication as a panacea for effective policy” Issing, O. (2002). Yet the persistence of the two myths analysed above suggests that formal transparency — the publication of minutes, inflation reports, and balance sheets — does not automatically translate into conceptual clarity among non-specialist audiences.

The muddle’s longevity thus reflects a confluence of factors: the genuine complexity of monetary operations, the institutional incentives for central banks to preserve a degree of mystique, the asymmetrical distribution of monetary literacy across populations, and the absence of any political constituency for widespread public education in monetary mechanics.

Conclusion

Clarity without Fragility

The analysis offered here has followed a single thread — the conceptual distinction between government base money and private bank liabilities — across three historical and institutional contexts: the panic-prone gold standard, the statistical misinterpretation of modern money creation, and the fiscal mythology of “only taxpayers’ money.” In each case, the confusion of categories has produced real consequences: financial instability, misplaced political blame, and policy debates conducted with systematically misleading premises.

A crucial element of this muddle is the endurance of the “Treasury View” in the United Kingdom. This doctrine, which posits that government borrowing crowds out private investment and that spending must be funded by taxation, has been criticised since at least Keynes. Yet it persists not as a law of nature, but as a working policy choice. It has been suspended many times for political and economic expediency — during wars, financial crises, and pandemics — demonstrating that it is an imposed political constraint, not an operational necessity. By treating this policy choice as an immutable economic law, the state reinforces the monetary muddle, obscuring the fact that fiscal space is determined by real resources and inflation, not by arbitrary accounting rules.

The conclusion is not that the muddle can or should be entirely eliminated. Some degree of opacity may be functional. Central bank independence is widely regarded as a valuable institutional achievement, and that independence may require a protective buffer against the full transparency that democratic accountability might otherwise demand.

What is possible, however, is a more systematic effort to distinguish — in public communication, in economic education, and in policy debate — between outside money and inside money; between the state’s liability and the bank’s liability; between what the government can do with a keystroke and what it must ultimately justify in terms of real resource allocation and inflationary constraint. Without that distinction, the history of monetary confusion will continue to repeat itself, each time dressed in the institutional clothing of its era but animated by the same conceptual failure.

The opening comment’s observation about a “muddle on redeemability” was not a technical aside. It was a diagnosis of the foundational weakness of commodity-based monetary systems — and a warning that conceptual clarity is not a luxury but a prerequisite for institutional stability. The task ahead is not to eliminate the muddle entirely but to prevent it from generating the same destructive dynamics in new forms.

Bibliography

Bagehot, W. (1873). Lombard Street: A Description of the Money Market. London: Henry S. King & Co.

Bank of England. (2014). “Money Creation in the Modern Economy.” Quarterly Bulletin, Q1.

Bignon, V., Flandreau, M., & Ugolini, S. (2011). “Where It All Began: Lending of Last Resort and the Bank of England during the Overend-Gurney Panic of 1866.” Norges Bank Working Paper.

Brunner, K. (1981). “The Case Against the Fed.” The Cato Journal, Vol. 1, No. 2.

Brunner, K. (1984). “Monetary Policy and Monetary Mystique.” Carnegie-Rochester Conference Series on Public Policy.

Eichengreen, B. (1992). Golden Fetters: The Gold Standard and the Great Depression, 1919–1939. New York: Oxford University Press.

Goodfriend, M. (1986). “Monetary Mystique: Secrecy and Central Banking.” Journal of Monetary Economics, Vol. 17, pp. 63–97.

Goodhart, C. A. E. (1987). “Why Do Banks Need a Central Bank?” Oxford Economic Papers, Vol. 39, No. 1, pp. 75–89.

Issing, O. (2002). Communication, Transparency, Accountability: Monetary Policy in the Twenty-First Century.

Mishkin, F. (2004). “Transparency and Monetary Policy: What Does the Academic Literature Tell Policymakers?” In Explorations in Economic Policy, Conference Volume. Sydney: Reserve Bank of Australia. Available at: https://www.rba.gov.au/publications/confs/2004/mishkin.html

Mitchell-Innes, A. (1913). “What is Money?” The Banking Law Journal.

Mitchell-Innes, A. (1914). “The Credit Theory of Money.” The Banking Law Journal.

Sprague, O. M. W. (1910). History of Crises under the National Banking System. Washington, D.C.: National Monetary Commission.

Thatcher, M. (1975). Speech to the Conservative Party Conference.

Turner, A. (2016). Between Debt and the Devil: Money, Credit, and Fixing Global Finance. Princeton University Press.

Wicker, E. (2006). “Were Panics of the National Banking Era Preventable?” In Banking Panics of the Gilded Age, Chapter 6, pp. 114-138. Cambridge: Cambridge University Press.

Wray, L. R. (2015). Modern Money Theory: A Primer on Macroeconomics for Sovereign Monetary Systems. Palgrave Macmillan.

See Also…

Printing Permanence

The Persistence of State Issuance, the Ephemeral Nature of Bank Credit (and How to Measure the State’s Footprint)

It is not so much what sits at the top of a monetary hierarchy and more which liabilities the state chooses to guarantee.

Logically the payments system should be separate from bank credit creation.

Much muddle comes from not recognizing this.

I think the reality of government spending always creating new money is concealed because if people knew they would be more likely to try to avoid paying tax.