Gilt by Association

The Bondage of an Illusory Debt

A Graphic Novella

Abstract

UK government bonds (gilts) are usually treated as proof of the state’s fiscal weakness. Rising yields are called a “cost” to taxpayers and a warning from bond vigilantes that austerity is needed. This article, written from a Modern Monetary Theory (MMT) perspective, tears down that story. It explains what gilts really are, why they are issued, how auctions work, and what happens in secondary markets. Then it shows why gilt yields have nothing to do with the government’s ability to spend, and how the media’s obsession with yields is not economics but politics.

The article also looks at today’s context: the Bank of England’s aggressive gilt sales and the “Bailey premium” – a self‑inflicted, multi‑billion‑pound cost that exposes the flaws of orthodox Quantitative Tightening.

Introduction

No financial instrument is more misunderstood than the UK gilt. Orthodoxy sees a government IOU – debt that must be paid for by taxes or future cuts. When yields rise, headlines scream “crisis”. From an MMT standpoint, almost every word of that framing is wrong. Today this misunderstanding is not just academic; it is actively weaponised by the Bank of England itself, which is selling gilts for no operational reason, creating an expensive “Bailey premium” and draining public money.

MMT insists on getting the institutional facts right. This article walks through the full life of a gilt, then shows how the noise around yields – including today’s manufactured noise – is politicised to enforce fiscal discipline.

The Orthodox Story vs. the MMT Reality

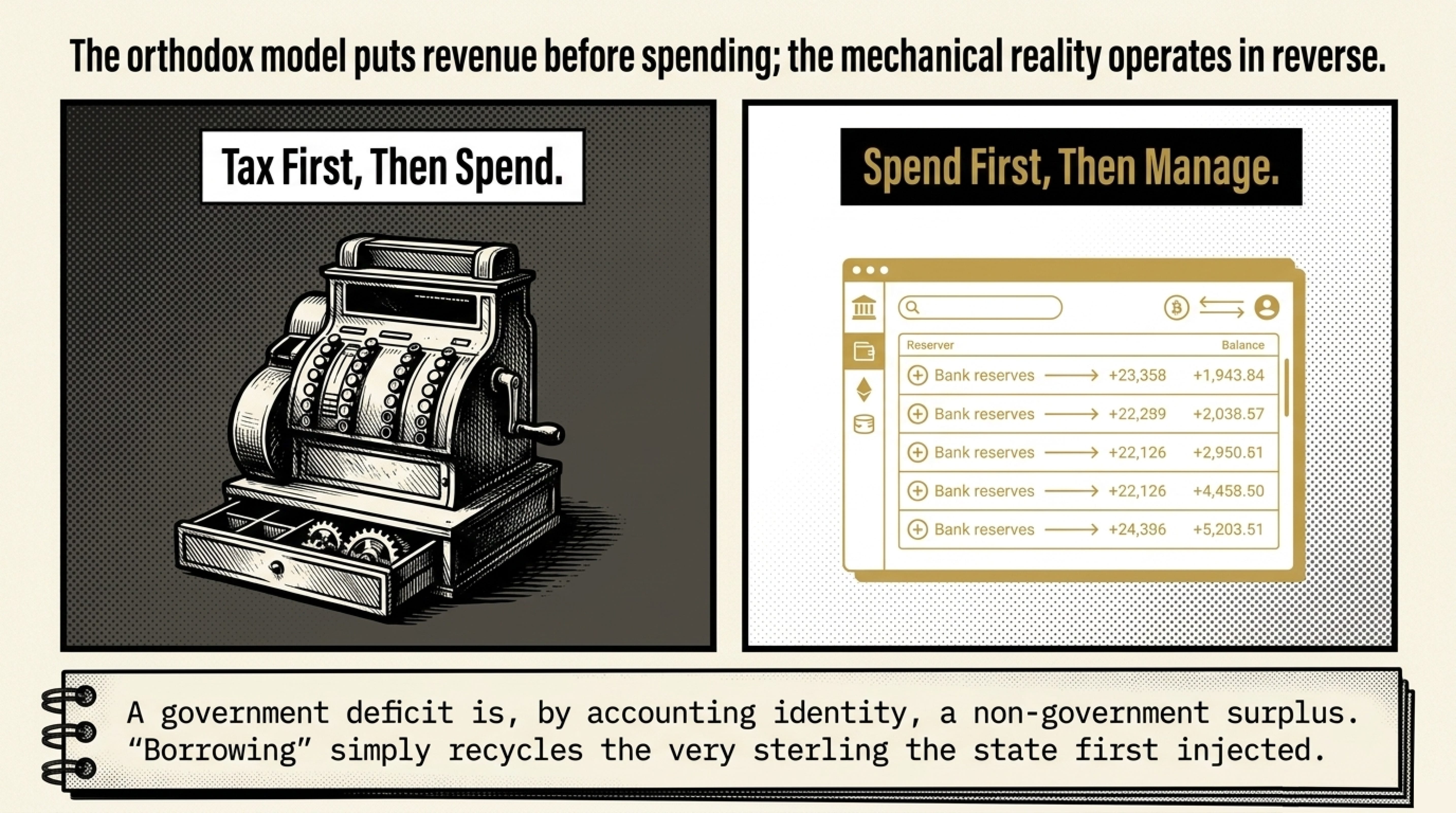

Orthodoxy: The government must collect money from the private sector (via taxes or bond sales) before it can spend. Too much borrowing depletes private savings, raises interest rates, and “crowds out” investment. Rising bond yields mean markets have lost confidence. Austerity is the only answer. This logic now justifies Quantitative Tightening (QT): a large central bank balance sheet is supposedly inflationary and must be shrunk by selling bonds.

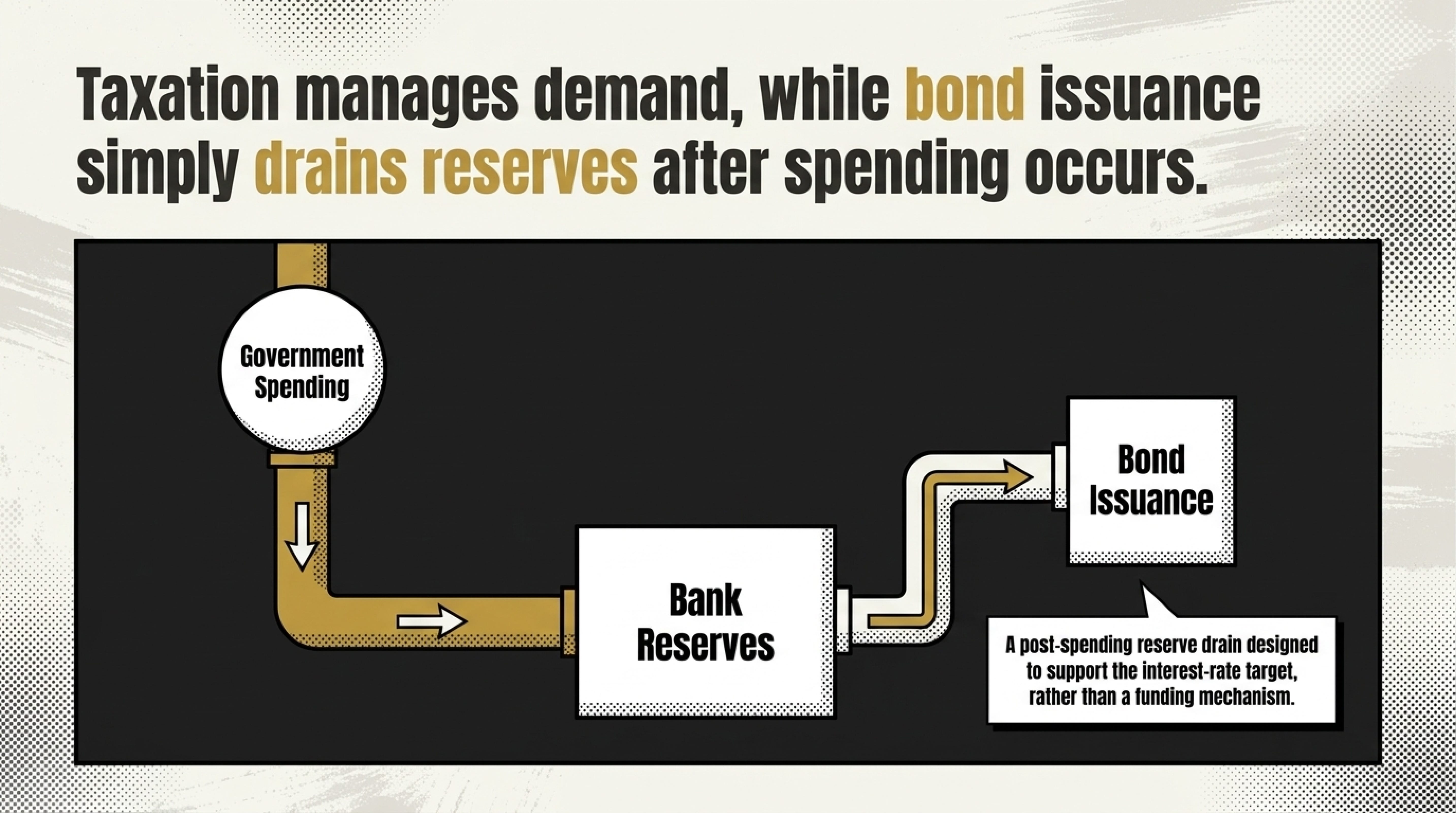

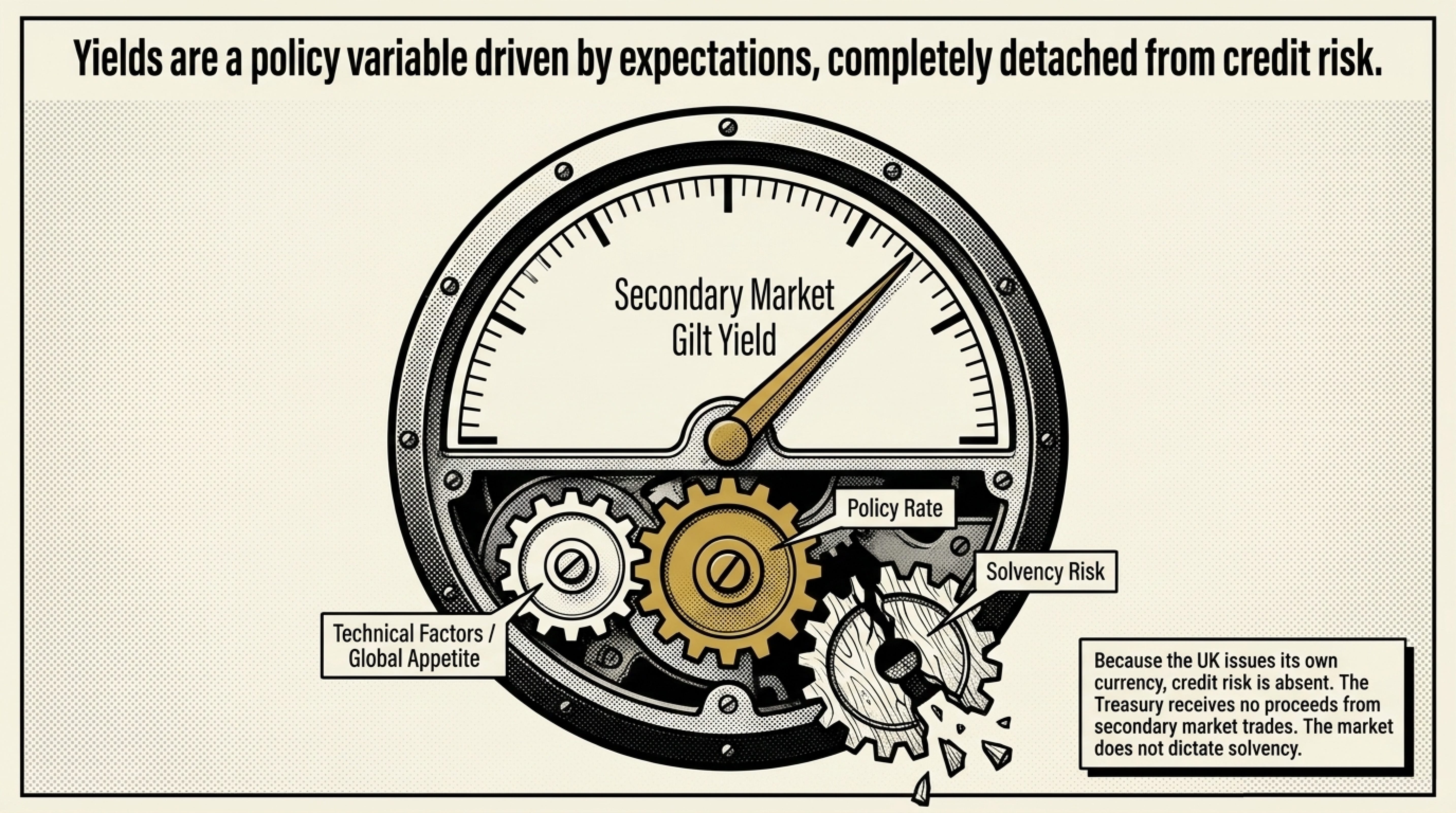

MMT: A sovereign currency issuer never needs to “fund” its spending. It spends by crediting bank reserves. Taxation manages demand, not revenue. Bond issuance is a post‑spending reserve drain to support the interest‑rate target. Crucially, a government deficit is, by accounting identity, a non‑government surplus – so “borrowing” from the private sector just recycles the sterling the state first injected. Gilt yields reflect the Bank of England’s policy rate and market technicals, not solvency risk. The state issues sterling; it never uses it.

What Are Gilts and Why Do They Exist?

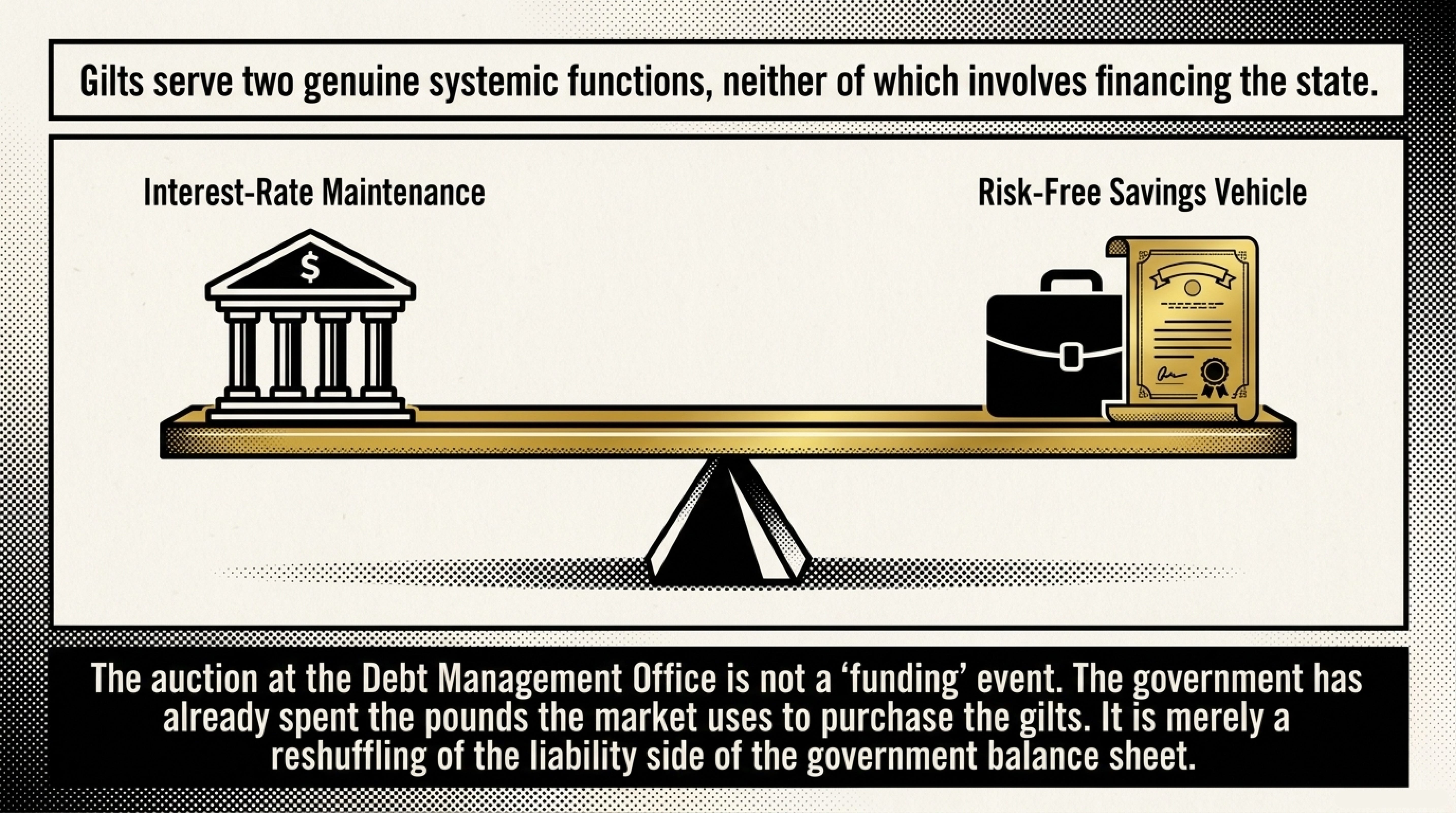

Today gilts have two genuine functions: interest‑rate maintenance (draining excess reserves to keep the overnight rate at Bank Rate) and providing a risk‑free, long‑dated savings vehicle for the private sector, especially pension funds. Issuing gilts is a policy choice about the term structure of government liabilities – not a question of affordability. The government could instead leave reserves in the system and pay a support rate on them, which is exactly what the Bank now does with its Tiered Reserves framework.

The Auction Process

Gilts are issued by the Debt Management Office (DMO) through competitive auctions to Gilt‑edged Market Makers (GEMMs). The auction is not a “funding” event. The government has already spent the pounds that will be used to buy the gilts. Those pounds sit in reserve accounts. At settlement, reserves are transferred from the buyer’s bank to the government’s Consolidated Fund at the Bank of England – a reshuffling of the liability side of the consolidated balance sheet, not a financing operation.

The Secondary Market: Trading, Derivatives, and Yield Discovery

Once a gilt is outstanding, it trades in a deep secondary market – cash, futures, swaps, baskets, and repo. Yield determination is a mix of expected Bank Rate, term premia, pension rules, global risk appetite, and technical factors like collateral scarcity. Credit risk is absent because the UK issues its own currency. The secondary market is just a reallocation of existing government liabilities among private entities; the Treasury receives no proceeds from secondary trades.

Yields and the State

An MMT Deconstruction

The orthodox story says rising gilt yields force austerity. MMT shows that maturing gilts and coupon payments are settled with keystrokes by the Bank of England. There is no operational constraint. Interest payments are an intra‑governmental transfer – for domestic holders, a redistribution within the sterling zone, with no net change in private sector net financial assets. The central bank can, if it chooses, buy gilts to stabilise markets. Quantitative easing proved this: the Bank bought over a third of the gilt market by crediting reserves, and yields fell because the central bank set a price‑insensitive bid. Gilt yields are ultimately a policy variable.

The Politics of Yields

Weaponising a Misunderstanding

The bond‑market‑as‑disciplinarian narrative serves powerful interests: it frames public investment as waste, provides cover for austerity, and protects asset owners. The 2022 mini‑budget panic was not a solvency crisis but a financial stability event caused by leveraged pension funds – which the Bank of England swiftly contained by buying gilts, proving it can control the market whenever it chooses. The call for a return to “orthodox” policy was a political choice dressed up as market necessity.

The Present Trap

Quantitative Tightening and the “Bailey Premium”

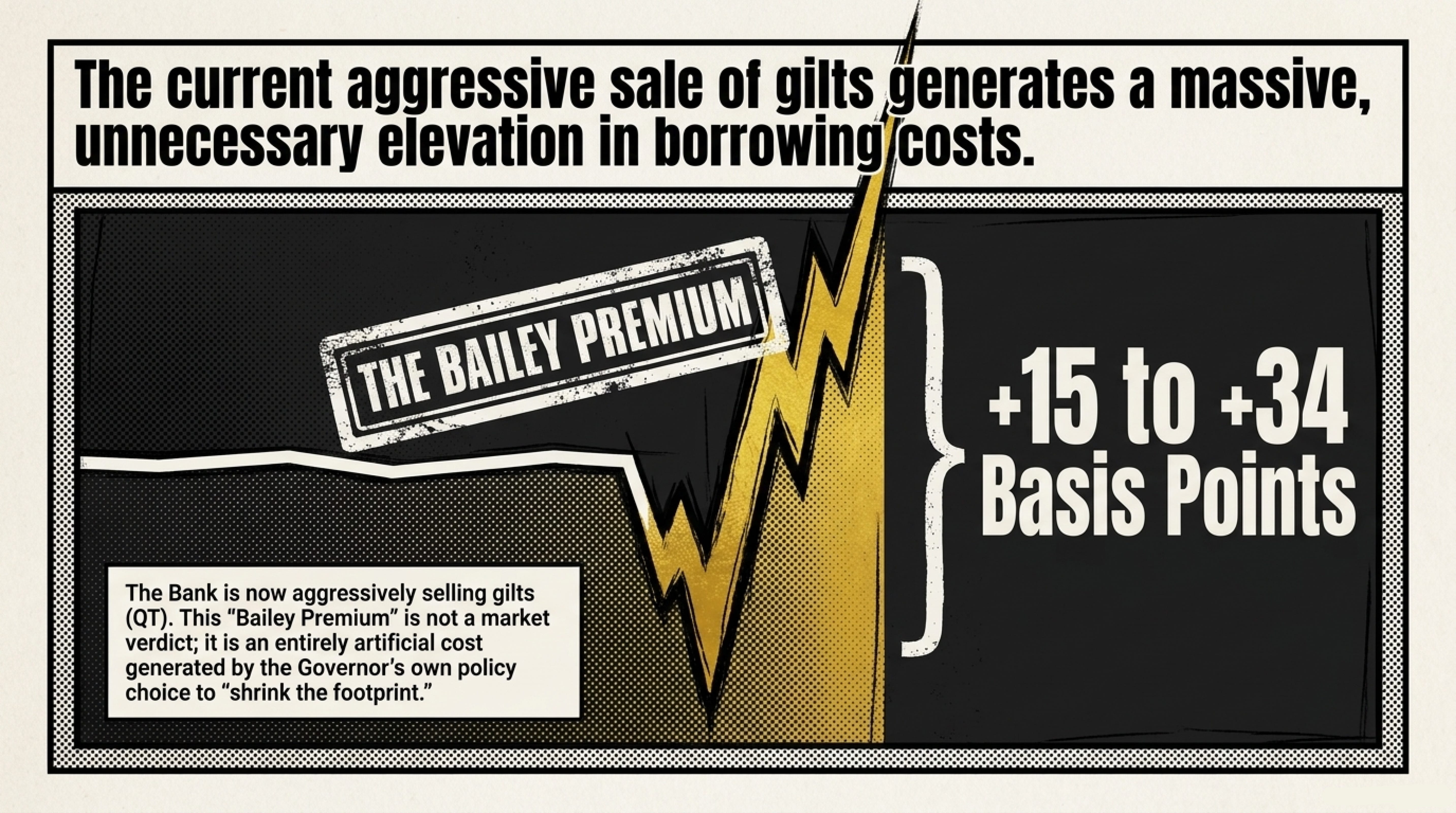

All of this brings us to the current moment. As Daniela Gabor recently noted, the Bank of England was until recently the largest single holder of UK gilts, a legacy of QE. It has since been aggressively selling those gilts “for no good reason other than Bailey wants to”, creating what she rightly calls a “Bailey premium” – an entirely unnecessary rise in long‑term borrowing costs. From an MMT perspective, this programme is a perfect case study in self‑inflicted fiscal harm and flawed economic theology.

What is QT and why is the Bank doing it?

Quantitative Tightening (QT) is the reverse of QE. The Bank of England has been actively selling gilts from its Asset Purchase Facility (APF) at a pace of £100 billion per year, plus letting some bonds mature without reinvestment. The orthodox justification is that a large balance sheet leaves “excess” reserves which could fuel inflation, and that shrinking the balance sheet restores monetary discipline.

The “Bailey premium” quantified

Active gilt sales dump extra supply onto the market, mechanically pushing prices down and yields up. The Bank’s own estimates suggest these sales may have raised 10‑year gilt yields by 15‑25 basis points. Independent researchers put the impact at 25‑34 basis points. This persistent elevation is the “Bailey premium” – an entirely unnecessary increase in government borrowing costs, generated by the Governor’s own policy choice.

The fiscal cost

a direct drain on the public purse

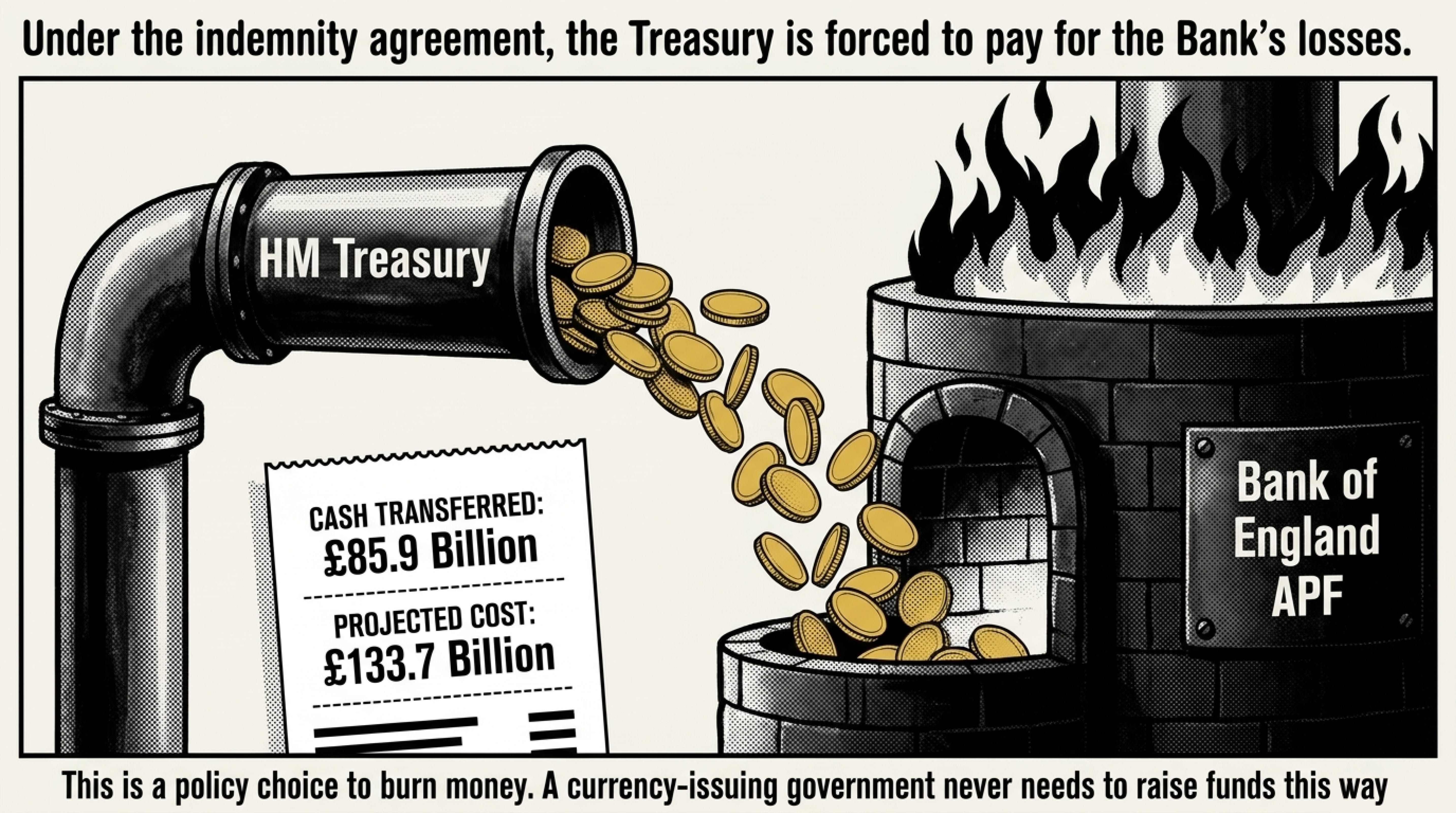

Under the indemnity agreement between the Bank of England and HM Treasury, any losses incurred by the APF are paid directly by the government. By actively selling gilts in a falling market, the Bank has turned unrealised valuation changes into huge, crystallised cash losses. Since October 2022, £85.9 billion has been transferred from the Treasury to the Bank of England to cover these losses. The Office for Budget Responsibility projects the total lifetime cost could reach £133.7 billion. In MMT terms, a currency‑issuing government never needs to raise funds this way. This enormous fiscal transfer serves no purpose – it is a policy choice to burn money.

QT is operationally unnecessary

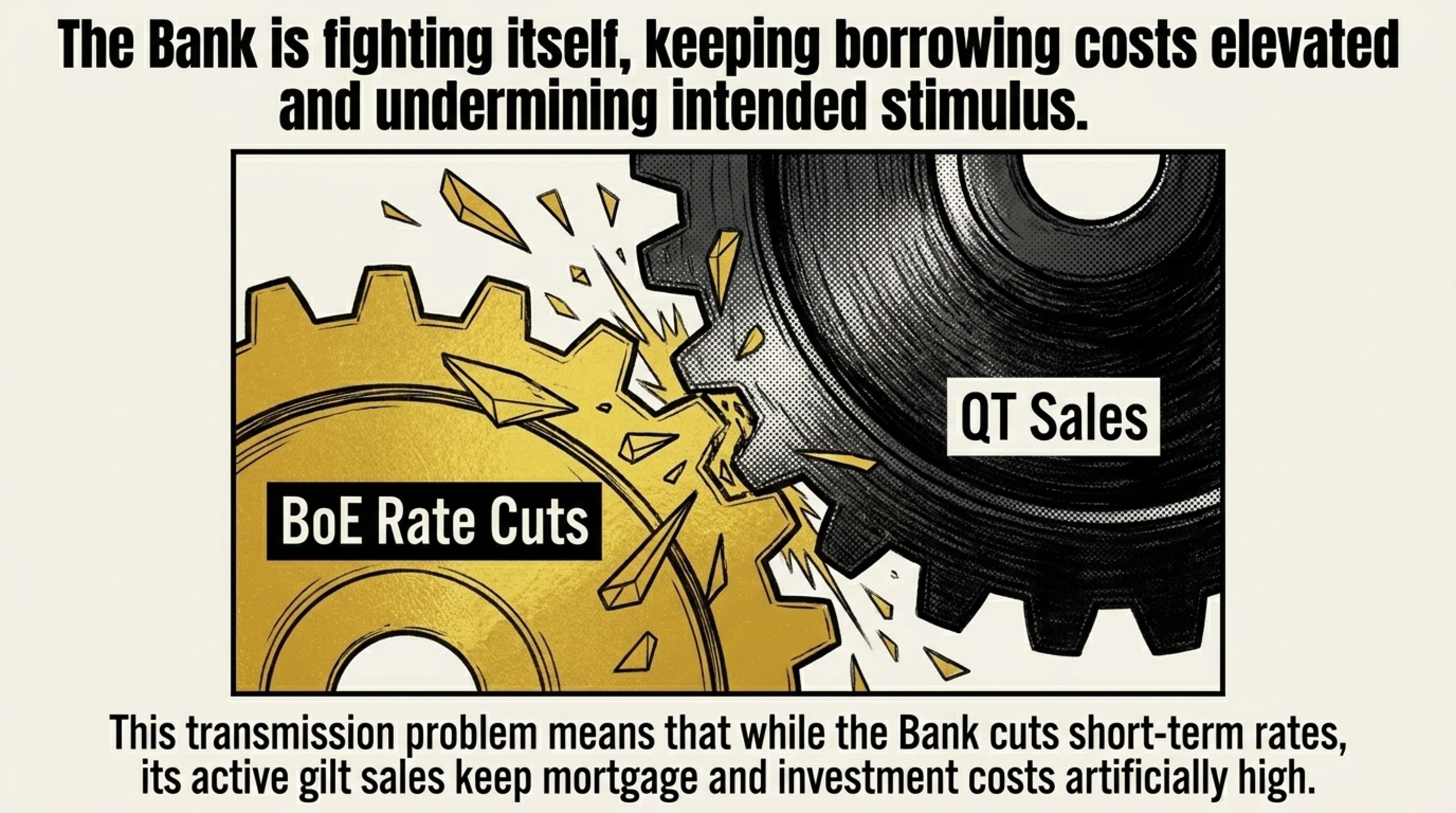

MMT shows that draining reserves to control inflation is a fallacy. Bank lending is not constrained by the quantity of reserves. The Bank of England can always control the overnight interest rate directly by paying interest on reserves – and it already does so through its tiered reserves framework. If the concern were truly about aggregate demand, the Treasury could use fiscal policy (taxation or reduced spending) to withdraw purchasing power. Instead, QT actively raises the long end of the yield curve at the same time that the Monetary Policy Committee is cutting short‑term rates, creating a “transmission problem”: long‑term borrowing costs for mortgages and corporate investment remain elevated, directly undermining the intended stimulus. The Bank is fighting itself.

A political choice

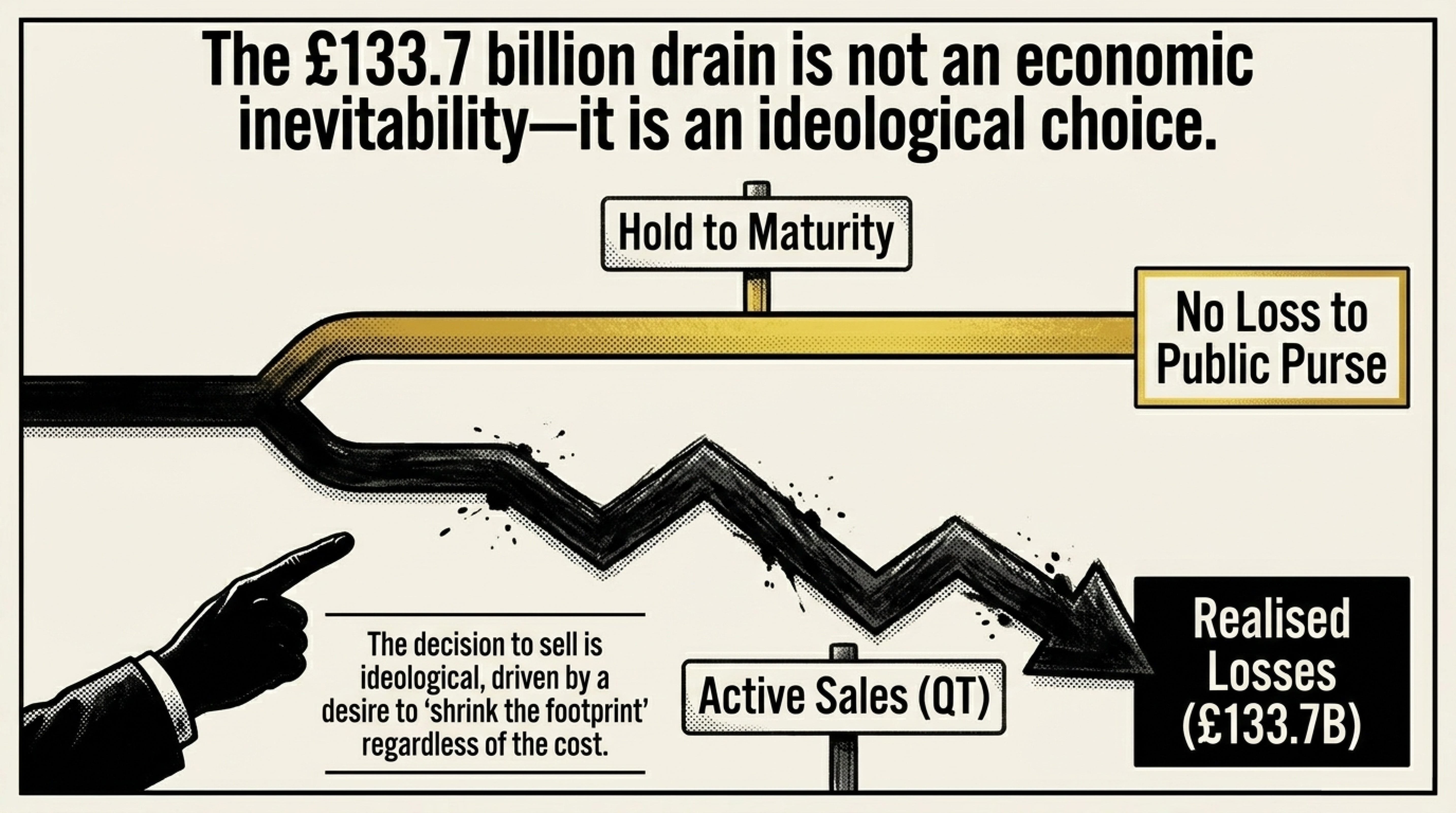

not an economic necessity

The Bank of England could simply hold its gilt portfolio to maturity, letting it roll off the balance sheet gradually with no market turmoil or realised losses. The decision to sell aggressively is an ideological choice to shrink the central bank’s footprint. As Daniela Gabor’s comment makes plain, the “Bailey premium” is not a market verdict on UK solvency – it is a policy‑generated cost, created by the very institution that claims to be safeguarding economic stability.

Conclusion

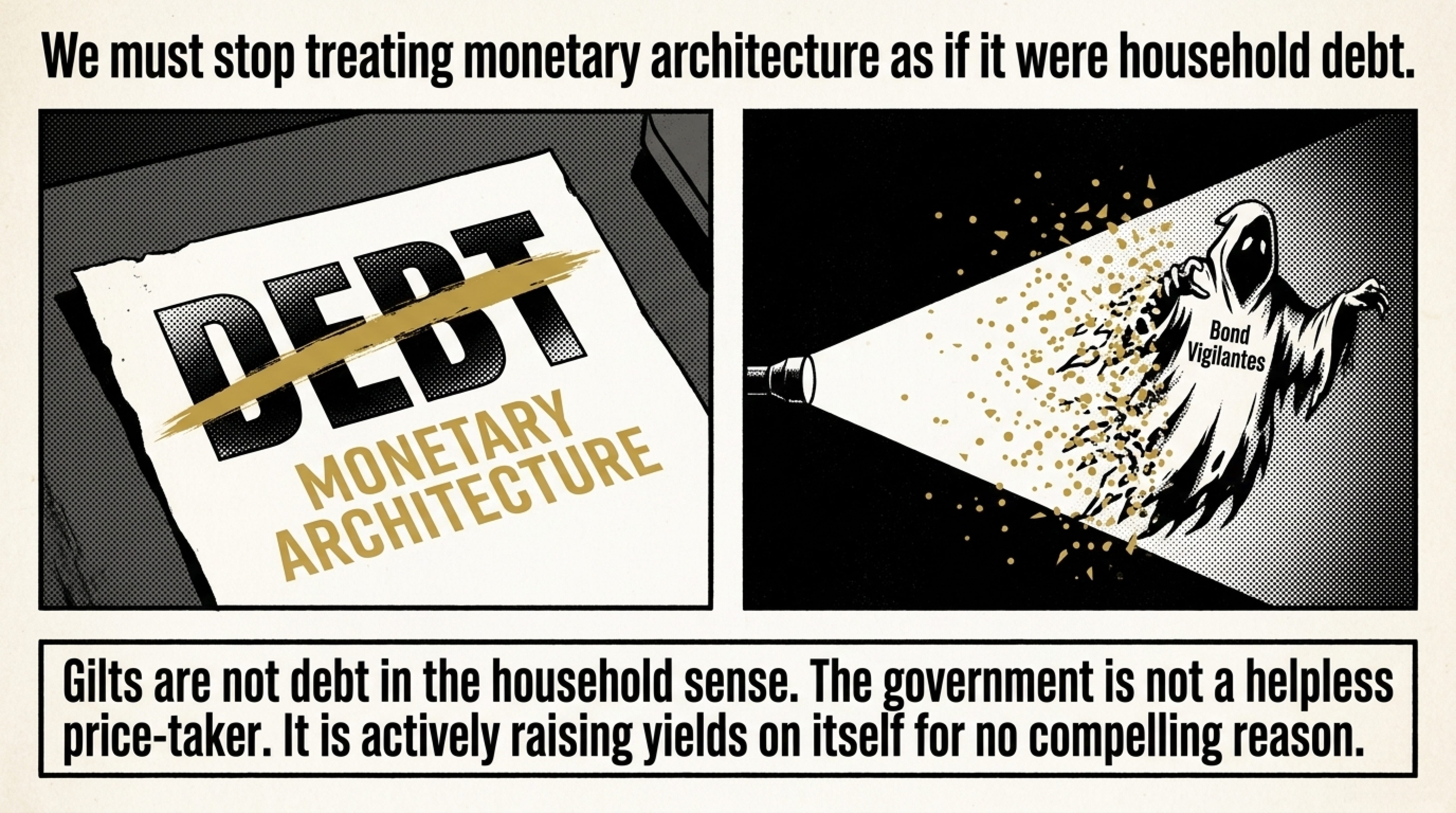

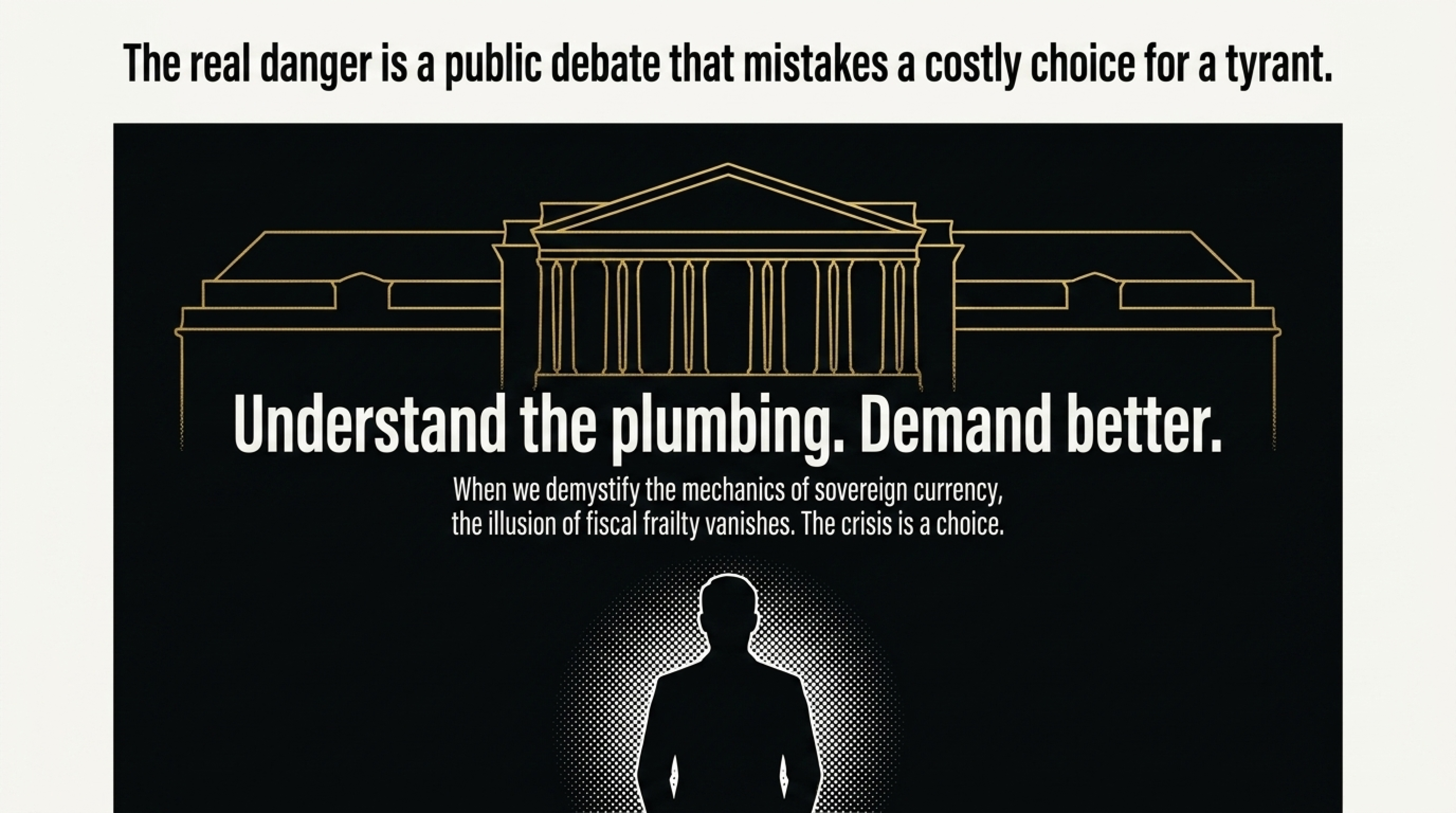

Gilts are not debt in the household sense. They are a component of the UK’s monetary architecture, and their yields are a variable over which the Bank of England exercises ultimate control. The current gilt sales programme and the resulting “Bailey premium” offer a vivid, real‑time demonstration of this article’s central thesis. The government is not a helpless price‑taker forced into austerity by bond vigilantes; it is actively, and expensively, raising yields on itself for no compelling operational reason. The £133 billion drain from the Treasury to the Bank is not an economic inevitability – it is a policy error, a self‑imposed tax arising from a failure to understand the nature of a sovereign currency. The phantom of the bond vigilante has been replaced by a self‑manufactured premium, paid by the public to satisfy a misguided monetary doctrine. The real danger remains a public debate that mistakes a costly choice for a tyrant.

References

BBC (2025) ‘BoE bond sales may be pushing up borrowing costs by more than thought, research shows’, BBC News, 25 November. Available at: https://www.bbc.co.uk/news

Bell, S. (2000) ‘Do taxes and bonds finance government spending?’, Journal of Economic Issues, 34(3), pp. 603–620. doi:10.1080/00213624.2000.11506287

Berkeley, A. et al. (2025) ‘The Self-Financing State: An Institutional Analysis of Government Expenditure, Revenue Collection and Debt Issuance Operations in the United Kingdom’, Journal of Economic Issues, 59(3), pp. 852–880. doi: 10.1080/00213624.2025.2533726.

Bloomberg (2025) ‘Bank of England should end gilt sales, former rate-setter says’, Bloomberg, 15 September. Available at: https://www.bloomberg.com

Fullwiler, S.T. (2016) ‘The debt ratio and sustainable macroeconomic policy’, World Economic Review, 7, pp. 12–42.

Gabor, D. (@DanielaGabor) (2025) [Tweet], 10 May. Available at:

Kelton, S. (2020) The deficit myth: Modern Monetary Theory and how to build a better economy. London: John Murray.

Milas, C. (2025) ‘Quantitative tightening and gilt yields: new evidence’, Economic Policy Review, forthcoming. Cited in: Reuters (2025) and BBC (2025).

Mosler, W. (2010) The 7 deadly innocent frauds of economic policy. Valance.

Office for Budget Responsibility (2023) Economic and fiscal outlook – November 2023, Box 4.2: Fiscal accounting for quantitative easing and tightening. London: OBR. Available at: https://obr.uk

Reuters (2025) ‘Bank of England sees bigger QT impact on gilt yields’, Reuters, 7 August. Available at: https://www.reuters.com

UK Debt Management Office (2025) GEMM guidebook: a guide to the roles of the DMO and primary dealers in the UK government bond market. Available at: https://www.dmo.gov.uk

UK Debt Management Office (2025) Official operations in the gilt market – an operational notice. Available at: https://www.dmo.gov.uk

UK Parliament (2025a) Written Answer HL6355: Asset Purchase Facility indemnity, 9 April. Available at: https://questions-statements.parliament.uk

UK Parliament (2025b) Written Answer HL6354: Quantitative Tightening Costs, 9 April. Available at: https://questions-statements.parliament.uk

Wray, L.R. (2012) Modern Money Theory: a primer on macroeconomics for sovereign monetary systems. Basingstoke: Palgrave Macmillan.

Excellent, Michael. Thank you.