The Golden Straitjacket

The Gold Inflation Argument is Built on Historical Fiction

A Graphic Novella

If you spend any time in certain corners of the financial internet, you will inevitably encounter the gold bug’s favourite talking point. The argument is always presented as a simple, irrefutable mathematical proof: in 1971, an ounce of gold cost $35. Today, it trades well over $4,000. Therefore, the US dollar has lost over 99% of its purchasing power, proving that fiat currency is a catastrophic failure and that we must return to the gold standard.

It is a neat narrative. It is also an elementary error that conflates the removal of a legally enforced price ceiling with currency debasement. From an MMT perspective, the gold standard was never a “natural” monetary anchor; it was an administrative fiat, a political straitjacket, and ultimately, a mathematical impossibility.

Here is why the gold bug’s proof collapses under rigorous historical and fiscal analysis.

The $35 Price Was an Administrative Fiction

Not a Market Signal

The foundational flaw in the gold bug’s argument is the assumption that the $35 per ounce price was a free-market equilibrium. It was nothing of the sort. It was a policy choice, unilaterally set and violently enforced by the state.

Following the Great Depression, President Franklin D. Roosevelt issued Executive Order 6102 in 1933,

which effectively criminalised the private hoarding of gold bullion by US citizens, forcing them to sell their holdings to the Federal Reserve at the existing price of $20.67 per ounce under the new mandate (later raised to $35 in 1934).

Private US citizens were largely forbidden from owning monetary gold until 1975. Foreign central banks could convert dollars to gold, but ordinary investors could not. Comparing the $35 administrative peg to today’s floating market price is analytically absurd. It is akin to comparing Soviet-era rent controls to modern market rents and blaming “money printing” for the difference. The subsequent rise in gold’s dollar price was not a measure of general inflation; it was the market’s revaluation of a previously suppressed asset once the legal coercion was lifted.

The Triffin Dilemma

The Peg Was Mathematically Doomed

Why did President Nixon “close the gold window” in 1971? The gold bug narrative suggests this was an ideological betrayal. The historical reality is that the United States was physically running out of gold.

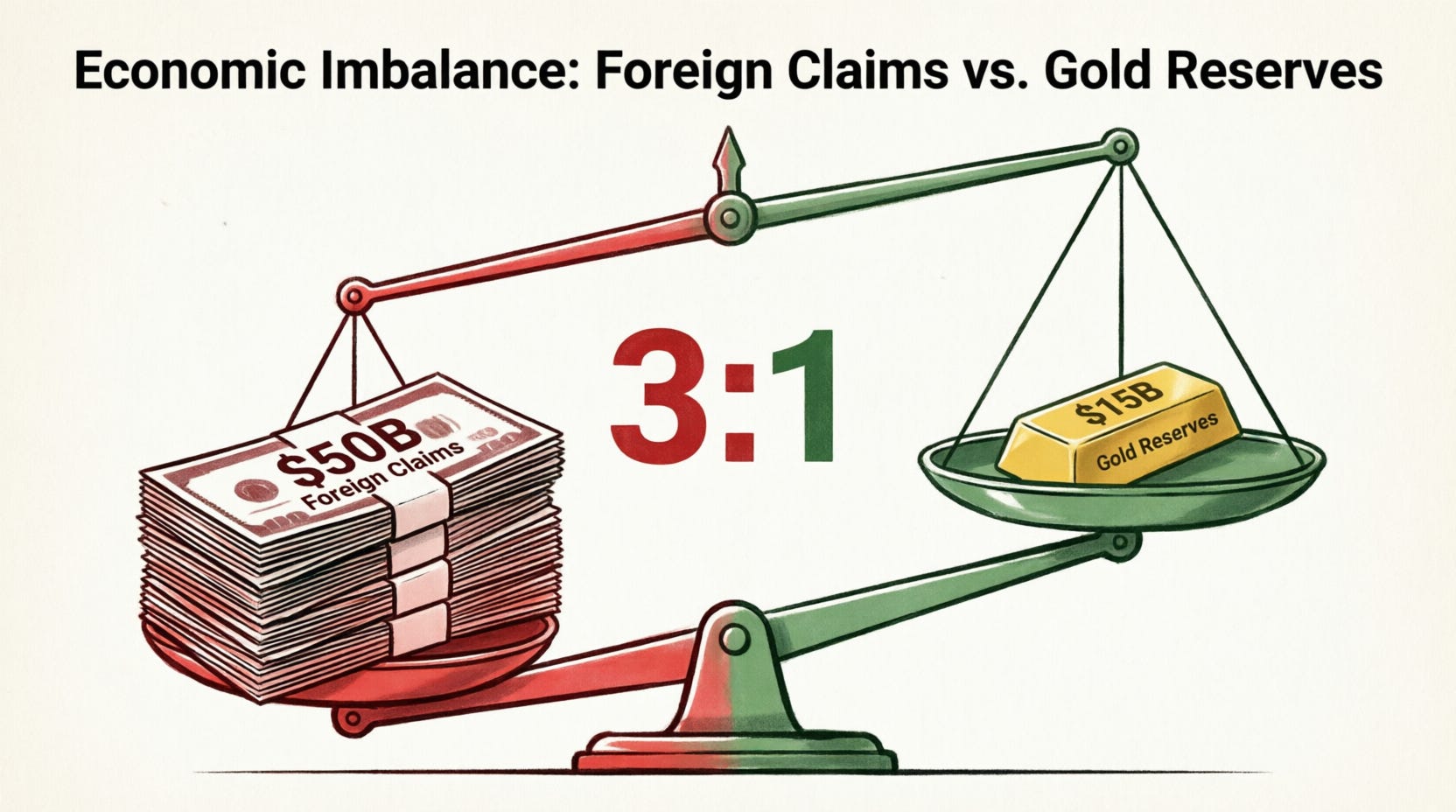

Under the Bretton Woods system, the global economy required US dollars for international trade and reserves. To supply these dollars, the US had to run persistent balance of payments deficits. However, this created the “Triffin Dilemma”: the more dollars the world held, the less confidence there was in the US ability to redeem them for gold. By 1971, foreign holdings of US dollars had ballooned to over $50 billion, while US gold reserves were valued at a mere $15 billion.

Nixon did not merely remove a price control; the US defaulted on a contract it could no longer honour. The gold standard did not fail because fiat is inherently flawed; it collapsed under the weight of its own mathematical contradictions.

The UK Precedent

Liberation, Not Collapse

For a proper fiscal perspective, we need only look across the Atlantic. The United Kingdom did not wait until 1971 to realise the gold standard was a destructive constraint. Britain suspended the gold standard in September 1931.

At the time, the UK Treasury and the Bank of England recognised that defending the sterling peg was importing catastrophic deflation and mass unemployment during the Great Depression. By abandoning the gold parity, the UK freed itself to pursue reflationary fiscal and monetary policies, allowing the state to mobilise idle labour and real resources. The historical record is clear: leaving gold was an act of economic liberation, not a descent into monetary chaos.

The Real Constraint vs. The Monetary Constraint

MMT posits that all money is a social and legal construct. The pound or the dollar functions today because the state imposes tax liabilities payable only in that currency, creating a baseline demand for it.

The gold bug’s obsession with the metal ignores the actual constraint on a sovereign fiat currency: real productive capacity. Inflation does not occur simply because the government runs a fiscal programme or creates money. It occurs when aggregate demand outstrips the economy’s capacity to produce goods and services (e.g., there is not enough steel, energy, or labour to meet demand).

Furthermore, gold’s modern price action has little to do with acting as a “passive inflation meter”. Gold yields zero interest. Its price is heavily financialised, acting as a speculative bond-proxy that surges when real interest rates fall and the opportunity cost of holding a non-yielding asset drops.

Conclusion

The gold bug’s “proof” is a category error. The $35 price was a legally enforced ceiling. Once that ceiling was removed and private trading legalised, gold’s price sought a new level reflecting speculation, industrial demand, and its role as a crisis hedge.

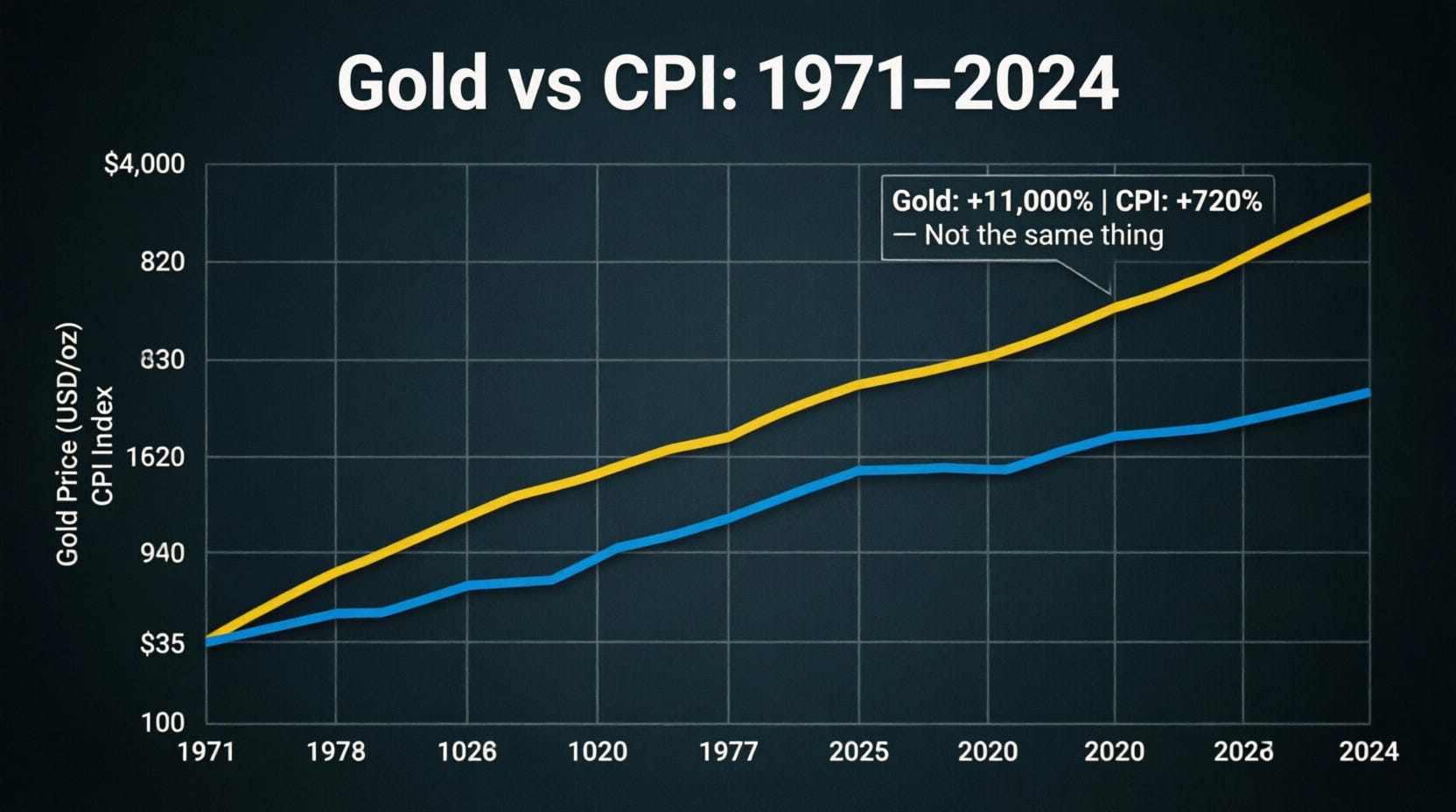

If anything, the post-1971 era highlights the remarkable resilience of fiat currency. Despite over 50 years of floating exchange rates, massive fiscal deficits, and multiple global recessions, the US dollar has not hyperinflated. General inflation, while currently a focal point of policy, has been modest by historical standards when viewed across the entire post-Bretton Woods era. For instance, according to the US Bureau of Labor Statistics, the Consumer Price Index has risen by a cumulative 722% (roughly 8-fold) between 1971 and 2024, a far cry from the 10,000%+ increase in the nominal price of gold.

The gold standard was a political choice. Its removal allowed modern economies to function. Clinging to it today is not rigorous economics; it is historical nostalgia.

Bibliography

Executive Order 6102 (1933)

Claim: The US government criminalised the private hoarding of gold bullion in 1933, forcing sales to the Federal Reserve.

https://www.usgoldbureau.com/content/gold-confiscationThe Triffin Dilemma and 1971 Gold Reserves

Claim: By 1971, foreign holdings of US dollars exceeded $50 billion, while US gold reserves were valued at only $15 billion, making the peg mathematically unsustainable.

https://www.federalreservehistory.org/essays/gold-convertibility-endsThe UK Abandonment of the Gold Standard (1931)

Claim: The United Kingdom suspended the gold standard in September 1931 to escape deflationary pressures and pursue reflationary policy.

https://www.nationalarchives.gov.uk/education/resources/thirties-britain/going-gold/US Consumer Price Index (CPI) Cumulative Increase

Claim: The US CPI has risen by approximately 722% (roughly 8-fold) between 1971 and 2024, demonstrating that gold’s price increase vastly outpaces general inflation.

https://www.bls.gov/data/inflation_calculator.htmModern Gold Pricing and Financialisation

Claim: Gold’s modern price is driven by financialisation, real interest rates, and its role as a non-yielding speculative asset, rather than acting as a simple inflation meter.

https://www.gold.org/goldhub/data/gold-prices

"Under the Bretton Woods system, the global economy required US dollars for international trade and reserves. To supply these dollars, the US had to run persistent balance of payments deficits."

Was this part of the agreement, or did the U.S. just do this reflexively because the dollar was rising against other currencies because it was the international unit of account, making imports cheap, and exports expensive?

Then, as discussed before, issuance of--at least the Federal Reserve-issued portion of--currency required active open market operations by the Federal Reserve (as treasury and bank payment net issuance were self draining by Treasury auction and the overnight market, respectively), or else the banks wouldn't have the reserves to pay for the currency, since all other counterparty payments resulting in net reserve creation were spoken for by the overnight market or it's subcategory, Treasury auctions.

__________________________

Another thing I noticed is that gold bullion being a third of currency was but one of a range of odd ratios during the period.

1. 1939, for instance: bullion was double currency, something one would think bound to drive scarcity of bullion and thereby by the law of supply and demand put the same sort of pressure on the currency one saw leading on down to 1970.

2. Or 1930: bullion roughly equaled currency. As one thinks of bullion as simply a kind of starter yeast, that too is odd. But then one realizes that at that time, some share of currency existed in ten and twenty dollar coin, making the ratio of gold to redeemable gold certificates even somewhat higher than one-to-one, even odder, as is the problem with the 1939 numbers; I mean, at a glance.

Then, you suggest that a thirty percent (fifteen to fifty) ratio is "wrong," but what, then *is* a good ratio, would you say? Or more to the point, what used to be this ratio back in the day, 1901, 1910, 1920? And why did this "crisis" not occur back in 1792 and throughout the nineteenth century? I know bullion-backed paper money is the problem, as one wouldn't see the problem of having to redeem coin with, say, coin back in trimetallic era. But in the early nineteenth century, the issue one hears is always a lack of industrial scale minting machinery, and never a shortage of bullion of either silver nor gold--as coin would still need bullion to mint it with.

"at the newly mandated price of $20.67 per ounce"

Not newly mandated, it's from 1901, but I think before, 1834. The 1792 ratio was very slightly lower (nine tenths of gold, one tenth of copper, by weight, so the volume of copper was a lot more..., for the twenty dollar one ounce coin), although we're really talking coins, not a weight in bullion, to my mind, up until at least 1901, although the Constitution on this point seems a bit unreadable to my eye. Note, it would be troy ounces, not regular ounces.