The Visible Hand

State Money in Times of Crisis

Part 4 of a series…

How the hierarchy of money operates when private systems fail – evidence from the US, UK, and Switzerland.

There is a moment in every financial crisis when the invisible hand of the market seizes up, and the very visible hand of the state must take over. The theoretical frameworks we have explored – Mehrling’s hierarchy of money and MMT’s understanding of state currency – find their most dramatic expression when governments are forced to mobilise public money at scale to rescue a financial system broken by the actions of commercial banks and shadow banking.

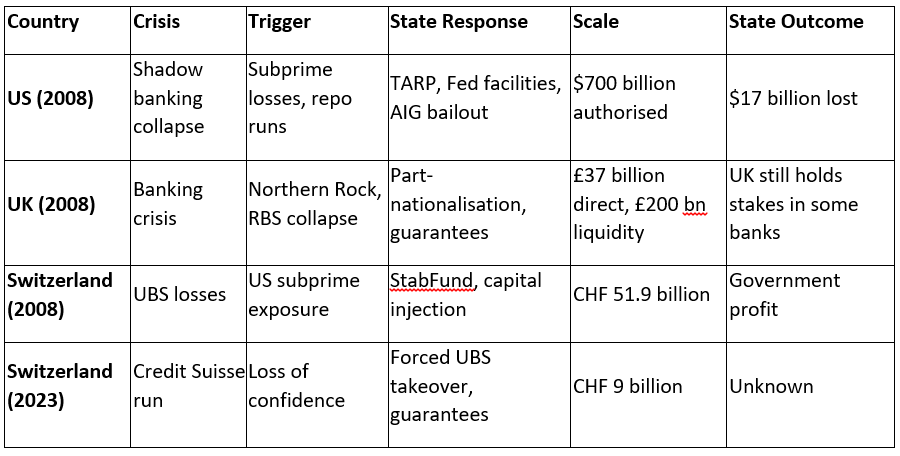

This article examines three such scenarios: the United States in 2008, the United Kingdom in 2008, and Switzerland across two crises (2008 and 2023). Each demonstrates the same fundamental truth: when private money creation goes wrong, state money – and only state money – can restore stability. From an MMT perspective, these interventions confirm that currency-sovereign states face no financial constraint in preventing depression; the only limits are political will and inflation risk.

The United States (2008): TARP, AIG, and the Shadow Banking Run

The American financial crisis of 2008 is the defining example of state intervention in modern history. What began as a problem with subprime mortgages spread through a shadow banking system that had grown beyond regulatory oversight, culminating in a full-scale run on institutions that were not banks but acted like them.

The Shadow Banking Problem

As Lev Menand documents, the crisis was not primarily about commercial banks – it was about “shadow banks: financial firms that operate in similar ways to a bank but aren’t regulated like one” (Menand 2022). Lehman Brothers, Bear Stearns, and other investment banks funded long-term lending with short-term borrowings that people treated as cash equivalents. When confidence evaporated, the shadow banking system experienced the same kind of run that had plagued the 19th-century banking system.

The trigger came in March 2008. On 10 March, Bear Stearns had $18 billion in liquidity reserves. By 13 March, that had plunged to $2 billion. Hedge funds were pulling their money; repo lenders were refusing to roll over loans. Bear Stearns was not a commercial bank – it did not have access to the Federal Reserve’s discount window. Under normal rules, it would have been left to fail.

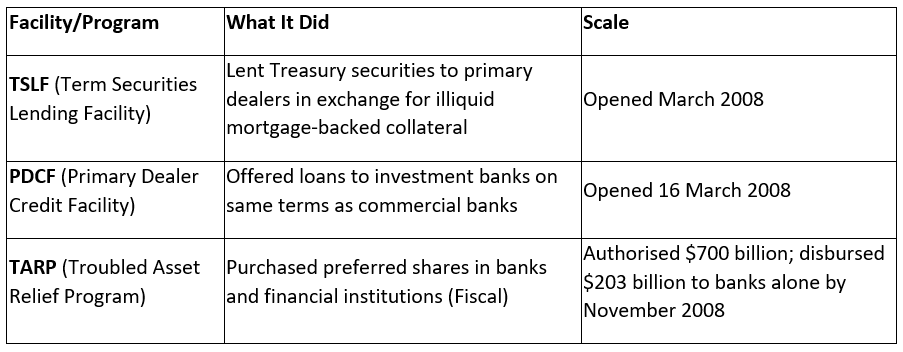

The State Mobilises: From TSLF to TARP

The Federal Reserve invoked its emergency powers under Section 13(3) of the Federal Reserve Act, which authorises loans to non-banks in “unusual and exigent circumstances”. Over the following months, the state deployed an extraordinary array of interventions. MMT Insight: It is crucial to distinguish between monetary operations (Fed facilities) and fiscal operations (TARP). The Fed creates liquidity; the Treasury spends appropriated funds. Both rely on state power, but TARP required Congressional approval, demonstrating that fiscal space is a political choice, not a financial constraint.

The Bear Stearns rescue itself was extraordinary. The Fed created an off-balance-sheet entity called Maiden Lane, loaned it $29 billion, and used it to acquire $30 billion of Bear’s most toxic assets – mostly non-prime mortgage-related securities. This effectively transferred risk from the private sector to the public balance sheet.

When Lehman Brothers was allowed to fail in September 2008, the resulting panic forced even larger interventions. The Fed and Treasury arranged a bailout of American International Group (AIG) – a massive insurance company whose shadow banking activities through credit default swaps had made it too interconnected to fail. The AIG rescue alone would eventually total $40 billion in TARP capital plus $112.5 billion in Fed loans.

The Scale of State Intervention

The full scope of state mobilisation was staggering:

$700 billion authorised under TARP.

$250 billion initially allocated for bank capital purchases.

$40 billion directly to AIG from TARP, with the Fed providing another $112.5 billion in separate facilities.

$25 billion each to JPMorgan Chase, Citigroup, and Wells Fargo.

$15 billion to Bank of America.

$10 billion each to Goldman Sachs and Morgan Stanley.

By the end of the programme, $635 billion had been distributed; $17 billion was ultimately lost or written off. MMT Insight: The fact that the US could mobilise these sums without solvency concerns demonstrates the privilege of issuing the world’s reserve currency. The constraint was not finding the dollars, but managing the political fallout of using them.

The Shadow Banking Dimension

What made 2008 distinct was the shadow banking component. The Fed had never before provided liquidity assistance to non-bank financial institutions – but the crisis forced its hand. As Fed Vice Chairman Donald Kohn observed at the time, “the dysfunction in the securities markets and the banking sector were intertwined, and there was just a very vicious spiral going on”.

The state had to intervene not just to save commercial banks, but to stabilise the entire parallel financial system that had grown up alongside them.

The United Kingdom (2008): Nationalisation by Stealth

Across the Atlantic, the British government faced a similar crisis but chose a different path – one that resulted in direct state ownership of major banks on a scale not seen since the post-war nationalisations.

The Collapse of Light-Touch Regulation

Britain had been the poster child for financial deregulation. London’s financial centre – the City – contributed some 20 per cent to GDP, and the government’s “light-touch regulation” was celebrated as a model of innovation. As one legal expert noted bluntly: “Britain’s celebrated light-touch regulation... was virtually no touch at all”.

The first signs of trouble came in September 2007 with Northern Rock – the first run on a British bank in 141 years. But the real crisis erupted in October 2008, when the government was forced to act decisively.

The £37 Billion Intervention

On 7 October 2008, the Labour government announced a part-nationalisation plan that would have been unthinkable weeks earlier:

Royal Bank of Scotland (RBS): £20 billion capital injection, giving the government a 57 per cent stake.

Lloyds TSB/HBOS merger: £17 billion injection, giving the government a 40 per cent stake.

Barclays: Raised £6.5 billion independently, avoiding government help.

The government also:

Doubled the Bank of England’s loan facility to banks, to £200 billion.

Made £250 billion available in loan guarantees to encourage interbank lending.

State Exposure and Currency Sovereignty

The scale of exposure was breathtaking. The three banks receiving capital held combined assets of approximately £2.75 trillion – far exceeding the UK’s GDP of £1.55 trillion. The state was now exposed to 45 per cent of the UK mortgage market and heavily exposed to commercial property through RBS and HBOS.

One analyst calculated that the total package – £500 billion including guarantees – represented more than one-third of GDP. As the Reuters analysis noted, this was a “gamble money worth more than one-third of GDP” on rescuing the banks (Neligan & Slater 2008). MMT Insight: Crucially, the UK faced no risk of default on these guarantees because they were denominated in sterling, a currency the UK issues. Unlike Eurozone nations (e.g., Greece, Ireland) who faced solvency crises because they lacked currency sovereignty, the UK’s constraint was inflationary pressure, not insolvency.

The Human Consequences

The crisis had real-world consequences beyond the balance sheets. By October 2008, the City of London’s bars and restaurants were “almost empty,” with one headhunter describing the atmosphere as feeling “like Armageddon”. Capio Nightingale, the City’s only mental health hospital, reported that requests for relief from “Square Mile Syndrome” – anxiety and depression – were up 33 per cent since July.

For ordinary Britons like antiques dealer Jenny Hicks-Beech, the sense was terrifying: “The fact that you feel you cannot trust the banks with your money is terrifying; we’ve never been in this situation before”.

Switzerland: Two Crises, Two Approaches

Switzerland offers a fascinating comparative case, having faced two very different banking crises – one in 2008 and another in 2023 – and responded with distinct state interventions.

2008: The UBS Rescue

When UBS faced collapse in 2008 due to losses on US subprime assets, the Swiss state intervened but structured the rescue to minimise state risk:

CHF 45.9 billion of illiquid assets transferred to StabFund, a stabilisation fund controlled by the Swiss National Bank.

CHF 6 billion direct capital injection from the federal government.

The government sold its stake in summer 2009 – and made a profit of CHF 1.2 billion.

The SNB sold the StabFund to UBS in 2013, also making a profit (USD 3.76 billion).

This was state intervention structured as a temporary backstop, with the government acting as a temporary owner rather than permanent rescuer.

2023: The Credit Suisse Collapse

The 2023 crisis at Credit Suisse was fundamentally different. Where UBS had suffered losses from identifiable toxic assets, Credit Suisse faced a crisis of confidence – a verifiable run on the bank as clients and investors lost faith.

Unlike in 2008, there was no “promising solution whereby individual assets could have been wound up in a stabilisation fund”. The bank faced immediate liquidity threats and resistance from central counterparties.

The government response was swift and extraordinary: it orchestrated the forced takeover of Credit Suisse by UBS, backed by state guarantees. The total package included up to CHF 9 billion in federal guarantees to cover potential losses. The intervention was designed to “prevent a financial crisis and extremely severe damage to the Swiss financial centre and the entire economy”.

Other Swiss Interventions

A Pattern of State Support

The Swiss government has used state money to support other systemically important sectors when private markets failed:

2020 Aviation Rescue: CHF 1.5 billion credit facility for Swiss/Edelweiss, 85 per cent federally guaranteed; fully repaid by May 2022.

2022 Axpo Rescue: CHF 4 billion credit facility for the energy company facing liquidity shortages after the Ukraine war; designed to protect Switzerland’s energy supply.

COVID-19 Credits: CHF 17 billion in guaranteed loans to businesses; 100 per cent federal guarantee for loans up to CHF 500,000, 85 per cent for larger amounts.

Each intervention followed the same pattern: private markets had failed to provide liquidity, and the state stepped in as the ultimate backstop. MMT Insight: These interventions exemplify “functional finance” – using state fiscal capacity to achieve public purpose (financial stability, energy security) regardless of deficit implications, provided real resources are available.

The Common Pattern

What These Scenarios Reveal

Across the US, UK, and Switzerland, three distinct crises reveal a common logic:

Lessons from the IMF vs. MMT

The International Monetary Fund has studied these interventions extensively. In a detailed report following the crisis, the IMF emphasised:

State intervention should be a “last resort” for systemically important institutions.

Shareholders and sometimes creditors should bear part of the losses.

State ownership should be temporary, guided by clear rules, professionally managed, and insulated from political interference.

Governments must recover funds swiftly and effectively (IMF 2009).

MMT Critique: While the IMF focuses on fiscal consolidation and moral hazard, MMT argues that the primary goal should be preserving public purpose (full employment, financial stability). The obsession with “recovering funds” misunderstands that currency-issuing governments do not need profit to sustain spending; they need to ensure real resources are not idled by financial collapse.

Where Countries Succeeded and Failed

The IMF specifically contrasted approaches:

United Kingdom (best practice): Government stakes managed through professional, politically independent body with clear exit strategy.

Greece (cautionary example): Hellenic Financial Stability Fund failed to preserve independence from political influence, refrained from legal action against executives whose failures contributed to losses, and left accountability unaddressed. MMT Insight: Greece’s struggle was compounded by its lack of currency sovereignty within the Eurozone, limiting its ability to deploy state money without external approval – a stark contrast to the UK’s autonomous capacity.

Conclusion

The Hierarchy in Practice

These scenarios illustrate the theoretical frameworks we have explored. When commercial banks and shadow banks created money elastically during the boom, they also created fragility. When the discipline of daily settlement exposed their vulnerabilities, the private system could not provide the liquidity needed.

In each case, the state – as the issuer of top-level money – had to step in. Mehrling’s “dealer of last resort” function operated at scale: central banks and treasuries provided reserves, purchased assets, and guaranteed liabilities when private markets froze. MMT’s insight – that the state cannot run out of its own currency – was demonstrated in practice: no country in these crises was constrained by an inability to create money. The constraint was political will, institutional capacity, and the risk of inflation or moral hazard.

The 2008 interventions were widely criticised at the time. One Republican congressman called TARP “a huge cow patty with a piece of marshmallow stuck in the middle of it”. Yet by 2016, TARP had wound down, having recouped most of its disbursements. The UK and US governments eventually sold their stakes, often at a profit.

The deeper lesson is that state money is not just a tool of last resort – it is the foundation upon which the entire financial system rests. When private money creation goes wrong, that foundation must be deployed at scale to prevent collapse. The question is not whether the state can act, but whether it will act in time, with the right instruments, and with sufficient understanding of the hierarchy it manages. For the citizen, this confirms that the safety of their savings ultimately depends not on bank balance sheets, but on the sovereign capacity of the state to stand behind them. MMT Final Word: This sovereign capacity is not infinite in real terms – it is bounded by inflation and resources – but it is infinite in financial terms. Understanding this distinction is the key to navigating future crises without succumbing to the myth of government insolvency.

References

Bank of England. (2008). Financial Stability Report. October 2008.

Board of Governors of the Federal Reserve System. (2008). “Fed Announces Establishment of Primary Dealer Credit Facility.” Press release, 16 March 2008.

Congressional Oversight Panel. (2009). April Oversight Report: Assessing Treasury’s Strategy for TARP. US Government Printing Office.

Federal Office for Economic Affairs (Switzerland). (2024). “Differences relative to the stabilisation of UBS, Swiss and Axpo, and to COVID-19 credits.” April 2024.

International Monetary Fund. (2009). Lessons from the Financial Crisis for Monetary Policy. Washington, DC: IMF.

Menand, L. (2022). The Fed Unbound: Central Banking in a Time of Crisis. Princeton University Press.

Neligan, M. & Slater, S. (2008). “UK bank bailout massively boosts govt exposure.” Reuters, 13 October 2008.

Pettifor, A. (2009). “America – the Bank-owned State.” Huffington Post, 20 April 2009.

Reuters. (2008). “UK bank bail-out to take big stakes in top banks.” El Economista, 12 October 2008.

Wilmarth Jr., A.E. (2020). “Bailouts Without End: Governments Provided Massive Bailouts to Rescue Universal Banks and Shadow Banks During the Financial Crisis.” In Taming the Megabanks. Oxford Academic.

For a quick AI generated video overview of this article…

Part 1 of the series

Part 2 of the series

Part 3 of the series