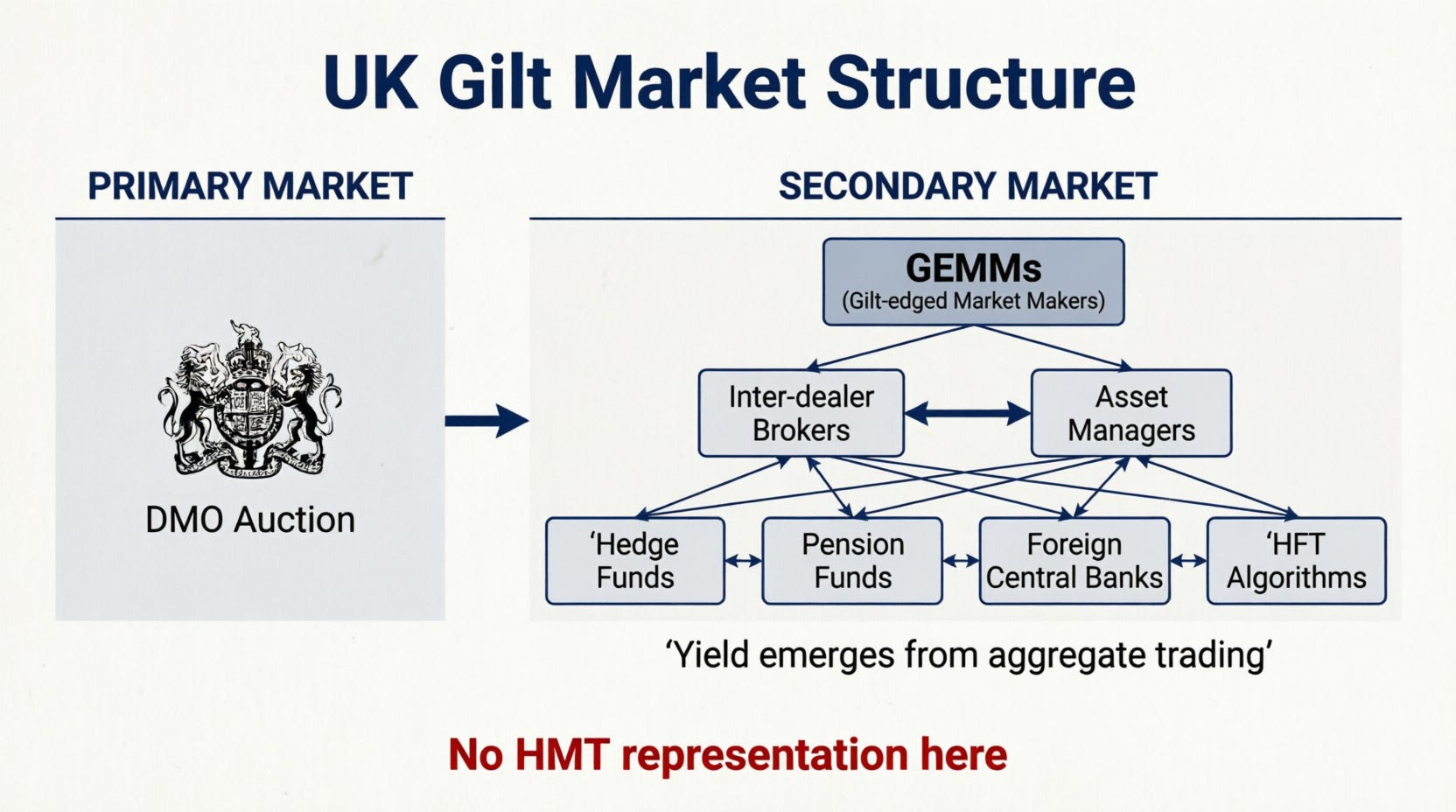

Secondary Gilt

The Primary-Secondary Distinction

What Is the Secondary Market?

The conventional distinction between primary and secondary markets is simple but carries profound implications for understanding where economic value originates—and, crucially from an MMT perspective, where operational control resides. The primary market is where new securities are created and sold directly by the issuer to investors. For gilts, the Debt Management Office (DMO) conducts auctions—such as the £3.75 billion auction of the 4⅛% Treasury Gilt 2031, which saw demand exceed supply by nearly four times with bids totalling £14.76 billion—or syndications involving a group of banks. The issuer receives the proceeds; capital flows from investors to the government.

This framing obscures the operational reality. Government spending precedes both taxation and bond issuance. The DMO auction is not a funding operation but a reserve-draining operation—swapping excess settlement balances created by fiscal deficits for interest-bearing securities. The primary market does not “finance” spending that has already occurred.

The secondary market, by contrast, is where investors trade already-issued securities among themselves. No new capital flows to the issuer. In the context of debt securities, the secondary market is defined as “the market where investors buy previously issued securities from other investors, as opposed to the primary market, where investors subscribe for new securities issued by the issuer”.

This distinction is sometimes captured in the memorable formulation: the primary market is the tap; the secondary market is the ocean. Once the gilt leaves the DMO’s auction, it enters a vast global trading ecosystem where its price is determined afresh with every transaction.

The “ocean” of secondary trading is where unaccountable private actors determine the yield on public debt—a constitutional arrangement that deserves scrutiny. Yet from an operational standpoint, these secondary market yields cannot prevent the government from spending. The constraint is inflation and real resource availability, not bond market discipline.

The Scale of the UK Gilt Secondary Market

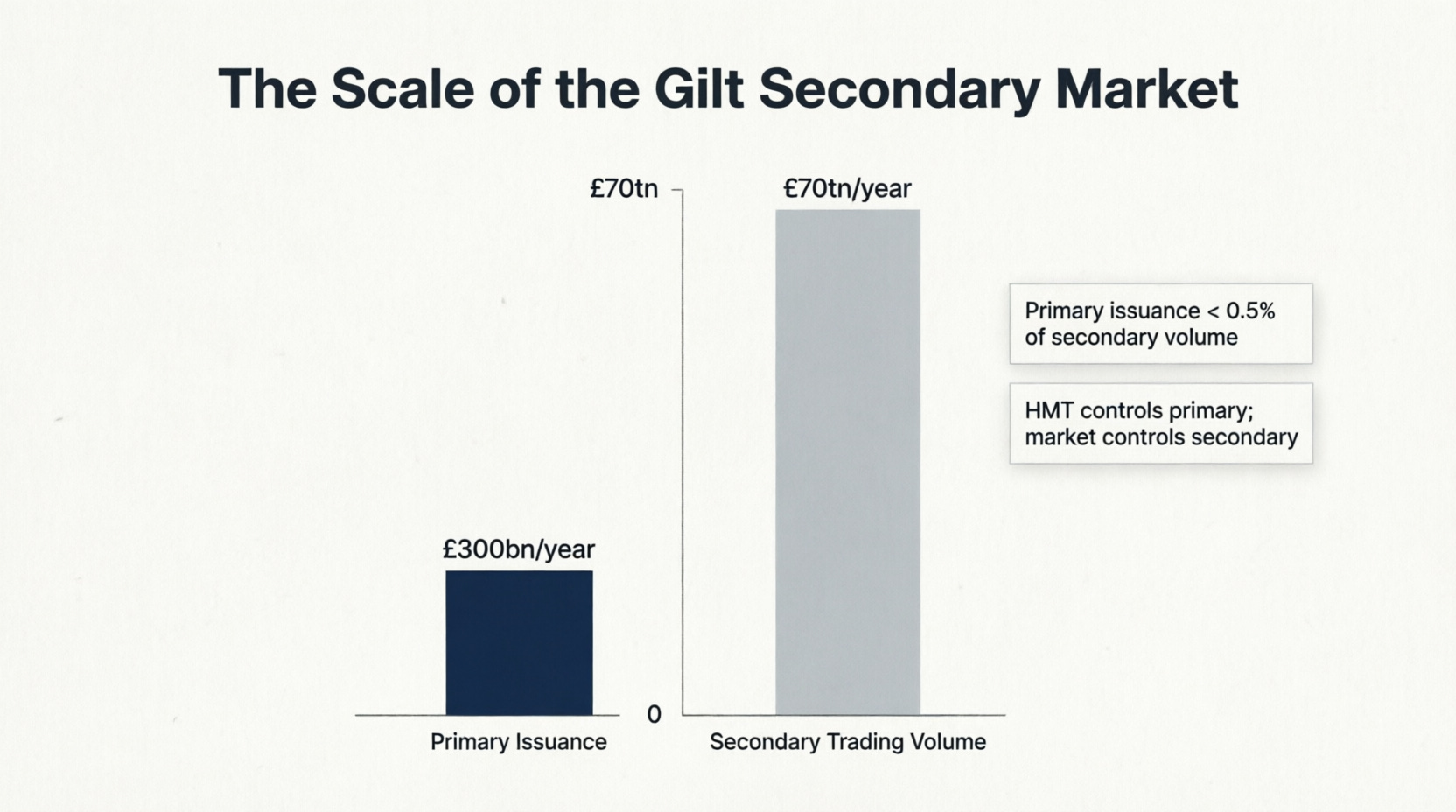

The gilt market is enormous and central to the UK financial system. There are currently over £2 trillion of gilts in issue. The government has raised its total planned gilt issuance to an estimated £308.1 billion for the current fiscal year, with the DMO announcing £12 billion of green gilts for 2026-27. Trading volumes in the secondary market dwarf primary issuance by orders of magnitude.

According to ICMA data, total trading volumes in European and UK sovereign bond markets reached €70.7 trillion in 2025, with €34.1 trillion traded in the second half alone. To put this in perspective: the entire UK gilt primary issuance for a year represents less than one-half of one per cent of annual secondary trading volumes. Approximately 53 per cent of trading volume occurs in the dealer-to-dealer market, with 38 per cent in dealer-to-client markets.

The year 2025 saw a dramatic acceleration in retail participation. Gilt trading on Hargreaves Lansdown’s platform increased by 75 per cent in January 2025 compared to the previous year, with trades almost doubling those made in December 2024. The number of gilt transactions in 2026, based on net buy and sell trades year-to-date, is already greater than the total placed in 2024.

Why the Gilt Market Matters for the Real Economy

The Bank of England monitors gilt market liquidity not as an academic exercise but because the market sits at the heart of the UK’s economic infrastructure. Its importance extends along several channels:

Government financing. The primary purpose of gilt issuance is to finance government spending. Without a functioning secondary market, investors would be unwilling to buy gilts in the primary market—the ability to exit a position is a prerequisite for entering it. As the Bank of England states, the gilt market is “fundamental to the broader UK financial system and real economy given its role in financing government activity”.

This conflates operational sequence with political economy. Gilts do not finance spending in the operational sense—the Bank of England credits accounts when the government spends. Rather, gilt issuance manages the monetary consequences of deficits by offering interest-bearing alternatives to zero-yielding reserves. The secondary market’s importance lies in maintaining demand for these bonds, which is ultimately a political choice about whether to offer bonds at all.

Benchmark pricing. Gilt yields serve as the benchmark for pricing corporate bonds, mortgages, and loans to households and businesses. When gilt yields rise, corporate borrowing costs typically follow.

Safe asset collateral. Gilts serve as “a safe and liquid asset for use as collateral or in capital regulatory requirements”. Banks, pension funds, and insurance companies rely on gilts to meet regulatory liquidity requirements and to secure funding in repo markets.

Monetary transmission. A material deterioration in gilt market liquidity “could impact monetary transmission and financial stability in the UK”. The Bank of England’s quantitative easing and quantitative tightening operations both operate through secondary gilt purchases and sales.

This reveals the circularity of the system. The state creates the demand for gilts through regulation (requiring banks and pension funds to hold them), then monitors whether the market it created is “liquid” enough. This is not a natural market phenomenon but a policy-constructed one.

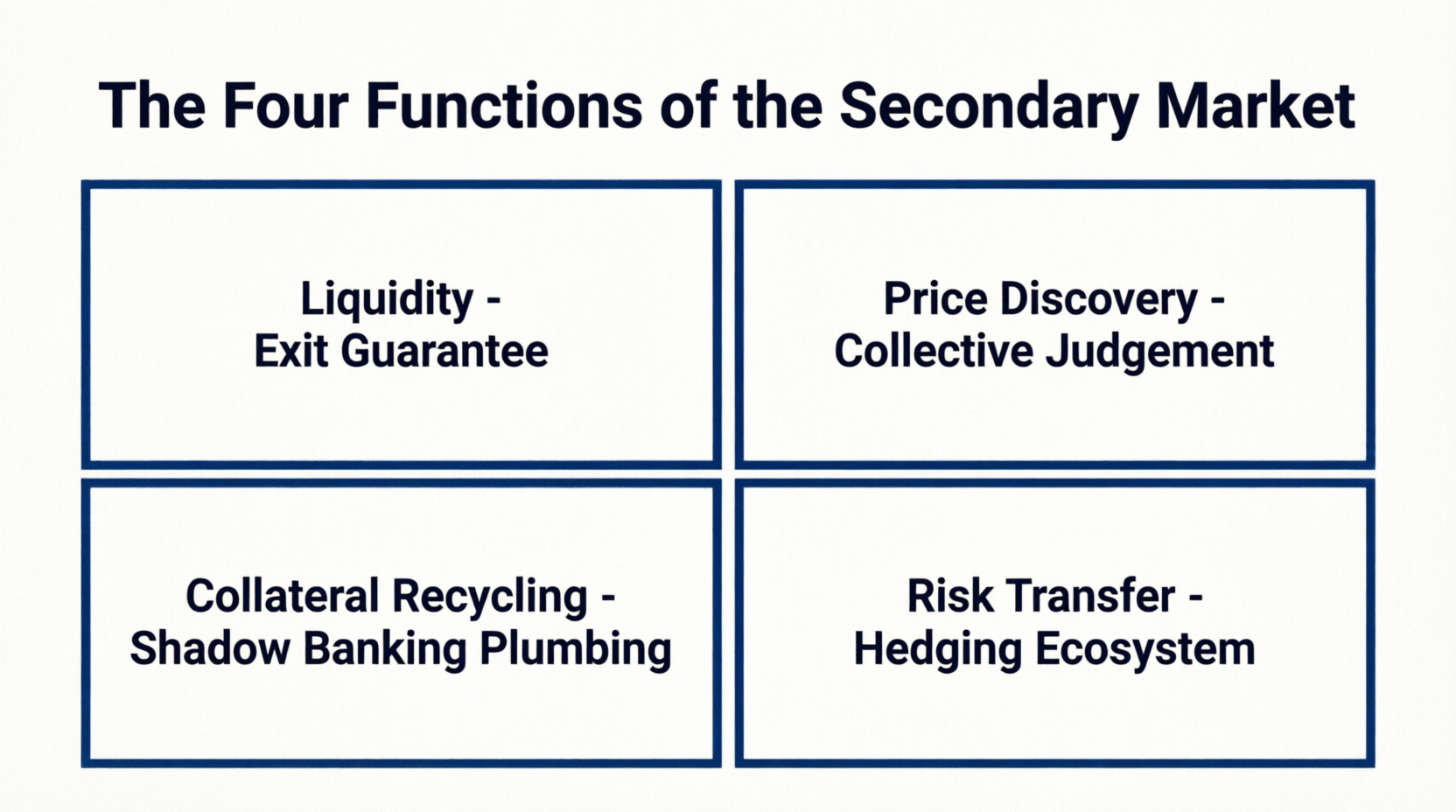

What the Secondary Market Does

The Four Core Functions

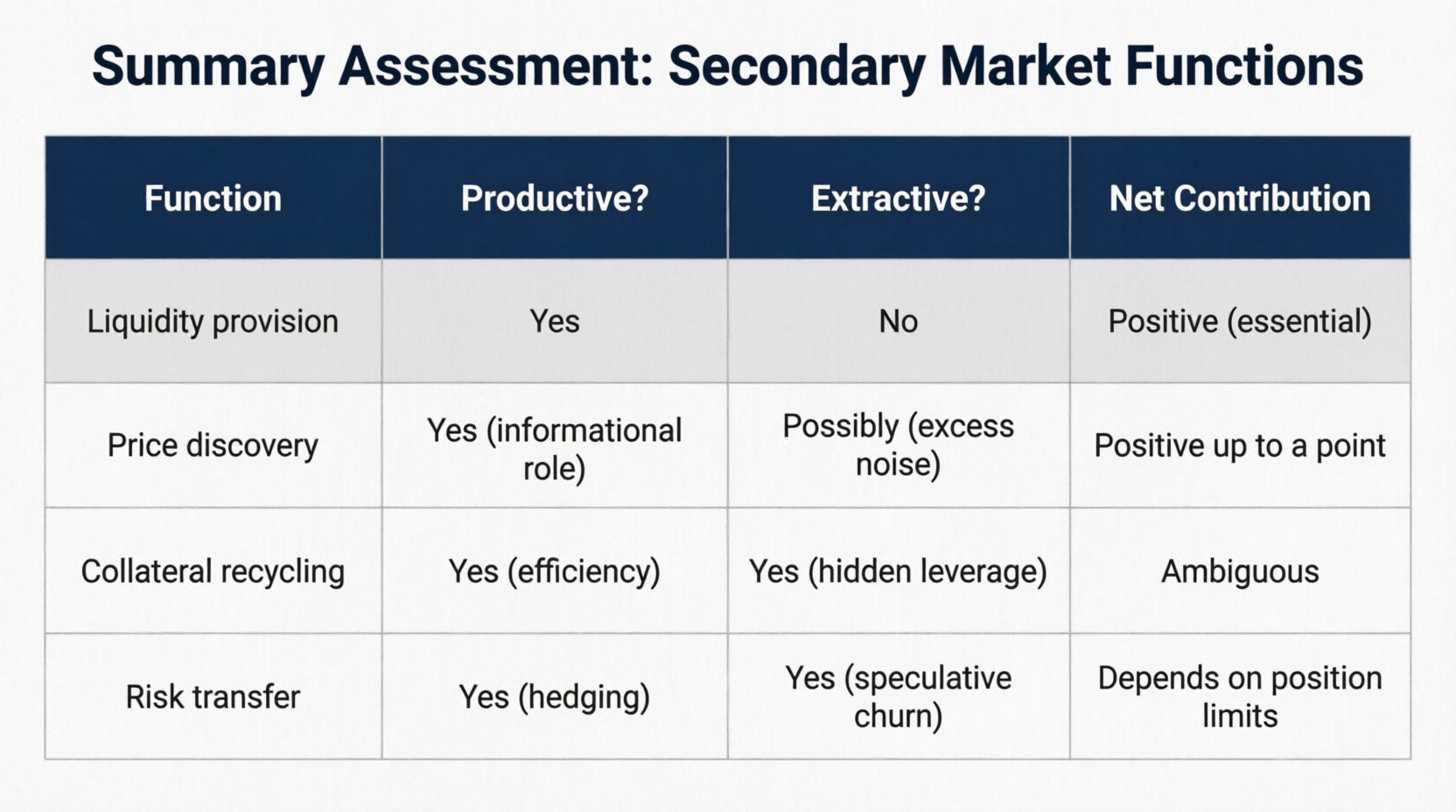

The secondary market performs four distinct economic functions. Understanding each is essential to assessing whether it contributes to or detracts from the real economy.

Liquidity Provision

The Exit Guarantee

The most obvious function of the secondary market is to provide liquidity—the ability to buy or sell an asset quickly without moving its price significantly. As British International Investment notes, “investors are more willing to put money into something when they are confident of being able to take it out again. That is why ‘secondary’ markets, where investors can buy and sell claims in existing investments, are so important”.

This applies as much to a pension fund manager with a £500 million liability-matching mandate as to a retail investor with £10,000 to place in a tax-efficient gilt.

When liquidity functions well, trades occur smoothly, bid-offer spreads are narrow, and large transactions can be executed without destabilising prices. When liquidity fails—as it did during the “dash for cash” in March 2020 and the LDI crisis of September 2022—the consequences can be dramatic. The Bank of England’s analysis found that liquidity in April 2025, while temporarily worsened during a period of heightened global volatility following US tariff announcements, was nevertheless “commensurate with the degree of volatility” and deteriorated “significantly less than other stress episodes” such as 2020 and 2022.

The Bank monitors liquidity using a range of metrics, including bid-offer spreads (the difference between the highest price a buyer is willing to pay and the lowest price a seller is willing to accept), yield curve noise (deviations of yields from a fitted curve, which can indicate reduced willingness to arbitrage dislocations), and Amihud (a measure of price impact per volume traded).

When liquidity fails, the state must intervene—not because the government “needs” the bond market to function, but because the regulatory framework created the dependency. Pension funds, banks, and insurers hold gilts because policy requires it. The state cannot then stand aside when that policy-created demand proves unstable.

Price Discovery

Revealing the Collective Judgement

The second core function of the secondary market is price discovery—the process by which the prices of securities are determined through the interaction of buyers and sellers. The Investopedia definition captures this well: through “a massive series of independent yet interconnected trades, the secondary market steers the price of an asset towards its actual value through the natural workings of supply and demand”.

In the gilt market, price discovery is not a one-time event but a continuous process, unfolding with every trade, every bid-offer spread adjustment, and every algorithmic update. The yield that appears on Bloomberg at 3:45 pm on a Tuesday is the product of thousands of individual judgements about future interest rates, inflation, fiscal policy, and global risk appetite.

The informational role of secondary market prices has been extensively studied in academic literature. A 2025 European Corporate Governance Institute review argues that “accounting for the feedback effect from market prices to the real economy significantly changes our understanding of the price formation process, the informativeness of the price, and speculators’ trading behaviour”. The authors contend that “a new definition of price efficiency is needed to account for the extent to which prices reflect information that is useful for the efficiency of real decisions (rather than the extent to which they forecast future cash flows)”.

This assumes secondary market prices reflect “fundamental value” rather than speculative dynamics, herding behaviour, and regulatory artefacts. The 2022 LDI crisis demonstrated that “price discovery” can become price destruction when leveraged positions unwind. Moreover, from an MMT perspective, gilt yields do not reveal any natural “cost of borrowing”—they reflect a policy choice to offer bonds rather than maintain permanent zero-yielding reserves. The “information” being discovered is partly a fiction of the policy framework itself.

Collateral Recycling

The Hidden Plumbing

Less visible but equally important is the role of the secondary market in facilitating the reuse of gilts as collateral. When a gilt is purchased in the secondary market, it can be used in a repo transaction to raise cash, which can then be used to purchase another gilt, which can be rehypothecated, and so on. This collateral recycling is the plumbing of the shadow banking system.

The Bank of England notes that gilts serve “as a safe and liquid asset for use as collateral or in capital regulatory requirements”. The ability to reuse gilts efficiently reduces funding costs across the financial system. It also creates risks—rehypothecation chains can amplify leverage and create hidden interdependencies—but the efficiency gains are substantial.

This reveals the circularity of the system. The state issues debt to drain reserves, then that debt becomes the collateral that creates private credit in the shadow banking system. The “efficiency gains” accrue to financial intermediaries, while the systemic risks are socialised (as the 2022 intervention demonstrated). This is not a natural market outcome but a policy-architected one.

Risk Transfer

The Hedging Ecosystem

The fourth function is the transfer of risk from those who do not wish to bear it to those who do. A pension fund with long-term liabilities might sell short-dated gilts and buy long-dated gilts to match its duration profile. A hedge fund with a view on interest rates might short gilt futures without ever taking delivery of the physical bond. An insurance company might use inflation swaps to hedge its annuity liabilities.

The derivatives ecosystem that enables this risk transfer is vast. Long gilt futures traded on ICE Futures Europe are “the only actively traded UK bond future,” and liquidity can be tracked “from one second to the next” using order book data. The secondary market in gilts and its derivatives is where risks are priced, packaged, and redistributed across the financial system.

Does the Secondary Market Contribute to the Productive Economy?

This is a central question. The answer is not binary but rests on a distinction between necessary and excessive secondary market activity.

The Virtuous Case

When Secondary Markets Enable Primary Investment

The most straightforward channel through which secondary markets contribute to the real economy is the liquidity-primary market nexus. A liquid secondary market makes primary issuance easier and cheaper because investors know they can exit their positions if needed. Without this exit guarantee, investors would demand a liquidity premium, raising the government’s cost of borrowing.

A Richmond Federal Reserve analysis explains the mechanism: “Features of secondary market trade can increase demand for assets, increasing issuance in the primary market”. The secondary market does not merely facilitate trading in existing assets; it expands the potential size of the primary market.

In emerging markets and developing economies, the importance of secondary markets is even more pronounced. The British International Investment reports that “weak exit routes constrain investment activity in emerging markets and developing economies. Across infrastructure and real estate, project developers struggle to refinance operating assets and release capital for investment in new projects”. Secondary market vehicles such as Infrastructure Investment Trusts (InvITs), YieldCos, and Real Estate Investment Trusts (REITs) “are pooling underlying investments and enabling their sale to new investors,” thereby “encouraging more primary investment by making it easier for them to exit and recycle capital”.

The secondary market, in this virtuous framing, is not an alternative to productive activity but its enabler.

This framing accepts the conventional narrative that government “needs” to attract investors. In reality, the government spends first, creating deposits. Bond issuance is optional—a monetary policy tool to support interest rates, not a fiscal necessity. The “cost of borrowing” is a policy choice: the government could simply maintain reserves at zero yield indefinitely. The secondary market’s “virtuous” role exists only because policy creates the need for it.

The Extractive Critique

Rent-Seeking and Financialisation

The opposing view is that secondary markets have grown far beyond the level that serves productive capital formation and have become extractive rent-seeking mechanisms. The financialisation of the economy—the increasing weight of financial activities relative to real economic activity—has transferred value from productive circuits to unproductive ones.

Richard Murphy, a prominent critic, contends that “most secondary market trading is societally unproductive” and “therefore amounts to rentierism and should be curbed”. His critique rests on the observation that secondary market trades do not directly finance new investment—they simply reshuffle existing ownership claims.

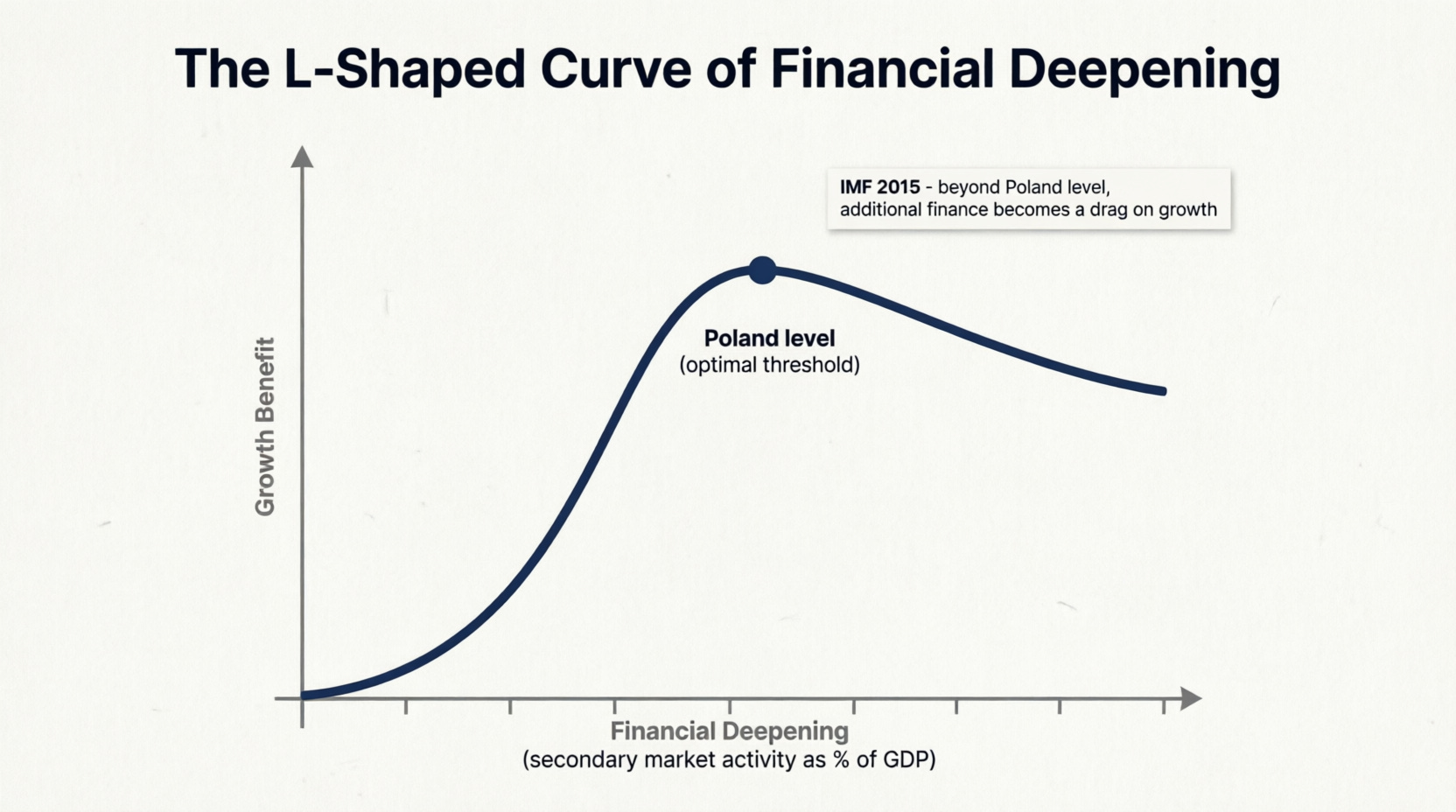

The empirical evidence is more nuanced but troubling for proponents of unlimited secondary market growth. A 2015 IMF paper, Rethinking Financial Deepening, “found that the growth benefits of financial deepening were positive only up to a certain point, and after that point, increased depth became a drag”. Poland was identified as representing “the optimal level of financial ‘deepening’” relative to real economy activity.

In other words, there is an L-shaped curve: up to a certain threshold, more secondary market activity supports growth; beyond that threshold, additional activity becomes detrimental.

The IMF’s findings have been summarised more sharply: “Studies by the IMF and others have found that overly large secondary market trading activity is correlated with lower growth. And ‘overly large’ is not all that big”.

The MMT perspective sharpens this critique. If secondary market activity beyond the optimal threshold reduces growth, and if that activity is policy-created (through regulations requiring gilt holdings, tax advantages for bond ownership, and the decision to issue bonds rather than maintain reserves), then the state is actively choosing to support extractive financialisation. This is not a market failure but a policy failure.

The Informational Channel

Productive Speculation?

A third perspective bridges the two poles. The informational role of secondary markets—the argument that trading reveals information that improves real investment decisions—offers a potential justification for secondary market activity even when it does not directly finance new capital.

The European Corporate Governance Institute review develops this argument systematically: secondary financial markets, “where securities are traded among investors without capital flowing to firms,” can nonetheless have “potential real effects … that stem from the informational role of market prices”.

If stock prices and bond yields reflect fundamental information about company prospects and economic conditions, that information guides the allocation of real resources. A factory built in response to a high stock price, or not built in response to a low one, represents a real effect of secondary market trading—even though the secondary trade itself did not finance the factory.

The authors contend that “accounting for the feedback effect from market prices to the real economy significantly changes our understanding of the price formation process, the informativeness of the price, and speculators’ trading behaviour”. Speculation, on this view, is not necessarily wasteful. Informed speculation improves price informativeness, which improves real decisions.

The critical unanswered question is how much speculation is necessary to achieve adequate price informativeness. If a small amount of secondary trading suffices to produce efficient prices—and if excess trading simply adds noise, volatility, and extraction—then the optimal level of secondary market activity could be far below current levels.

This assumes gilt yields convey useful information about fiscal sustainability or inflation prospects. But yields also reflect: (1) regulatory demand artefacts, (2) speculative herding, (3) central bank intervention expectations, and (4) global risk sentiment unrelated to UK fundamentals. The 2022 crisis showed yields can become disinformative—driven by LDI forced selling rather than fundamental assessment. From an MMT standpoint, the “information” in gilt yields is heavily contaminated by the policy framework itself.

Case Study

The 2022 Gilt Market Crisis

No examination of secondary market functionality is complete without an analysis of the 2022 Liability-Driven Investment (LDI) crisis. This episode provides a vivid illustration of both the essential role of secondary markets and the catastrophic consequences when liquidity fails.

Anatomy of a Liquidity Crunch

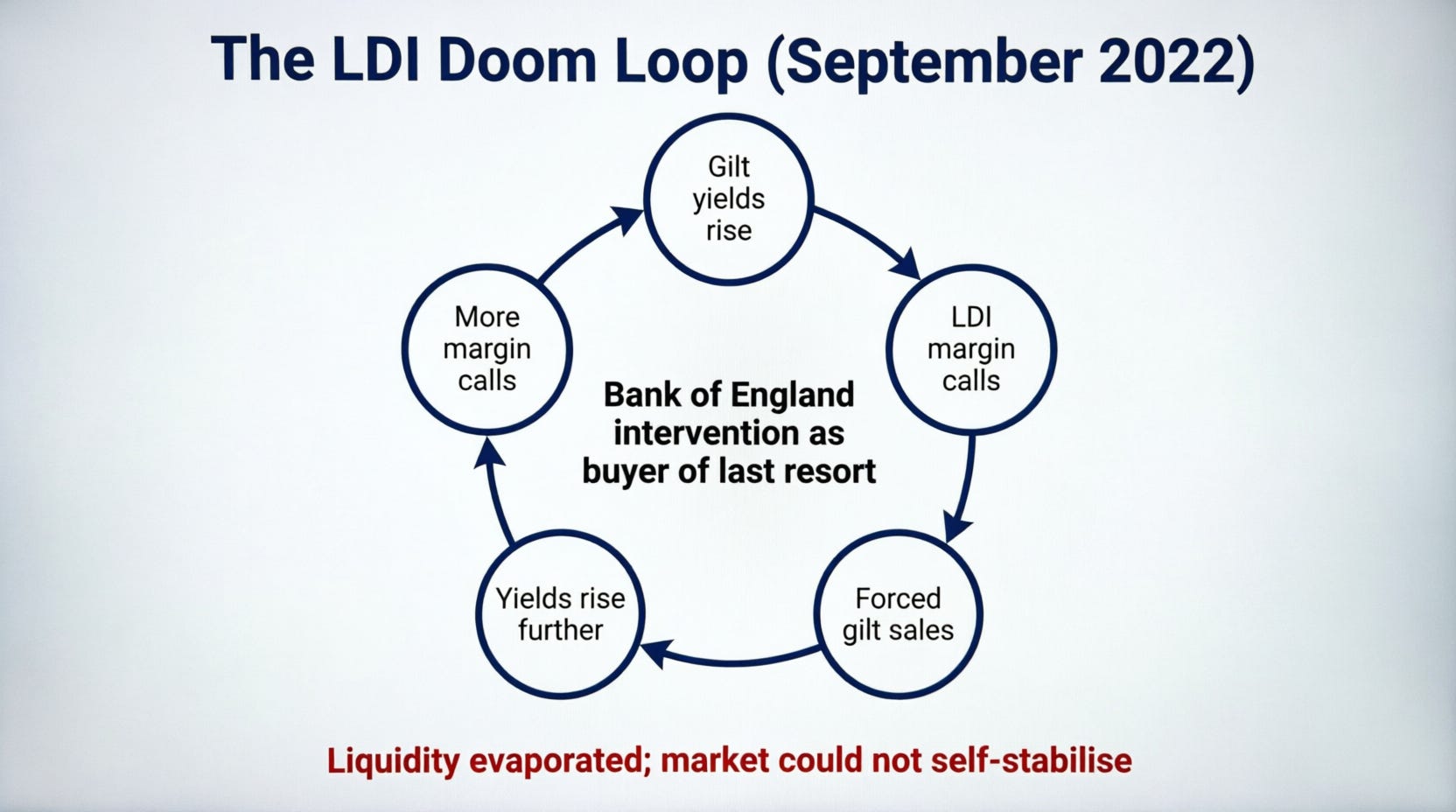

The crisis began in late September 2022 following the UK government’s “mini-budget”—a package of unfunded tax cuts announced without independent fiscal assessment. The Bank of England’s detailed analysis, published in March 2023, identifies the mechanism: “selling pressure in gilt markets – due to deteriorating derivative and repo positions of liability-driven investors (LDI) – led to evaporating market liquidity, especially in long-dated conventional gilts and index-linked gilts”.

LDI funds, which used derivatives to hedge pension scheme liabilities, faced margin calls as gilt yields surged. Forced selling of gilts to meet these calls drove yields higher still, triggering further margin calls—a classic “doom loop.” Total net sales of gilts between 23 September and 14 October exceeded £36 billion.

The crisis was not a failure of the secondary market per se—the market was, after all, still trading—but a failure of the market’s ability to intermediate large forced sales without price dislocation. The Bank of England was ultimately forced to intervene as a buyer of last resort.

What the Crisis Reveals About Secondary Markets

Three lessons from the 2022 episode are relevant to the productive versus extractive question.

First, secondary markets can amplify rather than absorb shocks when leveraged positions unwind simultaneously. The same liquidity that facilitates normal trading can vanish during stress, as bid-offer spreads widen and market depth evaporates.

This is not a “market failure” but an inherent feature of leveraged financial markets. The state created the regulatory framework that encouraged LDI strategies (requiring pension funds to hedge liabilities), then created the gilt supply that became the collateral for those strategies, then had to intervene when the strategies failed. This is policy-created fragility, not exogenous market dysfunction.

Second, the distinction between productive and unproductive speculation is not always clear. The LDI strategies that triggered the crisis were intended to serve a productive purpose—enabling pension funds to match their long-term liabilities efficiently. Yet those same strategies created fragility that threatened the entire financial system.

Third, the secondary market does not self-correct in times of extreme stress. The Bank of England’s intervention was necessary not to override the market but to prevent its collapse. The secondary market governs yields most of the time, but when it fails, the state—not HM Treasury directly, but the Bank of England—must step in.

This reveals the ultimate operational reality: the state is always the backstop. If the secondary market cannot function, the central bank intervenes. If pension funds become insolvent, the Pension Protection Fund (backed by the state) steps in. If inflation spikes, fiscal policy can adjust. The “bond vigilantes” cannot actually stop government spending—they can only make it politically costly via higher nominal yields. But from an MMT perspective, nominal yields are not the real constraint; inflation and real resource availability are.

Policy Implications

Can We Tame the Secondary Market Without Breaking It?

If secondary markets have both essential functions and extractive tendencies, the policy question is whether they can be regulated to preserve the former while curbing the latter.

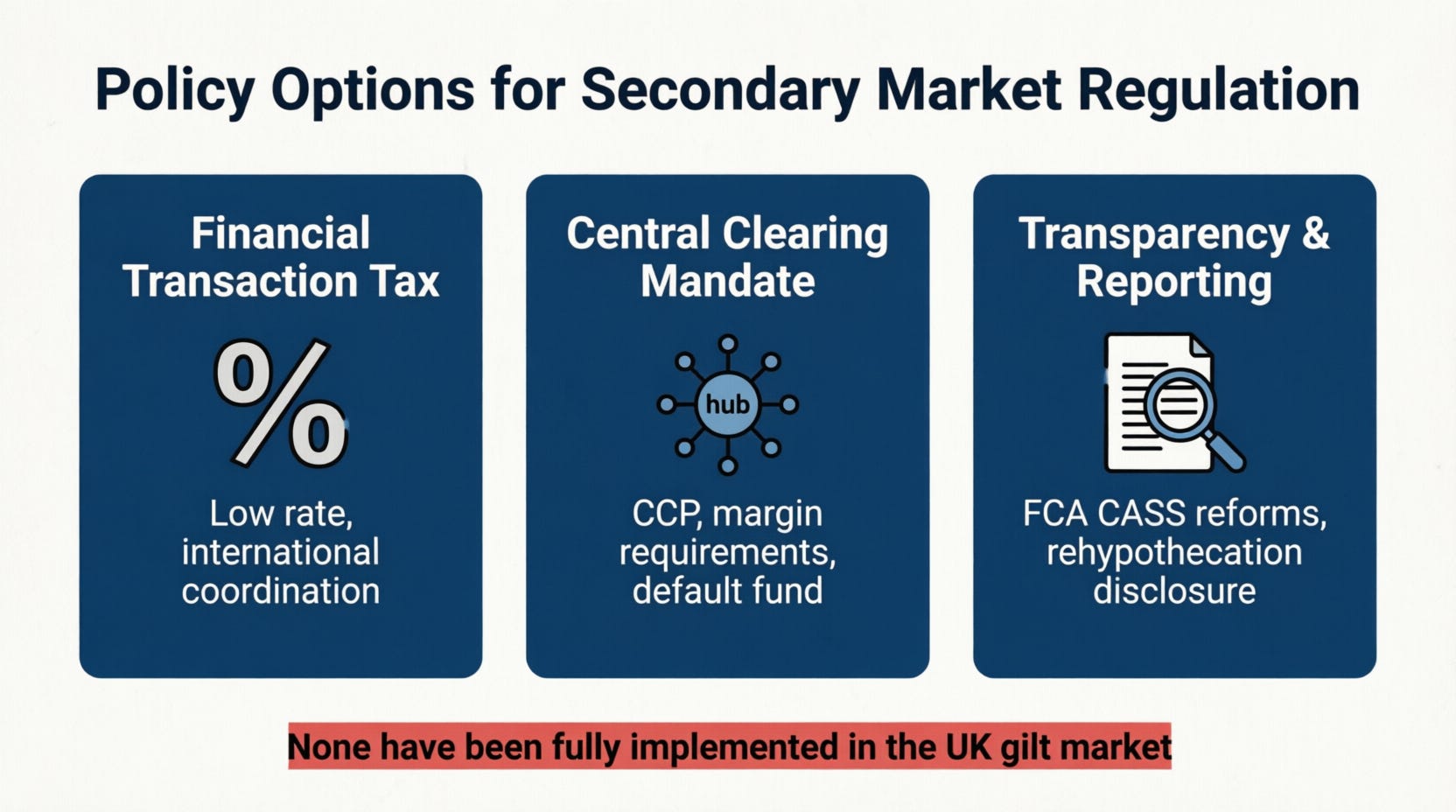

Financial Transaction Taxes

One frequently proposed remedy is a financial transaction tax (FTT) on securities trades. The theoretical case rests on the observation that trading can be a rent-seeking activity. Academic research has shown that “taxes on trading can reduce rent-seeking behaviour when agents engage in a ‘race’ to obtain private information earlier than others” and “can lead to greater firm values”.

The UK Treasury has historically resisted FTT proposals, citing concerns about driving trading activity offshore. Proponents counter that a well-designed FTT could be coordinated internationally (the EU has debated such a tax for years) and that even a very low rate—a few basis points—could reduce high-frequency arbitrage without impairing essential liquidity.

An FTT would reduce secondary market churn, which aligns with the IMF’s finding that excess financial deepening reduces growth. However, it would not address the operational issue that gilt issuance itself is optional. A more fundamental MMT-aligned reform would be to reduce gilt issuance and maintain larger reserve balances, shrinking the secondary market’s scope entirely.

Central Clearing Mandates

The Bank of England’s 2025 discussion paper on gilt repo market resilience explores mandatory central clearing as a tool to reduce counterparty risk and limit the build-up of hidden leverage in rehypothecation chains. Central clearing would bring secondary market transactions into a regulated CCP environment with transparent margin requirements and mutualised default funds.

The industry response has been mixed. ICMA “strongly opposes the suggestion of mandatory clearing for gilt repo” on grounds that “this would increase costs and restrict access for some participants” and that “clearing should be a commercial choice”. The BoE’s April 2026 Feedback Statement acknowledged this resistance while affirming that “further action is needed to deliver structural improvements to the resilience of the gilt repo market”.

Transparency and Reporting

A third approach is increased transparency—requiring more detailed reporting of secondary market transactions, short positions, and rehypothecation chains. The FCA’s consultation on Client Assets (CASS) reforms (CP25/37), published in December 2025, proposes “clearer expectations for firms that hold client money or safe custody assets” but stops short of imposing US-style quantitative limits on rehypothecation.

All three approaches tinker at the margins of a policy-created system. The more fundamental MMT question is: why issue so many bonds in the first place? If the secondary market is too large, too leveraged, and too extractive, the solution is not merely to regulate it better but to shrink it by reducing gilt issuance and maintaining larger reserve balances. The constraint is inflation, not bond market access.

The HM Treasury Disconnect

Why Yields Are Not a Policy Tool

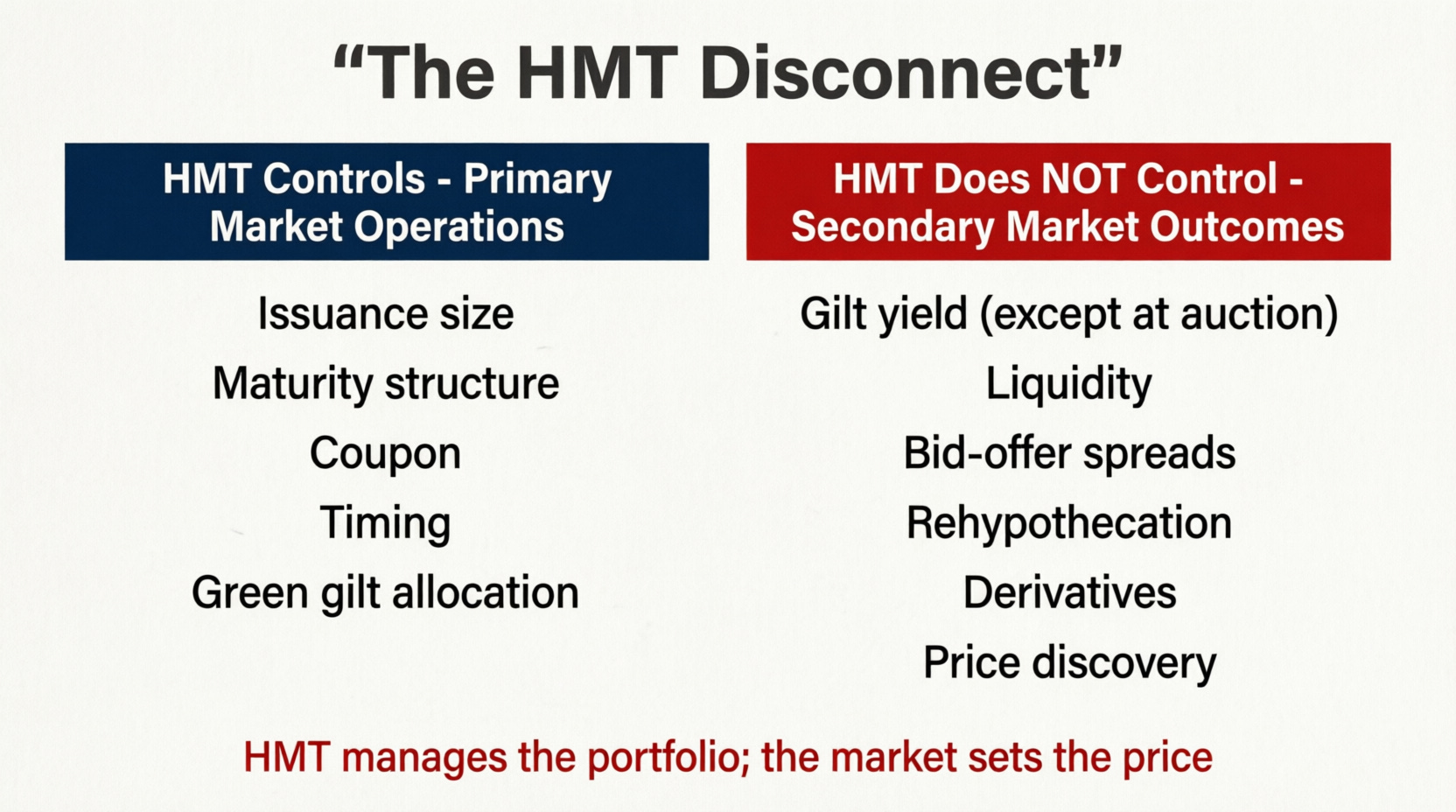

The unifying theme across this article—and the reason it appears in this series on gilt yields—is that HM Treasury does not control the yields that emerge from secondary trading. This is not a design flaw; it is a structural feature of modern sovereign debt markets. But it has profound implications for economic governance.

What HMT Controls vs What It Does Not

HM Treasury, through the DMO, controls:

The size of the gilt issuance programme

The maturity structure of new issuance (short, medium, long, index-linked)

The coupon offered at auction

The timing of auctions and syndications

The green gilt allocation (subject to demand and market conditions)

The DMO’s statutory debt management objective is “to minimise, over the long term, the costs of meeting the government’s financing needs, taking into account risk, while ensuring that debt management policy is consistent with the aims of monetary policy”. HM Treasury, on this framing, manages the portfolio—not the price.

This objective accepts the conventional framing that government “needs” to “meet financing needs” via bond markets. In operational reality, spending creates deposits; bond issuance drains them. The objective should be reframed as “to manage the monetary consequences of fiscal operations while supporting monetary policy objectives.”

HM Treasury does not control:

The yield at which any gilt trades after its first day of secondary trading

The liquidity of the secondary market

The bid-offer spreads that determine transaction costs

The rehypothecation chains that collateralise gilts across the shadow banking system

The derivatives positions that amplify or hedge gilt exposures

The price discovery process that aggregates market participants’ judgements

The distinction is absolute. The DMO’s auction sets the starting price; the secondary market sets every subsequent price.

The Bond Vigilante Thesis

The “bond vigilante” concept, coined in the 1980s, captures the idea that secondary market participants can punish perceived fiscal profligacy by driving yields higher—selling or refusing to buy government debt in sufficient quantity to raise borrowing costs. The vigilante model was dramatised during the Clinton administration, resurfaces periodically, and operates without any statutory authority.

The critical point for this article is that bond vigilantes are not elected, not accountable, and not licensed by HM Treasury. They are private market participants acting on their own judgements and interests. Their collective action determines gilt yields. HM Treasury’s response is necessarily reactive—it can adjust issuance strategy, extend maturities, or communicate fiscal discipline, but it cannot directly override the vigilantes’ verdict.

MMT demolition of the vigilante thesis:

This arrangement has defenders and critics. Defenders argue that market discipline imposes a necessary constraint on fiscal policy. Critics argue that unaccountable vigilantes can force pro-cyclical austerity, amplify economic downturns, and impose costs on future generations who have no vote in current fiscal debates.

But from an MMT perspective, the entire vigilante narrative rests on a category error:

Operational impossibility: Bond vigilantes cannot prevent government spending. When the government spends, the Bank of England credits accounts. Full stop. Vigilantes can only affect the interest rate offered on bonds after spending has occurred.

The central bank backstop: If vigilantes drive yields “too high,” the Bank of England can intervene via QE or yield curve control. The 2022 crisis proved this: when yields spiked, the BoE had to intervene. The vigilantes were stopped by the state.

The policy choice: The government can choose not to issue bonds. It can maintain permanent zero-yielding reserves. The “cost of borrowing” is thus a policy decision, not a market imperative.

The real constraint: The actual limit on spending is inflation and real resource availability, not bond market access. If the economy is at full capacity, spending more will be inflationary—regardless of what bond yields do. Conversely, if there is slack, spending can increase without inflation—again, regardless of bond yields.

The distributional effect: High yields transfer income from taxpayers to bondholders (typically wealthier households and overseas investors). This is a distributional choice, not an economic necessity.

The vigilante cannot stop the sovereign currency issuer. The vigilante can only make the political cost of spending higher via nominal yield increases. But the operational capacity to spend is unaffected.

In Conclusion

Infrastructure First, Extraction Second—but the Balance Is Not Fixed

The secondary gilt market in the United Kingdom is neither a purely productive infrastructure nor a purely extractive machine. It is both—and the balance between these two natures is not fixed but subject to change based on regulation, market structure, and the behaviour of participants.

The productive case for secondary markets rests on three pillars: liquidity for primary issuance, price discovery for efficient capital allocation, and collateral recycling for financial system functioning. Without these functions, the government would pay significantly more to borrow, corporations would face higher costs of capital, and the financial system would operate with greater friction.

This accepts the conventional narrative. Reframed: secondary markets exist because policy creates them. The government could spend without issuing bonds. The “cost savings” from liquid secondary markets are self-imposed—the result of choosing to issue bonds rather than maintain reserves. This is not inherently wrong, but it should be recognised as a policy choice, not an economic necessity.

The extractive case against oversized secondary markets rests on the IMF’s empirical finding that “overly large secondary market trading activity is correlated with lower growth” and that the growth benefits of financial deepening “were positive only up to a certain point”. Beyond this threshold, additional secondary market activity—speculative churn, high-frequency arbitrage, rent-seeking intermediation—siphons value from productive investment without generating offsetting real benefits.

The 2022 LDI crisis demonstrated that the secondary market is not self-correcting. When leveraged positions unwind simultaneously, liquidity can evaporate, and the state must intervene. This is not an argument for abolishing secondary markets—the crisis would have been worse without them—but it is an argument for regulation that preserves liquidity while curbing fragility.

The crisis proved that the state is always the backstop. If the secondary market is systemically important, it must be systemically regulated—or systemically reduced. The MMT policy prescription is clear: if secondary markets are too large, too extractive, and too fragile, shrink them by reducing gilt issuance and maintaining larger reserve balances. The constraint is inflation, not bond market access.

The policy implications are clear but contested. Financial transaction taxes could reduce rent-seeking churn but risk driving trading offshore. Central clearing mandates could reduce hidden leverage but face industry resistance. Transparency reforms could improve oversight but have been slow to materialise.

Rather than tinkering at the margins, ask the fundamental question: how much bond issuance is actually necessary? The answer is: only enough to support the monetary policy interest rate target. Everything beyond that is optional—and potentially extractive.

The fundamental constitutional reality that HM Treasury does not control the secondary market—that yields emerge from decentralised, unaccountable, private trading—is not a bug. It is the intended design of modern sovereign debt markets. The question is not whether this design should be overturned—that is practically impossible—but whether it should be bounded, regulated, and made more transparent. The secondary market governs yields; the question for democracy is how the market itself should be governed.

The deeper question is whether we should accept a system in which unaccountable private actors determine the cost of public debt. The operational reality is that the state could spend without bond market approval. The political choice to maintain the current system should be recognised as a choice—not as an economic necessity.

In the next article in this series, we examine the derivatives ecosystem—futures, options, swaps, and STRIPS—that further distances the realised cost of government borrowing from anything HM Treasury directly controls. The vigilantes, as it turns out, have many weapons.

And the state has the ultimate weapon: the power to not play the game. The question is whether it has the political will to use it.

Post Script

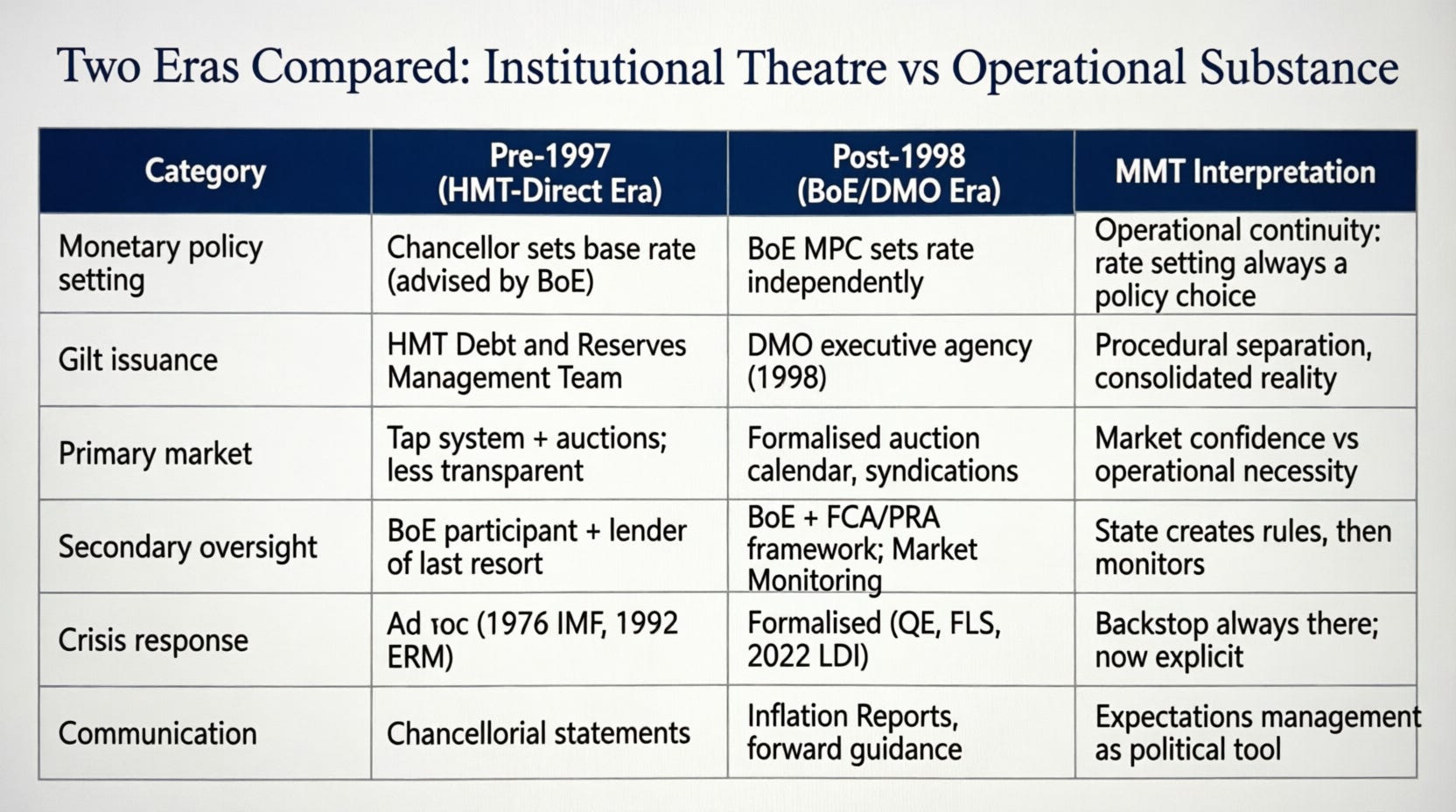

Bank of England Independence and the formation of Debt Management Office

What Changed (and Why It Matters)

1. The credibility narrative Post-1997 reforms were explicitly designed to “depoliticise” monetary policy and debt management — to signal to markets that inflation control and gilt issuance would not be subject to short-term electoral cycles. From a conventional perspective, this lowered risk premia and reduced borrowing costs.

This conflates political credibility with operational capacity. The UK government could always service sterling-denominated debt regardless of institutional arrangements. The reforms may have altered market perceptions of inflation risk, but they did not change the operational reality that spending creates deposits and bond issuance drains them. The “credibility dividend” is real in terms of market psychology, but it is a political achievement, not an economic necessity.

2. The separation of monetary and fiscal operations Pre-1997, the Treasury directly managed both spending and debt issuance, with the BoE acting as its banker. Post-reform, the BoE sets interest rates independently, while the DMO manages gilt issuance under HMT’s strategic direction.

This separation is institutional theatre with real political consequences, but limited operational impact. The consolidated government sector (HMT + BoE + DMO) still:

Credits bank accounts when it spends

Debits them when it taxes

Offers bonds as an interest-bearing alternative to reserves

The “independence” of the BoE means it can choose not to monetise deficits directly, but it cannot prevent the government from spending. The operational sequence remains: spend first, then decide whether to issue bonds or leave reserves in the system.

3. Crisis management: from ad hoc to institutionalised The 1976 IMF crisis saw the Treasury negotiating directly with international creditors under intense market pressure. The 2022 LDI crisis saw the BoE intervene within days using pre-announced facilities, with clear communication about the temporary, targeted nature of support.

Both episodes reveal the same underlying truth: the state is the ultimate backstop. The difference is that post-reform architecture makes this backstop more transparent — and therefore more politically accountable. The 2022 intervention was criticised by some as “fiscal dominance”; MMT would frame it as the state managing the consequences of its own regulatory framework (which encouraged LDI strategies).

4. Market expectations as a policy variable Pre-1997, market reactions to fiscal announcements were often volatile and unpredictable. Post-reform, the combination of BoE independence, DMO transparency, and inflation targeting has created a more predictable environment — at least in normal times.

Predictability is valuable, but it should not be mistaken for constraint. The government can still spend regardless of market expectations; what changes is the political cost of doing so. High yields increase debt service costs, which may force political choices about taxation or spending priorities — but they do not create an operational barrier to expenditure.

The Unchanged Core: Operational Sovereignty

Despite two decades of institutional reform, three operational realities persist:

Spending precedes revenue — The government credits accounts when it spends; taxes and bond issuance follow. This sequence is unchanged by who presses the buttons.

The consolidated government sector — HMT, BoE, and DMO are all part of the same sovereign currency-issuing entity. Transfers between them are accounting entries, not resource constraints.

The real constraint is inflation — Not bond yields, not credit ratings, not “market confidence”. If the economy is at full capacity, additional spending will be inflationary regardless of institutional arrangements. If there is slack, spending can increase without inflation — again, regardless of the institutional setup.

A Thought Experiment: What If We Reversed the Reforms?

Suppose tomorrow the government announced:

Reunification of monetary policy setting within HMT

Dissolution of the DMO as a separate executive agency

Direct BoE financing of deficits (abolishing the “no monetary financing” rule)

Conventional view: Market panic, sterling collapse, yield spike, inflation surge.

MMT view: Operational capacity unchanged. The political consequences could be significant (loss of credibility, capital flight), but the operational ability to spend, tax, and issue bonds in sterling would be unaffected. The key question would be whether the new institutional arrangement better serves the public purpose — full employment, price stability, equitable distribution — not whether it “pleases the markets”.

Final Word

The post-1997 architecture represents a political choice to delegate certain functions to technically independent bodies, with the aim of enhancing credibility and reducing short-term political interference. From an MMT perspective, this choice is legitimate — but it should be recognised as a choice, not as an economic imperative.

The operational reality — that the UK government, as issuer of its own currency, faces no financial constraint on spending — remains unchanged. What has changed is the political economy: who gets to decide, who gets blamed, and how policy choices are communicated to markets and the public.

In that sense, the gilt market’s secondary trading ecosystem — with all its complexity, fragility, and extractive potential — operates within a framework that the state created and can, if it chooses, reform. The vigilantes may have many weapons, but the sovereign currency issuer holds the ultimate card: the power to change the rules of the game.

The question is not whether the post-1997 settlement is “right” or “wrong”, but whether it continues to serve the public purpose in a world of heightened financial fragility, climate urgency, and distributional tension. From an MMT standpoint, that assessment should be based on real outcomes — employment, inflation, inequality — not on whether bond yields please an unaccountable market.

References

Bank of England (2025a) Enhancing the resilience of the gilt repo market – discussion paper feedback statement. 1 April 2026. Available at: https://www.bankofengland.co.uk

Bank of England (2025b) Gilt market liquidity in April 2025. 25 September 2025. Available at: https://www.bankofengland.co.uk

Bank of England (2025c) Financial Stability Report, July 2025. London: Bank of England. Available at: https://www.bankofengland.co.uk/financial-stability-report

Bank of England (2025d) A well-functioning gilt repo market enhances the liquidity and resilience of the cash gilt market, thereby supporting government financing, the transmission of monetary policy, and sustainable economic growth. Discussion paper, September 2025. Available at: https://www.investing.com

British International Investment (no date) About secondary markets. Available at: https://www.bii.co.uk

Butt, N. (2024) ‘Market resilience, non-bank financial institutions and the central bank toolkit – practical next steps’, Speech at London School of Economics, 12 March 2024. Available at: https://www.bankofengland.co.uk/speech/2024/march/market-resilience-non-bank-financial-institutions-and-the-central-bank-toolkit

Debt Management Office (2025) Record of consultations with gilt market participants. 2 December 2025. Available at: https://www.dmo.gov.uk

Euromoney (2022) ‘The bond vigilantes are back with a vengeance’, Euromoney, 13 October. Available at: https://www.euromoney.com

Foulger, L. (2025) ‘Strengthening market resilience: navigating evolving dynamics in sovereign markets’, Speech at AFME’s 20th Annual European Government Bond Conference, 12 November 2025. Available at: https://www.bankofengland.co.uk/speech

Hail, S. (2025) Cited in ‘Financial markets cannot punish a sovereign government. Here’s why’, Economic Reform Australia, 1 November. Available at: https://www.era.org.au

HM Treasury and Debt Management Office (2025) Debt Management Report 2025-26. 2 April 2025. London: HM Treasury. Available at: https://www.gov.uk/government/publications/debt-management-report-2025-26

HM Treasury and Debt Management Office (2026) Debt Management Report 2026-27. 11 March 2026. London: HM Treasury. Available at: https://www.gov.uk/government/publications/debt-management-report-2026-27

International Capital Market Association (no date) Secondary markets, repo & collateral. Available at: https://www.icmagroup.org

Investopedia (no date) Secondary market: definition, types, and examples. Available at: https://www.investopedia.com

Mitchell, B. (2010) ‘Saturday Quiz – September 18, 2010 – answers and discussion’, Billy Blog, 19 September. Available at: https://www.billmitchell.org/blog

Mitchell, B. (2019) ‘On money printing and bond issuance – Part 2’, Billy Blog, 27 August. Available at: https://www.billmitchell.org/blog

Murphy, R. (2023) ‘In a financialised economy raising interest rates actually causes inflation’, 23 June. Available at: https://markcarrigan.net

Murphy, R. (2025a) ‘The curse of the household analogy’, Naked Capitalism, 24 January. Available at: https://www.nakedcapitalism.com

Murphy, R. (2025b) ‘The UK is cursed: how finance destroyed our economy’, FeeOnlyNews.com, 29 November. Available at: https://www.feeonlynews.com

Murphy, R. and Christensen, J. (2026) ‘The finance curse is killing Britain’, Funding the Future podcast, 11 February. Available at: https://www.nakedcapitalism.com

Sahay, R., Čihák, M., N’Diaye, P., Barajas, A., Ayala Peña, D., Bi, R., Gao, Y., Kyobe, A., Nguyen, L., Saborowski, C., Svirydzenka, K. and Yousefi, S.R. (2015) Rethinking financial deepening: stability and growth in emerging markets. IMF Staff Discussion Note SDN/15/08. Washington, D.C.: International Monetary Fund. Available at: https://www.imf.org/external/pubs/ft/sdn/2015/sdn1508.pdf

Sky News (2022) ‘UK has lost credibility among investors and the “bond vigilantes” serve as a warning’, Sky News, 18 October. Available at: https://news.sky.com

Yardeni, E. (1980s) Cited in ‘Excell with Options: Do JPY and GBP have a similar set-up with different outcomes?’, CME Group, 1 November 2022. Available at: https://www.cmegroup.com

Clearly you know your onions Michael! Much of the discussion of the bond market by media, think tanks, and politicians ignores or fudges the existence of two markets – primary and secondary. They think of the secondary market players as investors in government debt, thereby being essential to the funding of government spending.

In that mode of thinking, we can say that significant breaches of the full funding rule occur given the extended periods of QE where the Bank buys back bonds from the "investors".

This is not the case as far as the DMO is concerned. It continues to meet its obligations, but reserves are returned to the "investors" regardless of the claim that the Bank is independent.

Is that a fair argument?