Gilt Derivatives

The Alchemy That Splits, Hedges, and Amplifies Gilt Yields

The yield you see is not the yield you get (and why HM Treasury has no seat at this table)

The Promise That Was Never Simple

To the uninitiated, a gilt is a simple promise: pay 2% each year for ten years, then return the principal. This is the image cultivated by the Debt Management Office’s auction calendars, by the Chancellor’s references to “the cost of government borrowing”, and by the financial pages that report the daily movement of the 10-year gilt yield. It is an image that is almost entirely misleading.

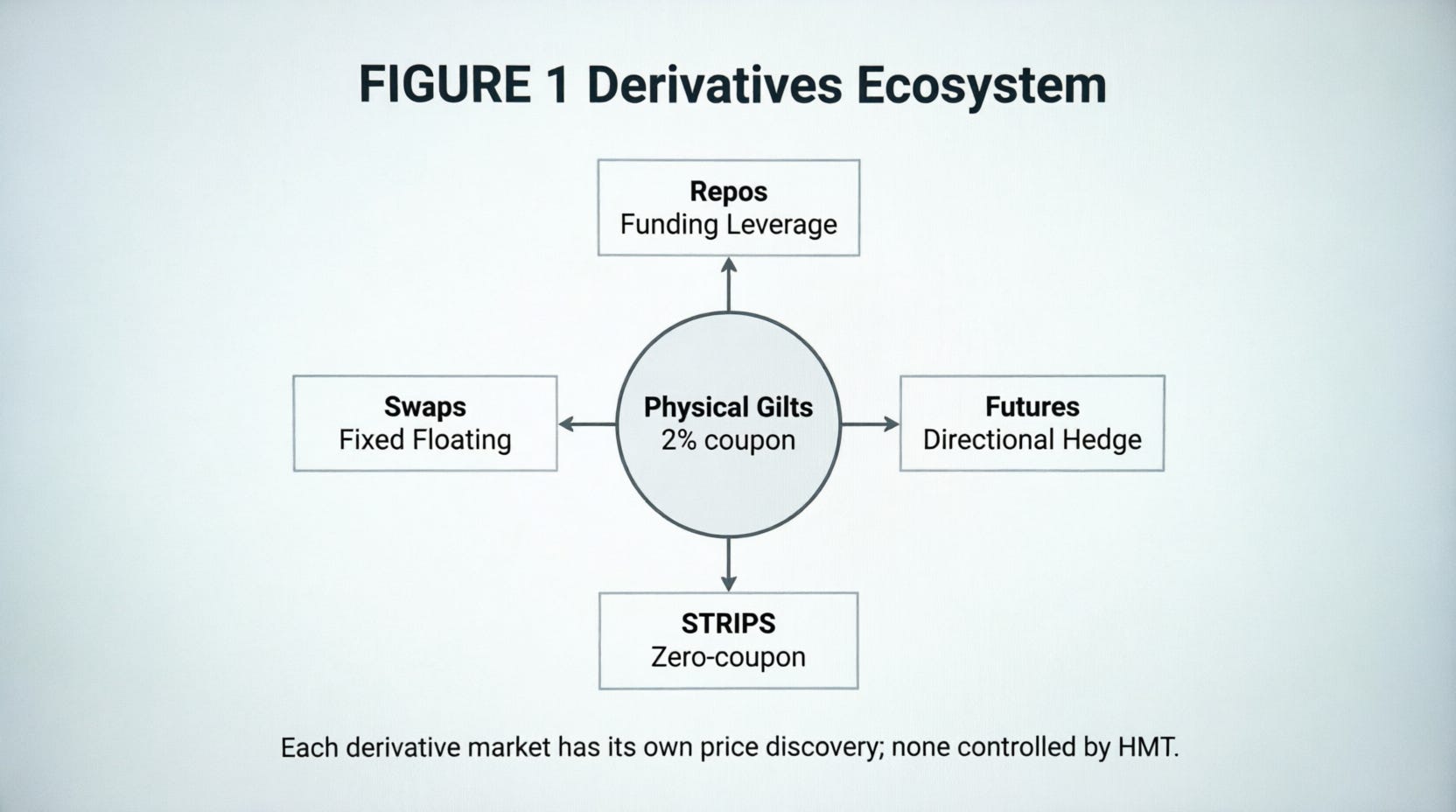

In the secondary market, that simple promise is torn apart, recombined, and used as raw material for a vast ecosystem of derivatives. These instruments – repos, futures, options, swaps, and STRIPS – are not esoteric sideshows. They are the engines of price discovery, the plumbing of the shadow banking system, and the vehicles through which billions of pounds of leveraged speculation flow daily. They also demonstrate, perhaps more clearly than any other feature of the gilt market, that the yield which matters for government borrowing is not set by HM Treasury but emerges from a decentralised, unaccountable, and increasingly algorithmic bazaar.

This separation is not accidental. It is the result of deliberate policy choices to delegate yield determination to private actors while maintaining the fiction that markets “fund” government spending. Operationally, the state spends first, creating reserves. Derivatives then speculate on the interest rate the central bank chooses to pay on those reserves. The entire edifice rests on policy decisions, not economic necessity.

This article explores four derivative instruments in depth: repos (which we have examined previously), gilt futures, STRIPS, and swaps. For each, we ask: what does it do? How does it contribute to the separation of yields from primary issuance? And does this activity serve the productive economy, or is it extractive? We then examine the 2022 Liability-Driven Investment (LDI) crisis as a case study of derivative-amplified fragility, consider what Modern Monetary Theory (MMT) makes of all this, and conclude with the policy implications of a market that HM Treasury cannot control but whose outcomes it must live with.

What Derivatives Are

A Functional Taxonomy

Before analysing the implications, we must understand what derivatives are and what they do. A derivative is a financial contract whose value is derived from an underlying asset – in this case, a gilt. The definitional point is important: derivatives do not represent ownership of the underlying gilt.

They represent a bet on, or a hedge against, a future movement in its price, yield, or associated interest rate.

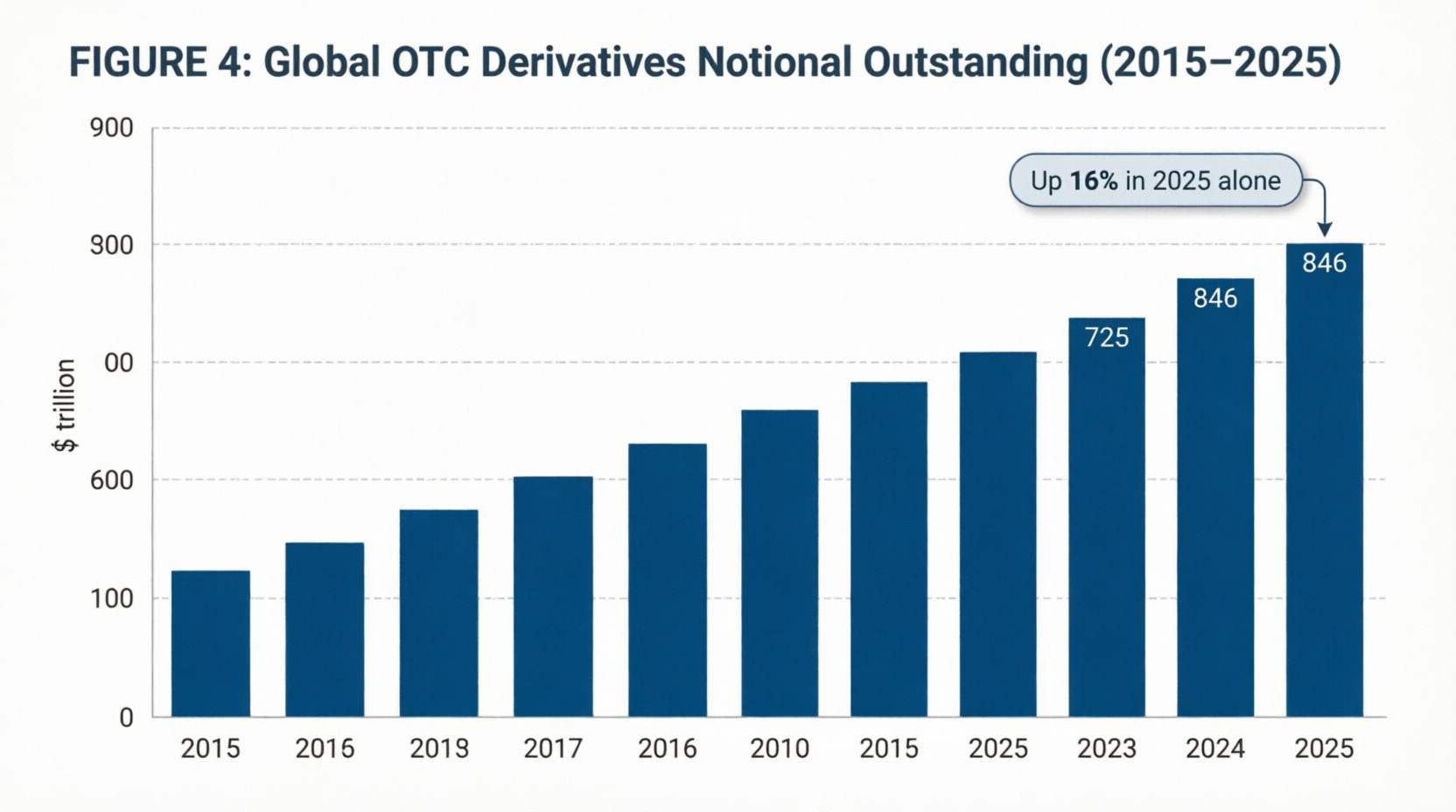

The Bank for International Settlements (BIS) reported that the notional value of outstanding over-the-counter (OTC) derivatives rose to $846 trillion by June 2025, up 16% from June 2024. Global OTC derivatives notional outstanding grew by 15.9% in the first half of 2025 compared to the same period in 2024. The gilt derivatives market is a significant component of these totals.

The Bank of England’s 2025 Financial Stability Report noted that net gilt repo positioning reached its highest level since data collection began in 2017, with borrowing concentrated among a relatively small number of firms. In November 2025, hedge fund net gilt repo borrowing rose to a fresh record near £100 billion. The Bank of England’s 2025 discussion paper noted that daily average gilt repo

volumes reached around £250 billion in the first quarter of 2025, approximately 65% higher than 2018 levels.

The scale is staggering. Primary gilt issuance in a full year is approximately £300 billion. Daily secondary and derivative trading volumes are larger than an entire year’s primary issuance. HM Treasury is present for the auction; it is absent for everything that follows.

This vast derivatives superstructure is built on top of what is, operationally, a simple accounting relationship: the government credits accounts when it spends, debits them when it taxes, and offers bonds as an interest-bearing alternative to reserves. The derivatives market speculates on the interest rate differential – a differential that the central bank chooses to maintain. None of this is operationally necessary; all of it is politically contingent.

Gilt Repos

Funding, Leverage, and the Basis Trade

Gilts relevance here is as a derivative-like instrument that enables funding and leverage. The Bank of England has noted that leveraged hedge fund borrowing in gilt repo markets reached close to £100 billion in November 2025, and that this activity is related, at least in part, to the popularity of the cash-futures basis trade.

The basis trade – arbitraging small price differences between cash gilts and gilt futures – has become a significant source of systemic vulnerability. UK regulators have sounded the alarm over a sharp rise in leveraged hedge fund positions in the gilt market, warning of potential systemic risks if trades unwind suddenly. Foreign hedge funds now account for around 30% of gilt trading, up from 15% in 2018, with basis trades financed via repo markets. The Bank of England warned in July 2025 that UK bonds risk being hit by a wave of forced selling by highly leveraged hedge funds, with hedge funds borrowing a record £77 billion via gilt repo agreements to add leverage to relative value strategies including the basis trade.

The growth has been explosive. Data shows that UK hedge fund net repo leverage positions surged from £4 billion at the beginning of 2024 to £61 billion by March 2025, the highest since 2017.

The basis trade exploits a price discrepancy that exists only because the state chooses to issue bonds rather than maintain permanent zero-yielding reserves. The “arbitrage” is not discovering any fundamental value; it is gaming a policy-created spread. When the trade unwinds, the state must intervene – not because the government “needs” the bond market to function, but because the regulatory framework created the dependency.

Gilt Futures

The Benchmark for the Yield Curve

Gilt futures are standardised exchange-traded contracts that obligate the buyer to purchase, and the seller to deliver, a notional gilt at a future date. ICE Futures Europe lists futures contracts on 2-year, 5-year, 10-year, and 30-year gilts. The ICE 10-year Long Gilt futures contract is described by the exchange as “the market benchmark for the 10-year segment of the UK sovereign yield curve” and “a highly liquid contract” that enables market participants to “trade curve basis, when used in conjunction with the 2, 5 and 30-year Gilt futures”.

The contract specifications are precise: each futures contract represents £100,000 nominal value of a notional gilt with a 4% coupon, with a tick size of 0.01 points (£10.00 per contract). Trading volumes are substantial, with open interest across ICE’s total futures and options markets reaching a record 109.5 million contracts as of October 2025, up 16% year-on-year.

Why do futures matter for yields? Because futures prices are forward-looking. A gilt futures contract expiring in December embeds the market’s expectation of where gilt yields will be at that time – plus a term premium, plus a convenience yield, plus a funding spread. These expectations feed back into cash gilt prices via arbitrage: if the futures price implies a higher yield than the cash gilt, traders will sell futures and buy cash gilts (the basis trade), pushing cash prices up and yields down until the relationship is restored.

The basis trade is not a neutral arbitrage. It is a leveraged, cross-market speculation that can amplify shocks. In the US Treasury market, basis trades have been linked to several flash crashes. In the UK, the Bank of England has explicitly warned that “the disorderly unwind of highly leveraged, concentrated positions” in gilt repo and futures markets could destabilise the entire gilt market.

Futures markets are often described as “discovering” the “true” cost of borrowing. But what they are actually doing is aggregating speculative views on what the central bank will choose to do with interest rates. The “forward curve” is not a natural phenomenon; it is a collective guess about future policy decisions. When those guesses prove wrong, the state bears the cost of adjustment.

Gilt STRIPS

The Zero-Coupon Deconstruction

STRIPS – Separate Trading of Registered Interest and Principal of Securities – is the process of decomposing a conventional gilt into its constituent cash flows: each semi-annual coupon payment becomes a separate zero-coupon security, and the final principal repayment becomes another zero-coupon security. These zero-coupon instruments are then traded separately, creating a market for risk-free cash flows at specific maturities.

The UK government allows stripping and reconstitution through the DMO’s facility. HM Revenue & Customs notes that “Strips are deeply discounted securities” and that “bond stripping could result in tax deferral”. Stripped gilts are popular with pension funds seeking to match specific liability cash flows. More recent data from 2024 estimates that UK pension funds and insurance companies hold

$602 billion worth of gilts, equating to 22.3 per cent of the entire market.

The significance of STRIPS for the separation of yields from HMT operations is subtle but profound. When a gilt is stripped, its cash flows are no longer bundled together. The yield on a coupon strip maturing in six years is not the same as the yield on a conventional gilt with six years to maturity, because the strip has no reinvestment risk. The zero-coupon yield curve derived from STRIPS is different from the par yield curve derived from conventional gilts. Which one is the “true” risk-free rate? The answer depends on whom you ask – but HM Treasury does not get a vote.

STRIPS fragment the yield curve into multiple, sometimes conflicting signals. This fragmentation is presented as “price discovery”, but it is more accurately described as “price multiplication” – creating multiple yields from the same underlying government promise. The state issues a single gilt; the market creates dozens of derivative yields, none of which the Treasury controls. This is not market efficiency; it is market complexity layered upon policy choice.

Gilt Swaps

Transforming Fixed into Floating

An interest rate swap is a contract in which two parties exchange cash flows: one party pays a fixed rate and receives a floating rate (SONIA, the Sterling Overnight Index Average), while the other does the opposite. In the gilt market, swaps are used to convert fixed-rate gilt exposures into floating-rate exposures, and vice versa.

SONIA is the Bank of England’s chosen risk-free rate, calculated as the volume-weighted average of overnight unsecured sterling transactions. Three-month SONIA futures are cash settled based on the compounded average of daily SONIA rates, enabling market participants to hedge or speculate on short-term interest rates.

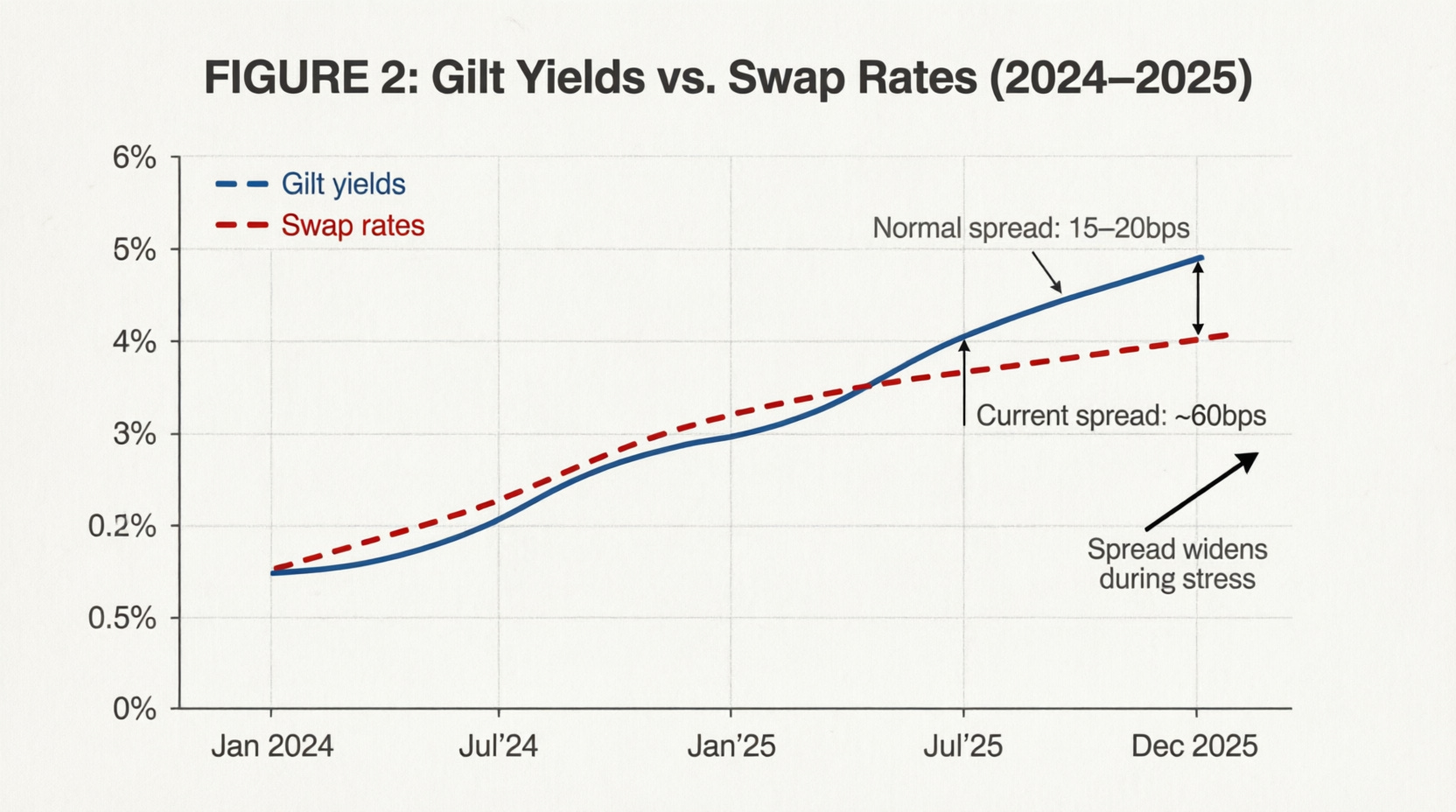

The gap between gilt yields and swap rates – the gilt swap spread – is a crucial market signal. Over the last few years, the spread between UK gilts and swap rates has significantly increased and remains elevated, with gilts currently offering investors a significant yield pickup over swaps. By August 2025, the 10-year gilt swap spread was reported at around 60 basis points, compared to a normal range of 15–20 basis points.

What does this spread tell us? A widening gilt swap spread typically indicates stress in funding markets. When investors fear that collateral will become scarce, they are willing to accept lower yields on swaps (which do not require collateral posting in the same way) relative to gilts. The Bank of England has noted that liquidity problems have appeared in lesser-followed places like Treasury basis trades and interest rate swap spreads, acting as canaries in the coal mine for broader market dysfunction.

The swap market, like the futures market, is a forward-looking, derivative-driven price discovery mechanism. When a corporate treasurer wants to know the cost of issuing a floating-rate bond, they look at the swap curve, not at the gilt curve. The swap curve is not set by HM Treasury; it is set by the collective judgement of swap traders.

The swap market has effectively displaced the gilt curve as the benchmark for private borrowing. This means that the cost of capital for households and businesses is determined by a derivatives market that HM Treasury does not control. Yet when that market malfunctions, the state is called upon to stabilise it. This is privatised price-setting with socialised risk – a structural feature of the current architecture, not a bug.

How Derivatives Disconnect Yields from HMT Operations

The Primary-Secondary Chasm Revisited

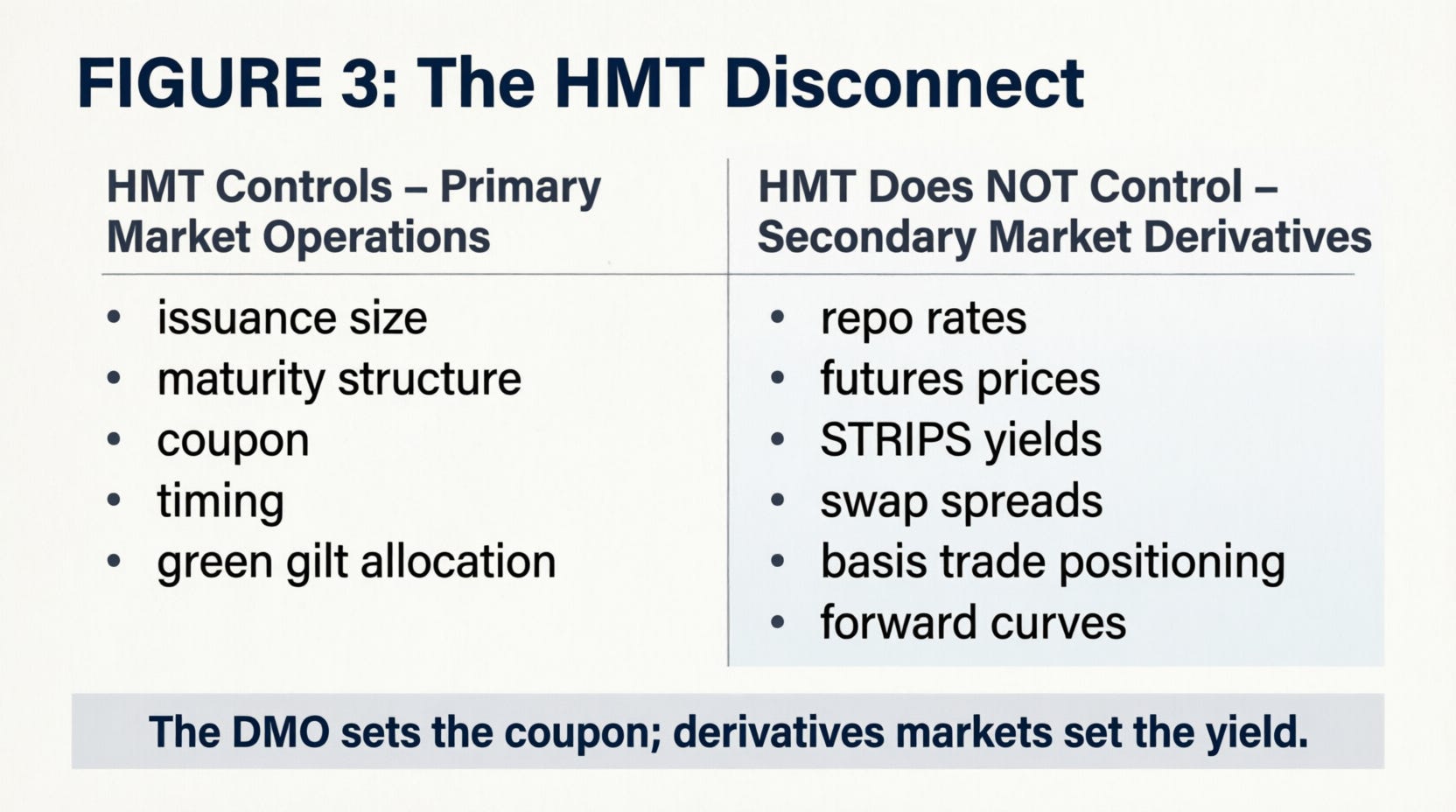

The DMO’s primary market sets the coupon and the initial price at auction. From the moment the gilt begins trading in the secondary market, however, its price and yield are determined by supply and demand among private participants. Derivatives amplify this separation by creating additional layers of price discovery.

A hedge fund that shorts a gilt futures contract is not buying or selling a gilt. It is expressing a view on future gilt yields without ever taking delivery of the physical bond. Its trading activity affects the futures price, which through arbitrage affects the cash gilt price. The DMO has no presence in this transaction. The hedge fund does not need to consult the DMO about its plans. Yet the yield that emerges from the interaction of thousands of such trades becomes the benchmark for government borrowing.

This is the constitutional reality of modern sovereign debt markets: unaccountable private actors determine the cost of public debt. The “bond vigilante” thesis celebrates this as market discipline; MMT recognises it as a political choice to delegate pricing power to speculative actors who bear no public accountability. The operational capacity of the state to spend is unchanged; the political cost is what varies.

The Basis Trade and the Leverage Amplifier

The basis trade – simultaneously buying cash gilts and selling gilt futures to capture a small price discrepancy – is a telling example of derivative-driven yield determination. The trade is financed via repo markets, where hedge funds borrow cash against the gilts they have purchased. The Bank of England’s 2025 Financial Stability Report noted that leveraged borrowing by hedge funds in gilt repo markets remains elevated, reaching close to £100 billion in November 2025, and that this activity is related, at least in part, to the popularity of the cash-futures basis trade.

Why does this matter for HMT? Because the basis trade directly links cash gilt yields to futures prices and repo rates. When the trade is unwound – as it would be if margins were called or funding dried up – the relationship can break violently, causing cash yields to spike. The Bank of England has warned that “the disorderly unwind of highly leveraged, concentrated positions” could trigger a wave of forced selling, driving yields higher still. HM Treasury has no tool to prevent this, beyond the indirect influence of fiscal credibility.

The basis trade is a speculative arbitrage that exists only because the state chooses to maintain a spread between cash and futures prices. When the trade fails, the state must intervene to prevent systemic collapse. This is not a market failure; it is a policy-created fragility that socialises losses while privatising gains. The MMT question is not “how do we regulate this better?” but “why do we permit it at all?”

STRIPS and the Fragmentation of the Yield Curve

When a gilt is stripped, the resulting zero-coupon securities have their own yields, which are not identical to the yield on the original coupon gilt. The zero-coupon yield curve derived from STRIPS is used by pension funds to value their liabilities and by insurers to price annuities. It is also used by derivatives traders as an input into swap pricing models.

The DMO facilitates stripping but does not control it. The decision to strip a gilt, and the timing of that decision, is made by market participants based on their own tax, regulatory, and trading considerations. The resulting fragmentation of the yield curve – multiple yields for the same underlying cash flows – is a feature of the market, not a bug. But it means that there is no single “gilt yield” that HMT can point to as the cost of government borrowing. There are many yields, each with its own dynamics.

This fragmentation serves the interests of financial intermediaries who profit from complexity, but it obscures the operational reality: the government issues a single promise to pay, and the derivatives market creates multiple, sometimes contradictory, prices for that promise. The “price discovery” narrative masks the fact that these are not discovering fundamental values but rather gaming a policy-created structure.

Swaps and the Benchmark Displacement

Perhaps the most significant displacement is the use of swap rates, rather than gilt yields, as the benchmark for private borrowing. When a company issues a bond, it typically prices it as a spread to the swap curve, not to the gilt curve. When a lender offers a fixed-rate mortgage, they hedge using swaps, not gilts. The swap curve has, to a substantial extent, displaced the gilt curve as the risk-free benchmark for the real economy.

The Bank of England has noted that the swap market is “very volatile” and that gilt spreads move “much slower than dollars and euros and other currencies versus the swap market”. The

consequence is that the cost of borrowing for households and businesses is determined more by swap markets than by gilt yields – and swap markets are not controlled by HM Treasury.

The displacement of the gilt curve by the swap curve means that the cost of capital for the real economy is set in a derivatives market that HM Treasury does not control. Yet when that market malfunctions, the state is expected to stabilise it. This is the privatisation of price-setting and the socialisation of risk – a structural feature that MMT would challenge at its root.

The MMT Critique

The Schumpeter-Bezemer Distinction

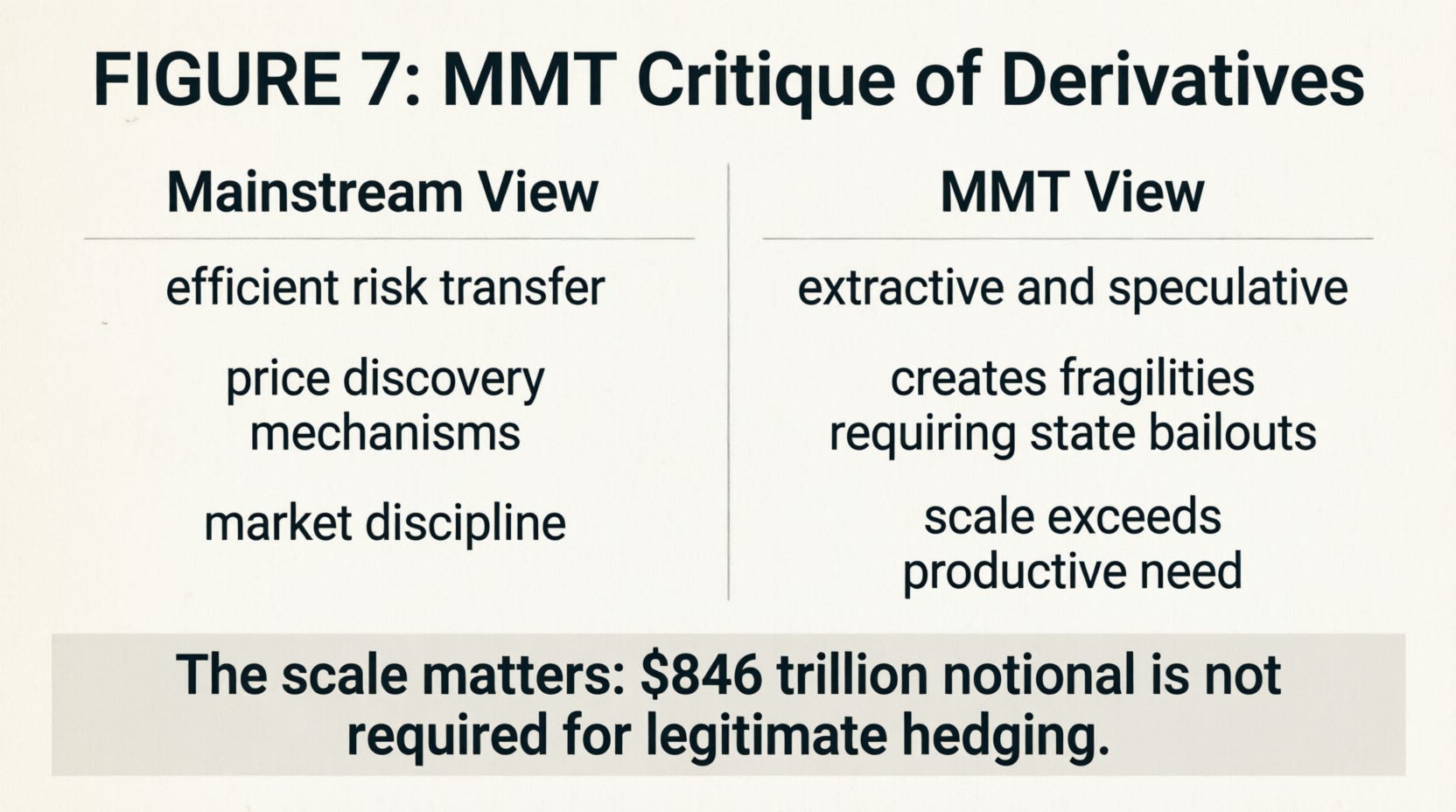

The productive versus extractive framing introduced in Article 1 applies with even greater force to derivatives. Following the work of Joseph Schumpeter and Dirk Bezemer, MMT economists separate finance into two parts: credit to productive sectors (manufacturing, infrastructure, agriculture, research and development) and credit for speculation (purchasing financial assets and real estate).

Derivatives trading in gilts falls squarely into the speculative category. When a hedge fund executes a basis trade, it does not finance a new factory. It does not employ a worker. It does not expand the economy’s productive capacity. It seeks to capture a small price discrepancy, amplified by leverage. If the trade is profitable, value is transferred from the counterparty to the fund. If it is unprofitable, the reverse occurs. In either case, no new real output is created.

This is not a moral judgement but an operational observation. Derivatives activity, at its current scale, diverts talent, capital, and computational resources away from productive investment. The question is not whether derivatives should exist – hedging and risk management are legitimate functions – but whether they should be permitted to grow to $846 trillion in notional value when a fraction of that scale would suffice for legitimate hedging.

The Extractive Case Against Derivatives

The extractive critique of derivatives is not that they serve no purpose – hedging and price discovery are real functions – but that the volume of speculative activity has grown far beyond what is necessary for these functions. The BIS reports that global OTC derivatives notional outstanding reached $846 trillion by June 2025. This is an astronomical figure, many times larger than global GDP. Even accounting for the fact that notional value overstates actual exposure, the scale is indicative of a financial system that has become decoupled from the real economy.

MMT would argue that this decoupling is not accidental. It is the result of deliberate policy choices: the deregulation of financial markets, the prioritisation of low inflation over full employment, and the acceptance of financialisation as an inevitable feature of modern capitalism. The derivatives market, on this view, is not a neutral mechanism for risk transfer. It is a rent-extracting machine that transfers wealth from productive workers and taxpayers to financial intermediaries and speculative investors.

The $846 trillion figure is not a measure of economic value; it is a measure of speculative churn. Reducing that churn would not harm the real economy; it would free up resources for more productive uses. The legitimate functions of derivatives – hedging, price discovery, liquidity provision – could be performed at a fraction of the current scale. The question is political: do we have the will to shrink a sector that has captured so much of our economy’s talent and resources?

The Counter-Argument

Hedging and Price Discovery

The counter-argument is that derivatives serve essential economic functions. A pension fund that uses swaps to hedge its interest rate exposure is not speculating; it is managing risk so that it can meet its obligations to retirees. A corporate treasurer who uses SONIA futures to lock in borrowing costs is not gambling; she is ensuring that the company can invest with confidence.

Moreover, derivatives contribute to price discovery. The futures market aggregates information about future interest rates, inflation, and economic conditions. This information is valuable for real investment decisions. A factory is more likely to be built if futures markets signal stable long-term interest rates.

MMT acknowledges these functions but argues that they do not require the current scale of derivative activity. A small, well-regulated derivatives market could provide hedging and price discovery without the extractive excess. The question is not whether derivatives should exist, but whether they should be permitted to grow to $846 trillion in notional value.

The hedging argument is often used to justify speculative excess. But there is a clear distinction between a pension fund hedging its liabilities and a hedge fund running a leveraged basis trade. The former serves a social purpose; the latter extracts rent. The regulatory framework should distinguish between them, not treat them as equivalent “market participants”.

The 2022 LDI Crisis as Derivative Failure

Anatomy of a Derivative-Driven Crisis

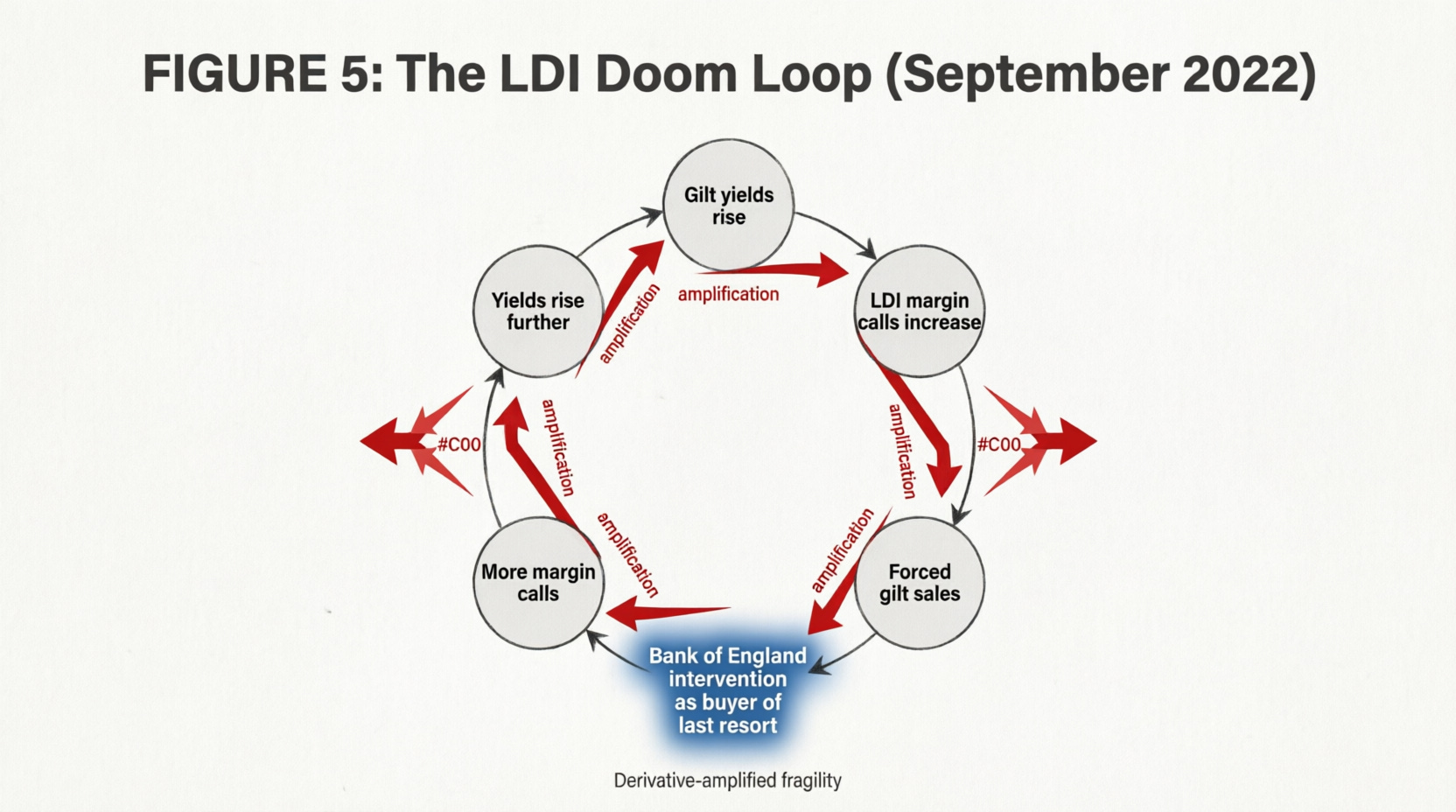

The Liability-Driven Investment (LDI) crisis of September 2022 is the most vivid recent illustration of derivative-amplified fragility. LDI funds used interest rate swaps and gilt repos to hedge pension scheme liabilities. When gilt yields spiked following the “mini-budget”, the margin calls on these derivative positions became unsustainable. Forced selling of gilts to meet margin calls drove yields higher, triggering further margin calls. The total net sales of gilts between 23 September and 14 October exceeded £36 billion.

The Bank of England was forced to intervene as a buyer of last resort, announcing a temporary purchase programme for long-dated gilts. The intervention stabilised the market but revealed the extent to which derivative-driven dynamics had overtaken underlying fundamentals.

The LDI crisis demonstrated that the state is always the ultimate backstop. The derivative market claimed to be “managing risk”, but when that risk materialised, it was the central bank that had to step in. This is not a market failure; it is the logical endpoint of a system that privatises gains and socialises losses.

What the LDI Crisis Reveals About Derivative Markets

Three lessons from the LDI crisis are relevant to our analysis.

First, derivatives can create “doom loops” that amplify rather than absorb shocks. The LDI funds’ use of swaps and repos was prudent on a standalone basis but became catastrophic when many funds attempted to unwind simultaneously. The derivative market did not have the capacity to intermediate these flows without price dislocation.

Second, derivative positions can be opaque. The Bank of England did not have real-time visibility into the aggregate leveraged positions of LDI funds until the crisis was underway. This opacity is a feature of over-the-counter derivative markets, which lack the transparency of exchange-traded instruments.

Third, when derivative markets fail, the state must step in. The Bank of England’s intervention was not a bailout of speculators; it was a necessary response to a systemic threat. The derivative market did not self-correct. It required a central bank buyer of last resort.

The LDI crisis proved that the “self-regulating market” is a fiction. When stress arrives, the state intervenes – not because it chooses to, but because it must. This being the case, MMT argues that the state should have the authority to prevent such crises by limiting speculative excess, not merely to respond to them after the fact.

Policy Implications

Can Derivatives Be Tamed?

The Bank of England’s Proposals

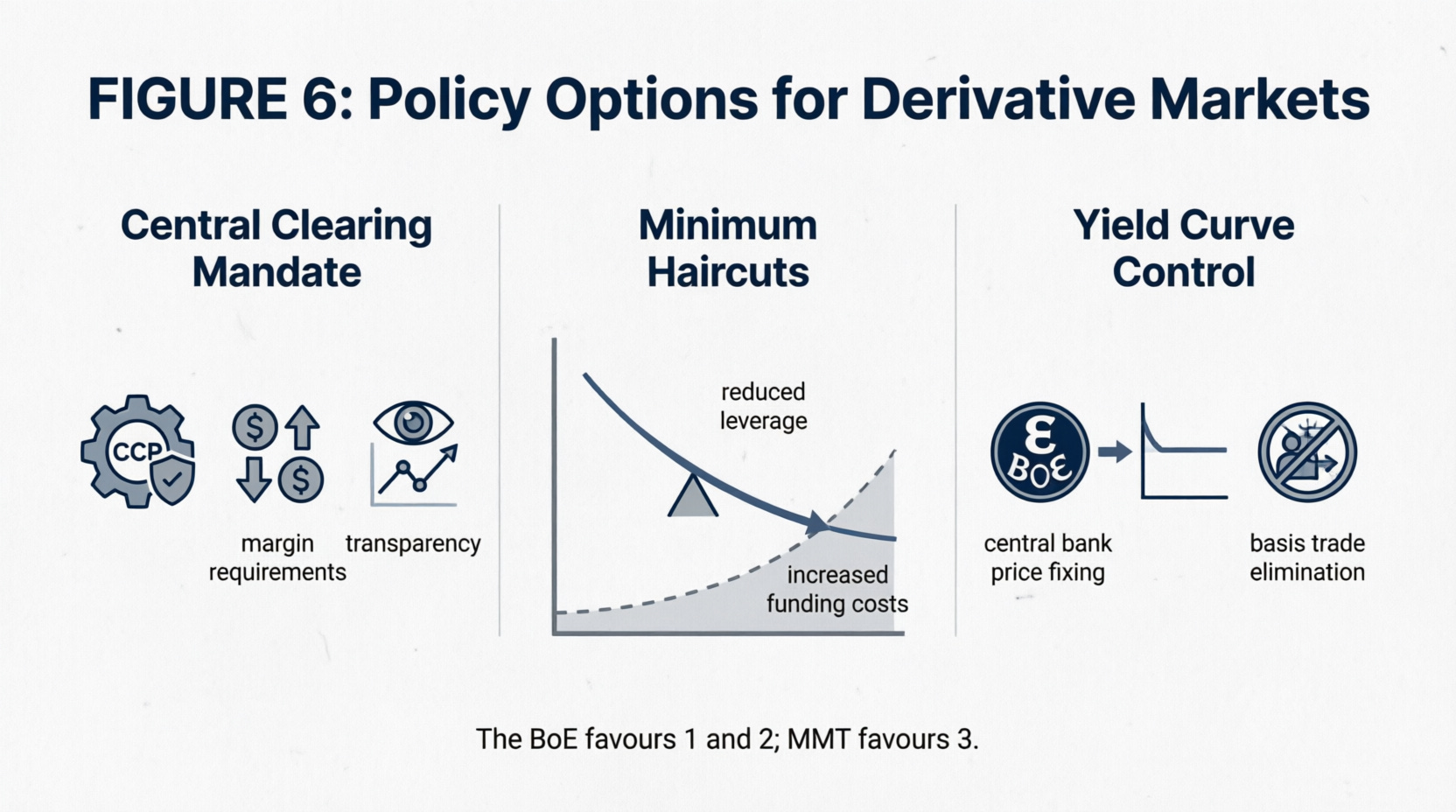

The Bank of England’s 2025 discussion paper on enhancing gilt repo market resilience explored two primary options: greater central clearing of gilt repo transactions and minimum haircuts or margins on non-centrally cleared gilt repo. Both measures would affect derivatives activity by increasing collateral requirements and reducing the opacity of leveraged positions.

The industry response has been mixed. ICMA strongly opposed mandatory clearing, arguing that “this would increase costs and restrict access for some participants” and that “clearing should be a commercial choice”. The BoE’s April 2026 Feedback Statement acknowledged this resistance while affirming that “further action is needed to deliver structural improvements to the resilience of the gilt repo market”.

Mandatory Central Clearing

Central clearing would require many derivative transactions (including repos, futures, and swaps) to be routed through a CCP such as LCH Ltd. The CCP would impose margin requirements, mutualise default losses, and provide real-time visibility into aggregate positions.

LCH has already made progress in this direction. LCH RepoClear achieved a record high settlement efficiency rate of 99.49% for gilt settlements in August 2025, and saw Term£GC volumes increase by 15% in Q3 vs Q2 2025. In April 2026, LCH launched a sponsored clearing model for the buy side, with Insight Investment becoming the first asset manager to clear a trade acting for a UK pension fund.

This sponsored model brings the benefits of clearing – netting, margin efficiency, counterparty risk reduction – to a wider range of participants.

The limitation of central clearing is that it does not address the underlying issue: derivatives activity is speculative and extractive. It merely makes that activity safer and more transparent. MMT would argue that safety and transparency are insufficient; the goal should be to reduce the scale of speculative finance.

Central clearing is a technical fix to a political problem. It makes the derivatives market safer, but it does not question whether the market should be this large in the first place.

MMT would push further: if the state is the ultimate backstop, the state should have the authority to limit the scale of activities that create systemic risk.

Minimum Haircuts

The second option – minimum haircuts on non-centrally cleared repos – would increase the cost of leverage, potentially reducing the volume of basis trades and other speculative strategies. The industry has opposed this measure on the grounds that it would impair liquidity and increase funding costs for legitimate hedgers.

The Bank of England’s July 2025 Financial Stability Report noted that the FPC will keep the case for introducing a minimum haircut under review, recognising that UK repo and securities lending markets continue to be less reliant on non-centrally cleared transactions than in some other jurisdictions.

The MMT Alternative: Monetary Financing

MMT offers a more radical alternative: eliminate the need for derivatives by eliminating the thing they speculate on. If the central bank were to adopt explicit yield curve control – committing to purchase unlimited quantities of gilts at a target yield – the derivative market would lose its primary anchor. Basis trades would become impossible because the cash price would be fixed by central bank intervention. Swap spreads would become irrelevant because the central bank would set both gilt yields and the policy rate.

This proposal is politically explosive. Yield curve control has been tried in other jurisdictions (Japan, Australia, briefly the UK in 2022) with mixed results. Critics argue that it would lead to fiscal dominance, where monetary policy is subordinated to the government’s borrowing needs. MMT responds that this is already the case – the Bank of England was forced to intervene as a buyer of last resort in 2022, demonstrating that the central bank is ultimately responsible for gilt market stability regardless of the formal separation of fiscal and monetary policy.

The choice is not between “free markets” and “state control”. It is between explicit state control (yield curve control, position limits, activity restrictions) and implicit state control (bailouts when things go wrong). MMT prefers the former: if the state is ultimately responsible, it should have explicit authority to shape the market’s structure, not merely to clean up the mess.

The MMT Perspective

Derivatives as a Policy Choice

The Central Bank’s Ultimate Power

MMT’s core insight is that a currency-issuing sovereign government can never be forced into insolvency in its own currency. This applies with equal force to derivatives: the Bank of England can always provide unlimited sterling liquidity to stabilise the gilt market. The 2022 LDI intervention demonstrated this capacity.

From an MMT perspective, the derivative market exists because the central bank chooses not to control yields directly. The volatility, the basis trades, the swap spreads, and the speculative churn are not unavoidable features of a market economy. They are the consequences of a policy choice to delegate yield determination to private actors.

The “market determines yields” narrative obscures the operational reality. The central bank sets the policy rate; it can set the entire yield curve if it chooses. The derivatives market speculates on the gap between what the central bank does and what it could do. That gap is a policy choice, not a market necessity.

Derivatives as an Extractive Sector

MMT would argue that the derivatives market, at its current scale, is extractive. It diverts talent and capital away from productive activity, creates systemic fragilities that require taxpayer-funded bailouts, and transfers wealth from the real economy to the financial sector.

The $846 trillion in notional OTC derivatives outstanding is not a measure of economic value. It is a measure of speculative churn. Reducing that churn would not harm the real economy; it would free up resources for more productive uses. The legitimate functions of derivatives – hedging, price discovery, liquidity provision – could be performed at a fraction of the current scale.

The extractive nature of derivatives is not a moral failing; it is a structural feature. When finance grows beyond the optimal threshold identified by the IMF (the “Poland level”), it becomes a drag on growth. The UK is far beyond that threshold. The question is not whether to regulate derivatives, but whether to shrink them.

The Inevitability of State Intervention

The LDI crisis demonstrated that when derivative markets fail, the state must intervene. This is not a bug; it is a feature of the system. The derivative market’s claim to be an independent, self-regulating mechanism is exposed as fiction when stress arrives.

MMT concludes that if the state is ultimately responsible for stability, the state should also have the authority to shape the market’s structure. That authority could be used to reduce the scale of speculative activity, redirect credit to productive sectors, and insulate the real economy from financial volatility.

The state is always the backstop. The choice is between preventive regulation (limiting scale, restricting activities, imposing position limits) and reactive intervention (bailouts after the fact). MMT prefers prevention: if the state bears the risk, it should have the authority to limit it.

Conclusion

The Derivatives Bazaar and the Treasury’s Empty Seat

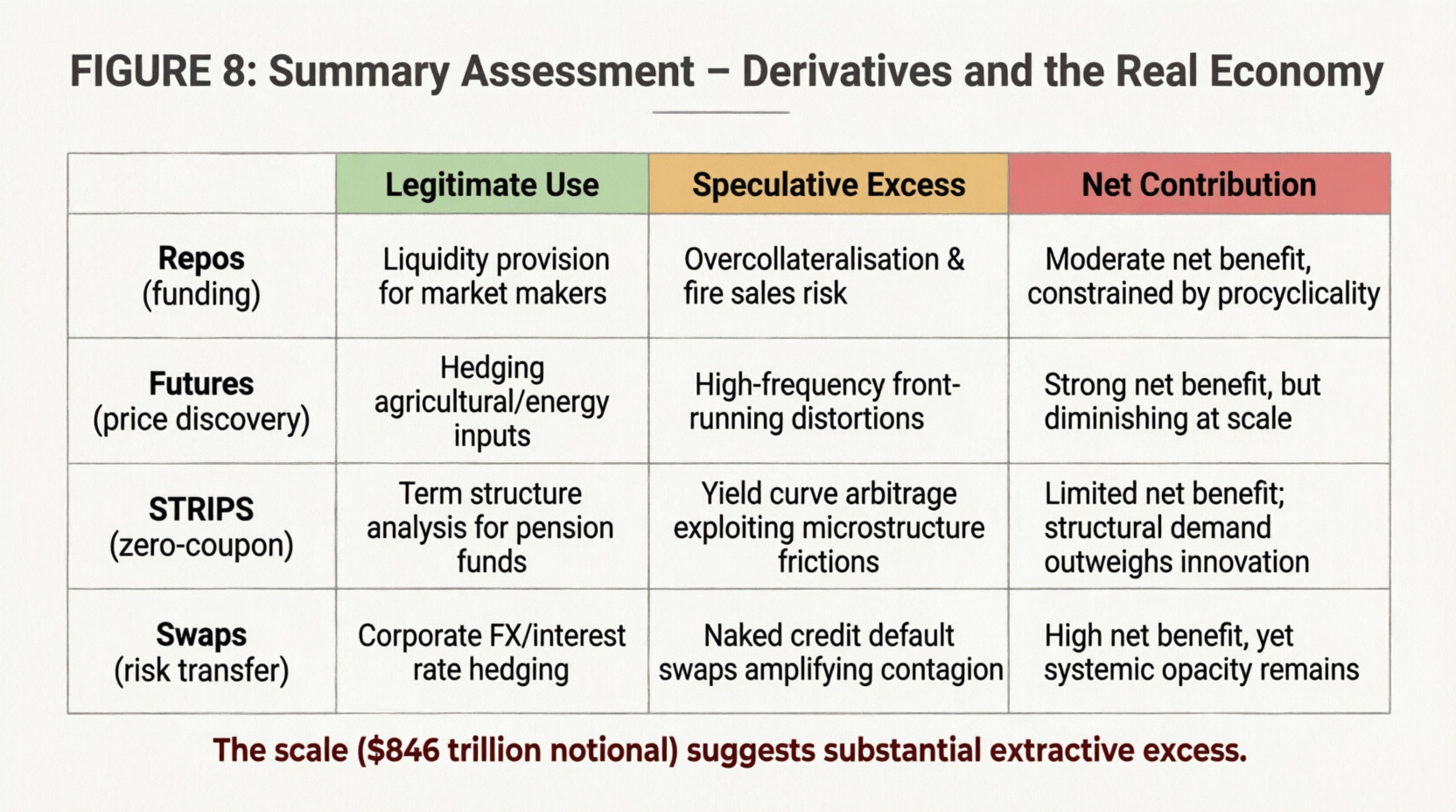

The secondary market in gilt derivatives is not a sideshow. It is the main event. Repos, futures, STRIPS, and swaps are the instruments through which yields are discovered, risks are transferred, and speculation is amplified. HM Treasury is not a participant in this market. It does not set repo rates, determine futures prices, influence swap spreads, or control the stripping of its own bonds. It issues the raw material; derivatives markets process it.

This arrangement has defenders and critics. Defenders argue that derivative markets provide essential liquidity, enable efficient risk transfer, and produce valuable price signals. Critics argue that the scale of derivative activity is extractive, that it creates systemic fragilities, and that the legitimate functions of derivatives could be performed at a much smaller scale.

The empirical evidence supports both positions, depending on the threshold. The IMF’s finding that financial deepening beyond a certain point becomes a drag on growth applies to derivatives with particular force. The $846 trillion notional figure is not a measure of economic value. It is a measure of churn.

The LDI crisis of 2022 demonstrated that derivatives can amplify rather than absorb shocks. When the market failed, the state intervened. The derivative market did not self-correct. This is not an argument for abolishing derivatives, but it is an argument for regulation that limits speculative

excess, mandates transparency, and ensures that the state’s ultimate backstop is matched by the state’s ultimate authority.

The fundamental constitutional reality remains: HM Treasury does not control the derivatives market. The yields that emerge from this market determine the cost of government borrowing, the pricing of corporate debt, and the cost of mortgages. Yet no minister is present when a basis trade is executed, a strip is created, or a swap spread is priced. The derivatives bazaar governs yields; the question for democracy is whether this governance should be subject to any democratic control.

The derivatives market is a policy choice, not an economic necessity. We can choose to shrink it, regulate it, or even eliminate it through yield curve control. The constraint is not “market discipline”; it is inflation and real resource availability. The question is political: do we have the will to subordinate finance to the public purpose, or will we continue to permit an extractive sector to govern the cost of public debt?

In the next article of this series, we examine rehypothecation – the legal, ethical, and operational practice of reusing collateral in the gilt repo market – and its implications for the separation of yields from HMT operations. The chains of rehypothecation, we shall see, are where the same gilt can be pledged many times over, creating hidden leverage and further distancing yields from anything HM Treasury can influence.

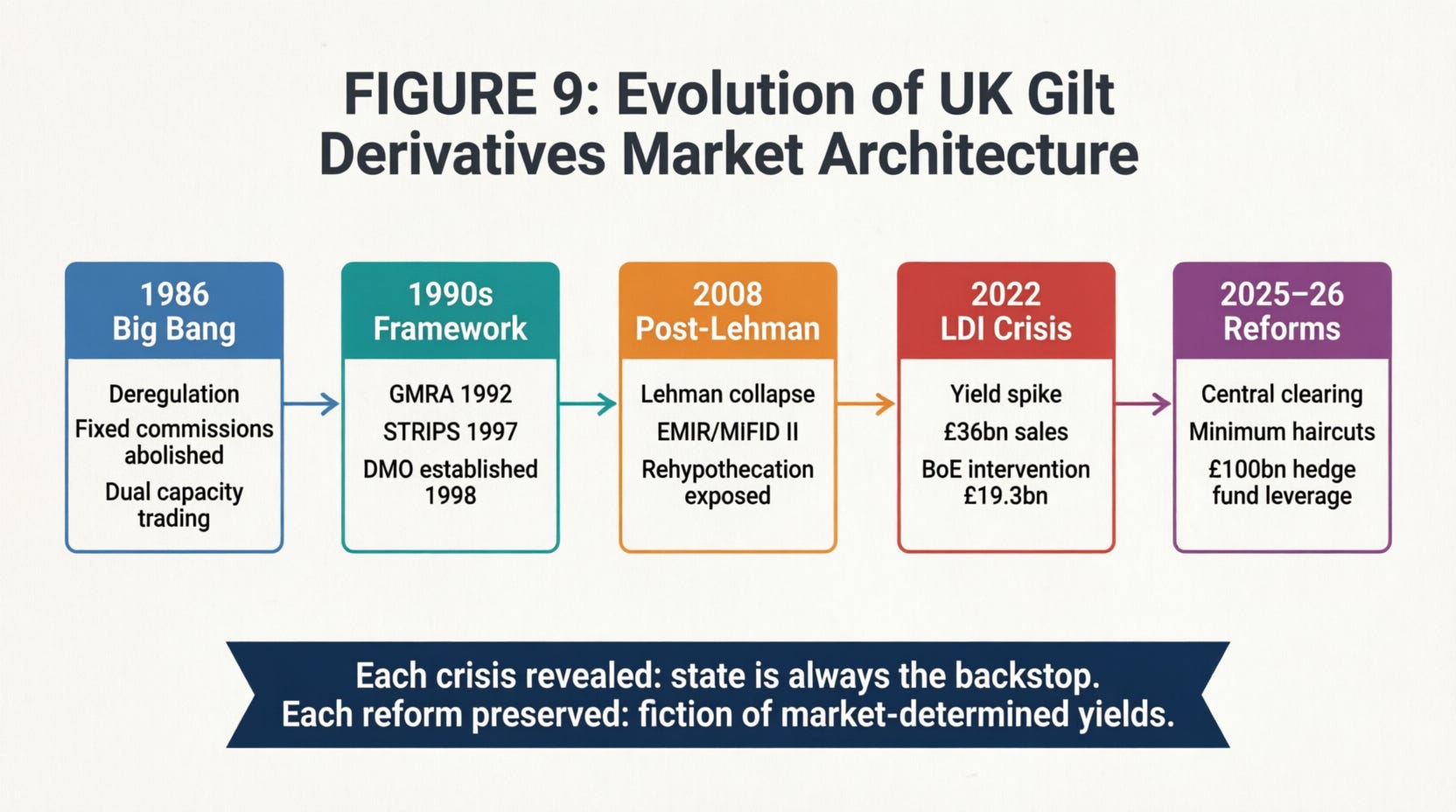

Evolution of Gilt Derivatives

A History Forged in Crisis

The gilt derivatives market did not emerge by accident. Its evolution has been a story of crisis, legal innovation, and the slow, often reluctant recalibration of state power. Each major legal and political shock — the deregulatory “Big Bang” of the 1980s, the institutionalisation of repo and stripping in the 1990s, the catastrophic legal battles following Lehman’s collapse in 2008, the European regulatory barrage of MiFID II and EMIR, and the near-collapse of the UK gilt market in 2022 — has fundamentally reshaped how the government’s debt is traded.

This is not a story of “market evolution” but of state-constructed markets. Each crisis revealed the same operational truth: the state is always the backstop. Yet each reform preserved the fiction that private actors, not public policy, determine the cost of public debt.

The Genesis: 1986 Big Bang

The modern foundation was laid on 27 October 1986, a date known as the “Big Bang”. This sweeping deregulation of the London Stock Exchange, driven by the Thatcher government, eliminated fixed commissions and abolished the historic division between brokers and jobbers. Crucially, it opened the gilt-edged securities market and authorised a dual-capacity system whereby a single firm could represent investors (brokering) and execute wholesale trades (dealing) on both equities and government debt. The changes proved successful: the volume of shares traded and market capitalisation increased, reinforcing London’s leadership in interbank lending, bond markets, and facilitating 24-hour trading across the world.

The Big Bang was a political choice to prioritise financial sector growth over other economic objectives. It was sold as “modernisation”, but it was really the beginning of UK financialisation — the deliberate expansion of finance as a share of GDP. The derivatives ecosystem we see today is the logical endpoint of that choice.

The 1990s

Formalising the Framework

If the 1980s opened the door, the 1990s furnished the rulebook. In 1992, the International Capital Market Association (ICMA) published the first Global Master Repurchase Agreement (GMRA), the standard industry contract for transacting repos. The GMRA was subsequently updated in 1995 to incorporate lessons from the collapse of Barings, and further updated in 2000 to incorporate lessons from the Russian and Asian financial crises. In parallel, the Bank of England introduced a series of critical operational reforms:

March 1997: The Bank widened the range of counterparties and included gilt repo as a regular instrument in its open market operations.

December 1997: The upgrade of the Central Gilts Office was completed, enabling the start of gilt strips trading. The Gilt Strips (Consequential Amendments) Regulations 1997 came into force on 1 December 1997, legally defining a “strip” and modifying statutory provisions to facilitate this new type of government security.

April 1998: A new Debt Management Office (DMO) assumed responsibility for the Government’s debt management, separating debt issuance from monetary policy.

These reforms created the legal and operational infrastructure for the derivatives explosion. The GMRA standardised repo contracts across jurisdictions, making it easier to lever positions. STRIPS fragmented the yield curve, creating new arbitrage opportunities. The DMO’s “independence” created the illusion that debt management was technical, not political. All three were policy choices that expanded the scope for speculative activity.

The Post-2008 Recalibration

Lehman, MiFID II and EMIR

The 2008 global financial crisis exposed the hidden fault lines in the repo market, particularly around rehypothecation. The subsequent UK government response was a regulatory realignment that remains in force today.

The collapse of Lehman Brothers International (Europe) on 15 September 2008 triggered a fierce legal battle under the GMRA 2000 that would last until 2016. The case of Lehman Brothers International (Europe) v ExxonMobil Financial Services BV [2016] EWHC 2699 (Comm) became the leading English authority on close-out valuation mechanics under the GMRA 2000. The core dispute revolved around a repo where EMFS had lent US$250 million to LBIE, providing a diversified portfolio of equities and bonds as collateral. The court ruled on several key issues: the meaning of “close of business” (finding it context-dependent, and in this case, a default notice received at or shortly after 6:02 p.m. was valid), the validity of service by e-mail, and the exercise of contractual discretion regarding valuation.

The crisis also triggered a wave of EU-level reforms — EMIR (European Market Infrastructure Regulation) and MiFID II (Markets in Financial Instruments Directive II) — which mandated the reporting of derivative trades to trade repositories and imposed new transparency and risk-mitigation requirements on OTC derivatives. These came into force in 2018 alongside the FCA’s updated rulebook. Following Brexit, the UK has maintained equivalent regimes, though the Treasury and FCA have begun to diverge to reduce compliance burdens.

The Lehman case revealed the legal fiction at the heart of repo markets: when collateral is rehypothecated, who actually owns it? The answer, as Lehman’s creditors discovered, is “whoever gets to the courthouse first”. EMIR and MiFID II attempted to patch this opacity with reporting requirements, but they did not challenge the fundamental practice of rehypothecation. From an MMT perspective, this is regulatory tinkering: making the extractive machinery transparent without questioning whether it should exist at this scale.

The 2022 LDI Crisis

Derivatives Amplify Fragility

The most vivid recent illustration of derivative-amplified fragility occurred in September and October 2022, when the Bank of England was forced to intervene in the gilt market to restore market functioning. Leveraged liability-driven investment (LDI) arrangements, which used financial instruments to increase allocation in gilts and derivatives, faced intense collateral demands as interest rates changed sharply. Total net gilt sales between 23 September and 14 October exceeded

£36 billion; DB pension plans accounted for approximately £14 billion of those sales, and LDI funds accounted for £23 billion. The Bank’s temporary and targeted purchase programme — announced on 28 September 2022 — ultimately purchased £19.3 billion of long-dated gilts to restore orderly market conditions. A subsequent Bank of England analysis found that the majority of margin calls came from repo, and in the run-up to the stress, LDI and pension funds in one sample reported a total of £205 billion of net gilt repo borrowing — around 60 per cent of total net gilt repo borrowing by non-banks.

The LDI crisis was not a “market failure” but a policy-created crisis. The state encouraged pension funds to use LDI strategies through regulatory frameworks (Solvency II, pension fund accounting rules). The state supplied the gilts that became the collateral for those strategies.

The state’s own policy announcement (the mini-budget) triggered the yield spike. And when the strategies failed, the state had to intervene. This is the circularity of modern finance: the state creates the conditions for speculative excess, then rescues the system when that excess unravels.

Current Reforms

Resilience and Leverage

As of 2025–2026, the Bank of England is actively consulting on a new wave of reforms designed to strengthen the plumbing of the UK’s government bond market. Lee Foulger, BoE director for financial stability, has warned that “unchecked leverage and near-zero collateral practices could amplify stress in times of turmoil”. The BoE’s discussion paper explores two main policy options: greater use of central clearing for gilt-backed repo trades and minimum “haircuts” (the extra collateral borrowers must post) on non-cleared transactions. These reforms are driven by evidence that a small number of hedge funds account for more than 90 per cent of net gilt repo borrowing, with trades often transacted at zero or near-zero collateral haircuts and very short maturities requiring regular refinancing. Leveraged borrowing by hedge funds in gilt repo markets reached close to £100 billion in November 2025. The debate remains contested, with ICMA strongly opposing mandatory clearing on grounds that “this would increase costs and restrict access for some participants”.

These reforms are necessary but insufficient. Central clearing and minimum haircuts make the derivatives market safer, but they do not make it smaller or less extractive. The MMT question is: why do we need £100 billion of hedge fund leverage in gilt repo markets? What

productive purpose does this serve? The answer is: none. It is speculative churn, pure and simple. The BoE is trying to make the casino safer; MMT would ask why we have a casino at all.

Conclusion

The Market Forges the Contract

From the floor of the London Stock Exchange to the electronic messaging systems that now serve default notices after 6:00 p.m., gilt derivatives have evolved through a series of punctuated equilibria — long periods of stability interrupted by catastrophic shocks. Each shock has rewritten the legal and political architecture, but the underlying dynamic remains unchanged: HM Treasury issues the gilt, but the derivatives market, through its private contracts and centralised clearing houses, determines the yield.

This is not inevitable. It is the result of policy choices made over four decades: to deregulate, to financialise, to delegate yield determination to private actors, and to socialise losses when those actors fail. The operational reality is that the state could control yields directly through yield curve control. It could limit speculative activity through position limits or activity restrictions. It could shrink the derivatives market by reducing gilt issuance and maintaining larger reserve balances.

The question is not whether these options are technically feasible — they are. The question is whether they are politically feasible. That is a question of power, not economics. And it is a question that MMT insists must be asked.

References

Bank for International Settlements (2025a) OTC derivatives statistics at end-June 2025. Basel: Bank for International Settlements. Available at: https://www.bis.org/statistics/derstats.htm

Bank for International Settlements (2025b) Biggest hedge funds get best repo leverage terms, BIS finds. Basel: Bank for International Settlements. Available at: https://www.bis.org

Bank of England (2023) Financial stability buy/sell tools: a gilt market case study. November 2023. London: Bank of England. Available at: https://www.bankofengland.co.uk

Bank of England (2025a) Financial Stability Report, July 2025. London: Bank of England. Available at: https://www.bankofengland.co.uk/financial-stability-report

Bank of England (2025b) Enhancing the resilience of the gilt repo market: a discussion paper. September 2025. London: Bank of England. Available at: https://www.bankofengland.co.uk

Bank of England (2026) Enhancing the resilience of the gilt repo market – discussion paper feedback statement. 1 April 2026. London: Bank of England. Available at: https://www.bankofengland.co.uk

Bloomberg (2025) ‘FTSE 100 live: UK stocks jump most since 2020 as tariff pause sparks rally’, Bloomberg, 10 April. Available at: https://www.bloomberg.com

CME Group (2022) Excell with options: Do JPY and GBP have a similar set-up with different outcomes? 1 November 2022. Available at: https://www.cmegroup.com

Euromoney (2022) ‘The bond vigilantes are back with a vengeance’, Euromoney, 13 October. Available at: https://www.euromoney.com

Finadium (2026) ‘Net gilt repo positioning reached highest level in early 2026’. Available at: https://www.finadium.com

Foulger, L. (2025) ‘Strengthening market resilience: navigating evolving dynamics in sovereign markets’, Speech at AFME’s 20th Annual European Government Bond Conference, 12 November 2025. London: Bank of England. Available at: https://www.bankofengland.co.uk/speech

Hedgeweek (2025) ‘UK hedge fund repo leverage surges to record levels’. Available at: https://www.hedgeweek.com

Informist Media (2025) ‘Down on sales from PDs, FPIs unwind bond swap trades’. Available at: https://www.informistmedia.com

Intercontinental Exchange (2025a) 10 year Long Gilt futures contract specifications. Available at: https://www.ice.com

Intercontinental Exchange (2025b) Intercontinental Exchange reports October statistics. Available at: https://www.ice.com

International Capital Market Association (2025) ICMA ERCC position papers and responses to public consultations. London: ICMA. Available at: https://www.icmagroup.org

LCH Ltd (2025a) ‘RepoClear sets new gilt settlement efficiency record, sees Term£GC volume growth’. Available at: https://www.lseg.com/lch

LCH Ltd (2025b) LCH RepoClear Q3 2025 highlights. Available at: https://www.lseg.com/lch

LCH Ltd (2025c) LCH minimum cash framework: activation of the minimum cash requirement. Available at: https://www.lseg.com/lch

LCH Ltd (2026) ‘LCH RepoClear introduces new sponsored clearing model’, Traders Magazine, 15 April. Available at: https://www.tradersmagazine.com

Lehman Brothers International (Europe) v ExxonMobil Financial Services BV [2016] EWHC 2699 (Comm).

Organisation for Economic Co-operation and Development (2025) Institutional investors and long-term investment: UK country note. Paris: OECD Publishing.

Sahay, R., Čihák, M., N’Diaye, P., Barajas, A., Ayala Peña, D., Bi, R., Gao, Y., Kyobe, A., Nguyen, L., Saborowski, C., Svirydzenka, K. and Yousefi, S.R. (2015) Rethinking financial deepening: stability and growth in emerging markets. IMF Staff Discussion Note SDN/15/08. Washington, D.C.: International Monetary Fund. Available at: https://www.imf.org/external/pubs/ft/sdn/2015/sdn1508.pdf

Sky News (2022) ‘UK has lost credibility among investors and the “bond vigilantes” serve as a warning’, Sky News, 18 October. Available at: https://news.sky.com

Swiss Re (2025) Gilt swap spread analysis. Available at: https://www.swissre.com

Summary by Claude, what do you think -

"Core argument: The gilt yield that HM Treasury cares about is not actually set by the Treasury — it emerges from a vast derivatives market that the government has no direct control over, yet must always bail out when it fails. From an MMT perspective, this is a political choice, not an economic necessity.

**The four key instruments explained:**

- **Repos** — allow hedge funds to borrow against gilts to fund leveraged trades. Hedge fund net repo borrowing hit a record ~£100bn in late 2025, much of it financing the "basis trade" (arbitraging small price gaps between cash gilts and gilt futures).

- **Gilt futures** — standardised contracts whose prices feed back into cash gilt yields via arbitrage. Futures markets don't discover "true" yields; they aggregate guesses about what the Bank of England will *choose* to do with rates.

- **STRIPS** — gilts decomposed into individual cash flows traded separately, creating a fragmented zero-coupon yield curve that the Treasury doesn't control and that serves mainly pension funds and arbitrageurs.

- **Swaps** — interest rate swaps have largely *displaced* gilt yields as the benchmark for real-economy borrowing (mortgages, corporate bonds), yet HMT has no seat at that table either. The 10-year gilt-swap spread was around 60 basis points in mid-2025, well above the normal 15–20bp range.

**The 2022 LDI crisis as proof of concept:** When the mini-budget spiked gilt yields, pension funds using LDI strategies faced unsustainable margin calls, triggering forced gilt sales of over £36bn. The Bank of England had to step in and buy £19.3bn of long-dated gilts. The article argues this wasn't a market failure — it was the logical result of a *state-designed* system that privatises gains and socialises losses.

**The MMT critique:** The $846 trillion in global OTC derivatives is not a measure of economic value but of "speculative churn." Derivatives at this scale divert talent and capital from productive activity. The state is always the ultimate backstop — so it should have explicit authority to prevent crises rather than just clean them up. Options include mandatory clearing, minimum repo haircuts, or more radically, yield curve control (fixing the entire gilt curve directly).

**The bottom line:** Gilt yields — which determine UK government borrowing costs, mortgage rates, and corporate debt pricing — are set by an unaccountable, largely algorithmic derivatives bazaar. This is the result of four decades of deliberate deregulation and financialisation, not economic necessity. The constraint on change is political will, not operational capacity."