Rehypothecation

How the reuse of collateral creates hidden leverage, turns clients into unsecured creditors, and illustrates that HM Treasury has no seat in this shadow banking bazaar

A Tower of Risk

Legal, Ethical, and Operational Impacts

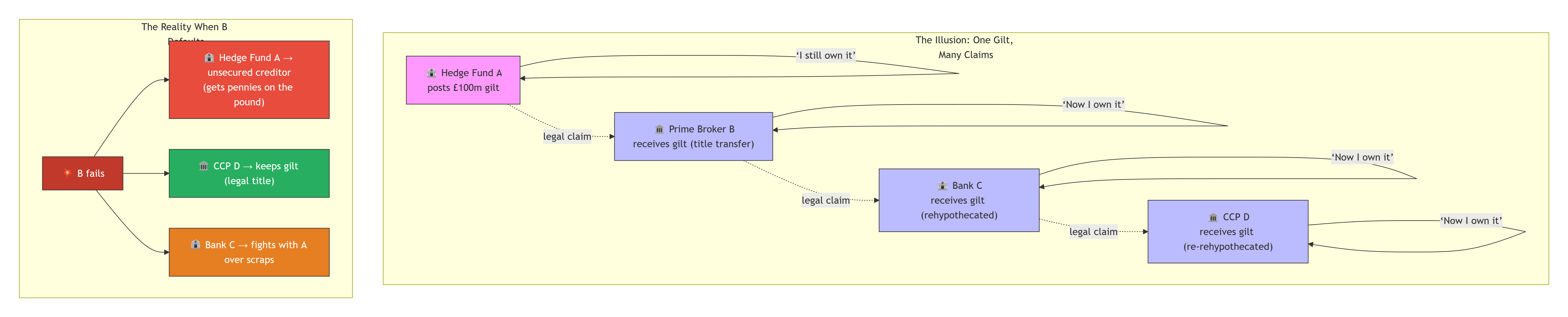

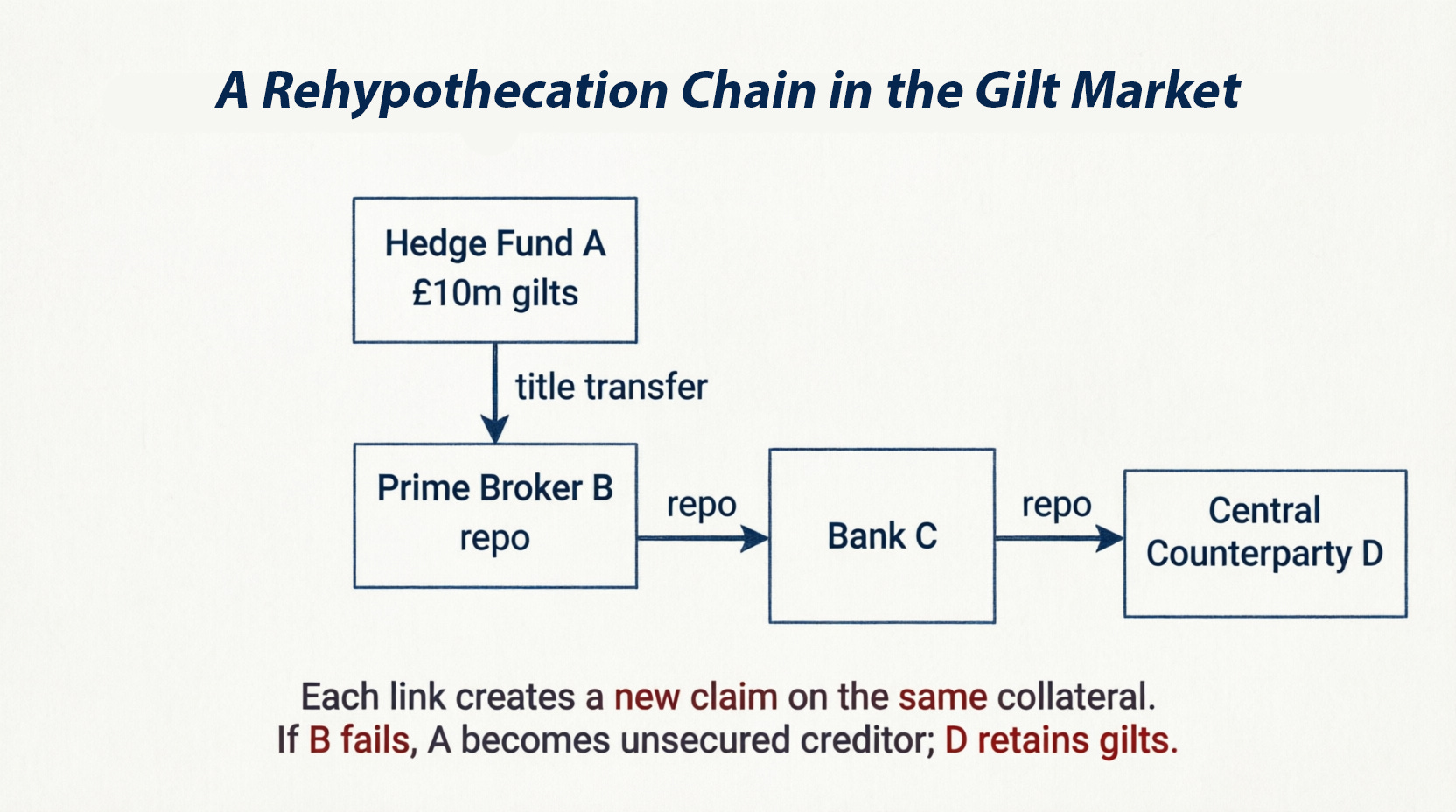

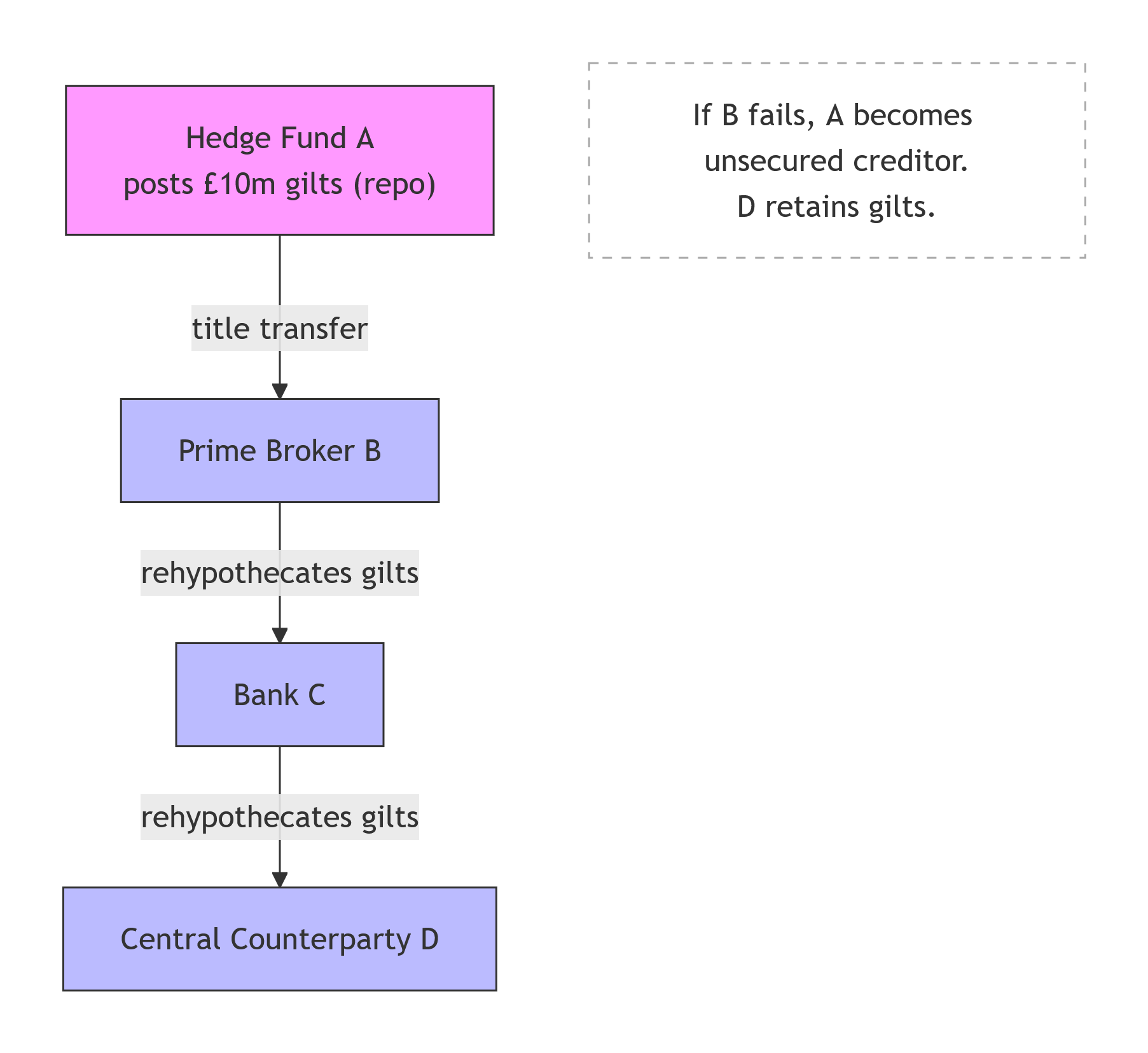

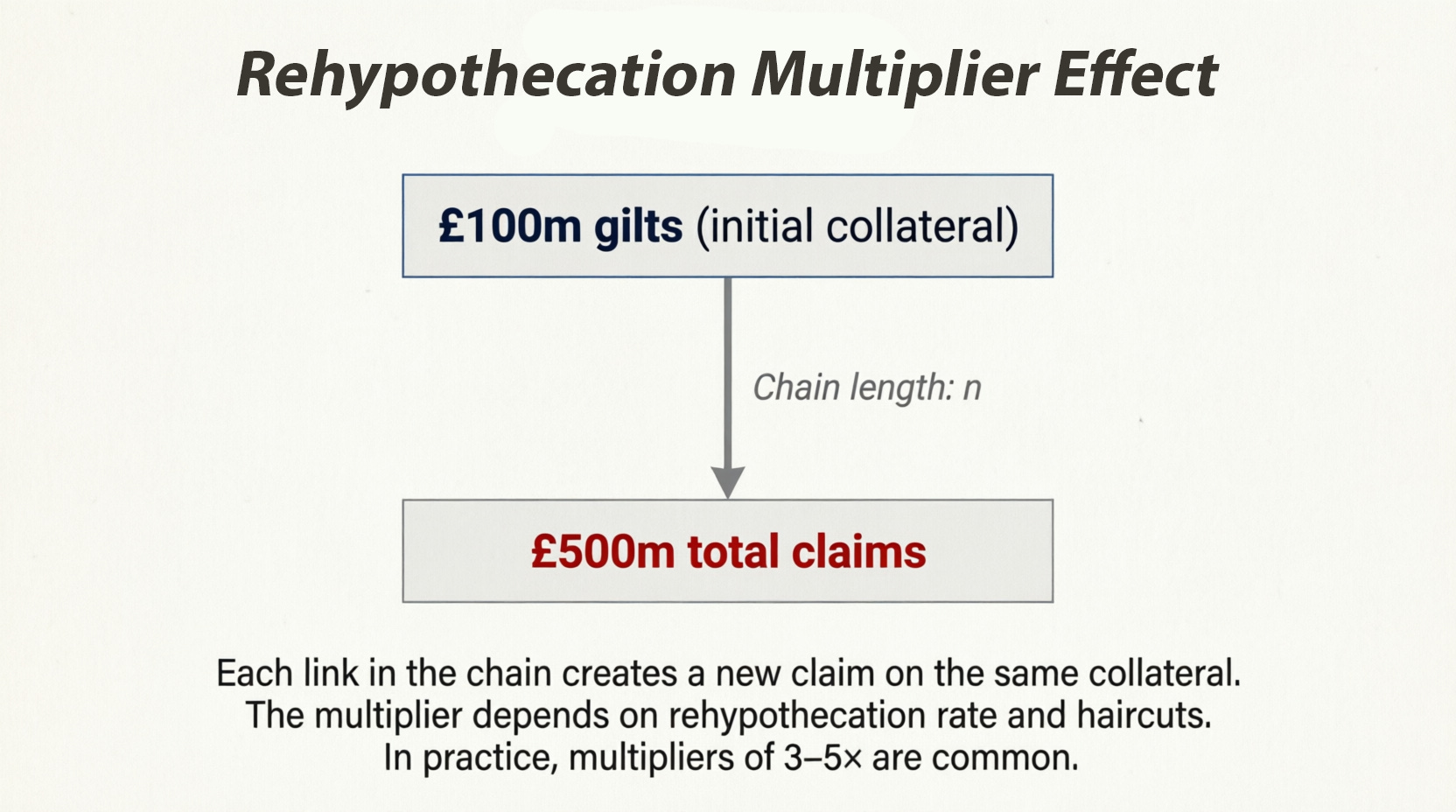

A gilt is pledged by a hedge fund to a prime broker as collateral. That prime broker, by virtue of legal title, pledges the same gilt to a clearing bank. The clearing bank, in turn, pledges it to a central counterparty. By the time the chain ends, the same £100 million of gilts may have been pledged multiple times, supporting several times that amount in leverage. The original hedge fund that posted the gilts believes it holds a claim on its assets. It does not. In the event of a default, it becomes an unsecured creditor, while a downstream bank may retain legal title to the gilts it never posted.

This is not a market failure but a policy-created structure. The state permits rehypothecation through legal frameworks (GMRA, CASS), then stands aside while private actors multiply claims on public debt. When the chains break, the state must intervene – not because it chose to, but because it is the ultimate backstop. The operational reality is that the state could restrict or abolish rehypothecation. It chooses not to.

This article examines the legal framework that enables rehypothecation, the ethical dimensions of client consent and systemic risk, the operational realities of collateral chains, the landmark Lehman case that exposed the catastrophic consequences of unlimited reuse, the 2022 LDI crisis as a rehypothecation-adjacent catastrophe, the policy debate over restrictions, and what Modern Monetary Theory makes of it all.

What Is Rehypothecation?

Definitional Foundation

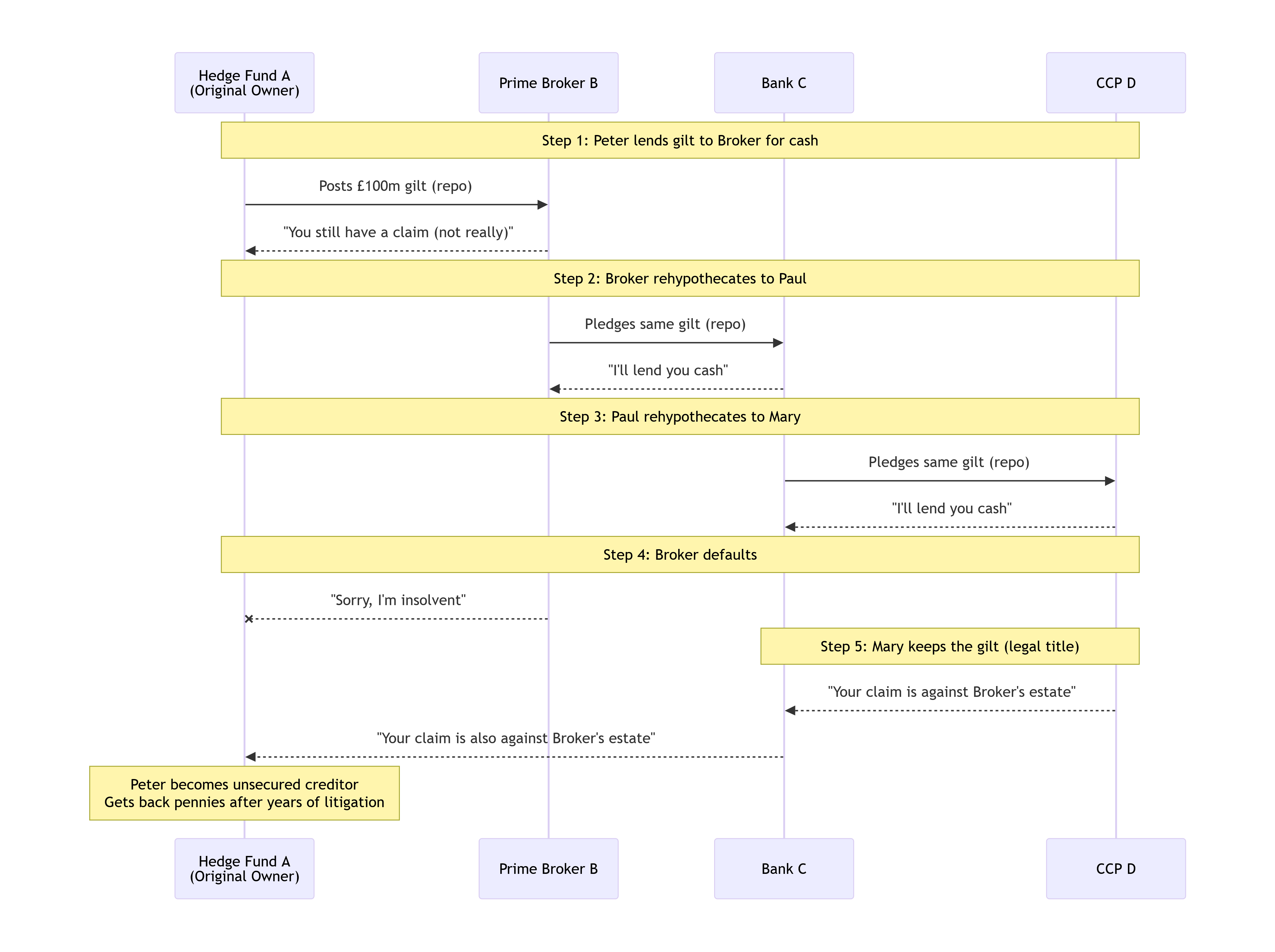

Rehypothecation is the practice by which a financial institution (typically a prime broker or bank) reuses collateral posted by its clients for its own purposes, such as securing its own borrowings or funding its trading activities. In the gilt market, it operates through the following mechanism:

A hedge fund borrows cash from a prime broker, posting gilts as collateral under a repurchase agreement (repo).

Under the GMRA, title to the gilts passes to the prime broker.

The prime broker, as legal owner, pledges the same gilts to another bank as collateral for its own borrowing.

The process repeats, creating a chain of rehypothecation.

The International Capital Market Association (ICMA) notes that rehypothecation is “an alternative name for re-pledging” and is “widely used by prime brokers involved in the collateralisation of derivatives transactions with hedge funds”. The practice “enables immense liquidity from a finite pool of assets, greasing the market’s wheels, but it also builds an invisible tower of interconnected risk where one failure can trigger a catastrophic collapse”.

The Title-Transfer Foundation

The legal foundation for rehypothecation in the UK is title transfer. In a repo governed by English law, the buyer of gilts does not merely take a security interest; it becomes the legal owner of the securities for the duration of the transaction. Rights of reuse are “inherent in title-transfer financial collateral arrangements—because ownership of the property actually changes”. This contrasts with pledge-based arrangements common in some civil law jurisdictions, where the collateral taker holds only a security interest and rehypothecation requires explicit consent.

The Oxford Law Faculty notes that “the same securities are assumed to be pledged and re-pledged again and again along a chain of transactions” and that “after reuse, the original collateral provider no longer has a property right in the reused securities and cannot assert claims against downstream transferees”. This is the crucial legal consequence: the original client becomes an unsecured creditor of its prime broker.

This legal architecture is not inevitable. It is a policy choice to prioritise title-transfer arrangements that facilitate collateral reuse over pledge-based arrangements that would protect original owners. The state could require explicit consent for each reuse, or prohibit reuse entirely. It chooses not to, because the financial sector demands the liquidity benefits. This is distributional politics, not economic necessity.

Legal Framework

GMRA, CASS, and the UK’s Permissive Regime

The Global Master Repurchase Agreement

The GMRA is “a model legal agreement designed for parties transacting repos” published by ICMA. It has been updated several times: GMRA 2000, GMRA 2011, and ongoing annexes for digital assets. ICMA publishes annual legal opinions covering 73 jurisdictions as of 2025, confirming the enforceability of close-out netting provisions.

Under the GMRA’s standard terms, rehypothecation is the default position unless explicitly restricted in Annex I of the agreement. Banks insist on broad rehypothecation rights; counterparties, particularly hedge funds, may negotiate caps on reuse or “insist on same quality return and full traceability”.

The FCA’s Client Assets Sourcebook (CASS)

The FCA’s CASS rules require firms holding client assets to disclose rehypothecation practices and obtain client consent. Unlike the SEC’s quantitative 140% cap, the UK approach is disclosure-based rather than quantity-limited. The FCA has proposed targeted clarifications of CASS 6 and CASS 7 through consultation CP25/37, published in December 2025, which would “require firms to update processes, governance documentation and consumer disclosures”. The consultation period closed on 27 January 2026, and a final policy statement is expected in the second quarter of 2026, with rule changes effective three months thereafter.

The US Contrast

SEC Rule 15c3-3

The United States imposes a statutory cap on rehypothecation. SEC Rule 15c3-3, the “customer protection rule” adopted in 1972, permits broker-dealers to rehypothecate customer assets up to 140% of the customer’s debit balance. This cap applies only to margin accounts; fully paid securities are excluded from rehypothecation. The SEC recently amended Rule 15c3-3 to require daily reserve computations for certain broker-dealers, with compliance extended to 30 June 2026.

The asymmetry between the permissive UK regime and the capped US regime has made London a global centre for prime brokerage and securities financing. US firms have used European subsidiaries to circumvent domestic caps, transferring client assets to UK affiliates where no statutory cap applies. This cross-border arbitrage was highlighted in the Lehman collapse and remains a source of regulatory concern.

The UK’s permissive regime is a competitive strategy – attracting financial activity by offering lighter regulation. This is regulatory arbitrage dressed as “market efficiency”. The state could impose a statutory cap like the US. It chooses not to, because the City of London’s profitability depends on facilitating leveraged speculation. This is a political choice with systemic consequences.

Ethical Dimensions

Consent, Disclosure, and the Moral Hazard Problem

The Consent Question

Rehypothecation is legal only with client consent. But what constitutes meaningful consent? Prime brokerage agreements typically bury rehypothecation rights in fine print, often granting the prime broker “carte blanche” to rehypothecate client assets without specific transaction-level authorisation. After Lehman, some hedge funds negotiated caps on the proportion of assets that could be rehypothecated – for example, no more than 50% of posted collateral – but such restrictions remain rare.

The ethical problem is acute: the client who posts gilts as collateral believes it retains a claim on those gilts. It does not. In the event of prime broker default, the client discovers that its assets are now in the hands of a third-party bank. This was the devastating discovery made by LBIE’s clients on 15 September 2008.

Systemic Moral Hazard

Rehypothecation creates a moral hazard problem at two levels. First, prime brokers have an incentive to reuse collateral aggressively because rehypothecation generates revenue (e.g., through lending fees or reduced funding costs). This revenue allows them to offer clients better terms on leverage, creating a competitive dynamic that encourages ever-longer rehypothecation chains.

Second, the original collateral provider may be less concerned about the default risk of its immediate counterparty if it believes the system is too big to fail. This moral hazard has been studied in the literature, which finds that “as the moral hazard problem gets more severe, the borrower is less concerned about the default risk of the intermediary, resulting in indirect financing being chosen more frequently”.

The Collateral Illusion

The financial press describes rehypothecation as creating “an invisible tower of interconnected risk”. This tower is built on a collateral illusion: the same £100 million of gilts appears on multiple balance sheets, inflating the perception of safe assets. Academic research has shown that “rehypothecation enhances provision of funding liquidity to the economy, but it also incurs deadweight cost by misallocating the asset among the agents when counterparties fail”.

The ethical question is whether this illusion is a form of systemic deception. Proponents argue that rehypothecation is simply the efficient reuse of scarce collateral. Critics argue that it obscures the true extent of leverage and creates hidden interdependencies that no single market participant can see.

The “collateral illusion” is not a bug; it is the feature that makes rehypothecation profitable for financial intermediaries. By creating multiple claims on the same asset, the system generates fees, spreads, and trading volume. But when the illusion collapses, the state bears the cost. This is privatised profit and socialised risk – the defining characteristic of extractive finance.

Operational Impacts

How Rehypothecation Affects Gilt Yields

Rehypothecation affects gilt yields through three channels.

The Collateral Scarcity Premium

When rehypothecation chains are long, the same gilt collateral is in high demand. This demand reduces repo rates (the cost of borrowing gilts) and compresses the spread between gilt yields and risk-free rates. A lower repo rate means cheaper funding for leveraged gilt positions, which can encourage more basis trading and put downward pressure on cash gilt yields.

The Leverage Amplifier

Rehypothecation allows a given stock of gilts to support multiple leveraged positions. The leverage multiplier can be approximated by:

Multiplier ≈ 1 / (1 - r × (1 - h))

where r is the rehypothecation rate (percentage of collateral reused) and h is the haircut. If rehypothecation rates are high and haircuts low, the multiplier can exceed 3–5×. This amplified leverage can drive large directional flows in gilt markets, affecting yields.

The Liquidity Shock Amplifier

When a chain breaks – for example, when a prime broker defaults or when sharp yield movements trigger margin calls – collateral can become trapped downstream, and forced selling can cascade. This was the mechanism observed in the 2022 LDI crisis, where “selling pressure in gilt markets – due to deteriorating derivative and repo positions of liability-driven investors (LDI) – led to evaporating market liquidity, especially in long-dated conventional gilts and index-linked gilts”.

The Financial Stability Board has noted that “both re-hypothecation and collateral re-use increase the availability of collateral, reduce the cost of using collateral, and consequently reduce transaction and liquidity costs”, but that “market-based finance, in particular its work to dampen procyclicality and other financial stability risks in securities financing transactions such as repos” is essential.

These “operational impacts” are not externalities; they are the direct consequences of a policy choice to permit extensive rehypothecation. The state could limit chain length, impose minimum haircuts, or require segregation of client assets. It chooses not to, because the financial sector demands the flexibility. When the system fails, the state must intervene. This is not market discipline; it is policy-created fragility.

Case Study

Lehman Brothers International (Europe)

The Collapse

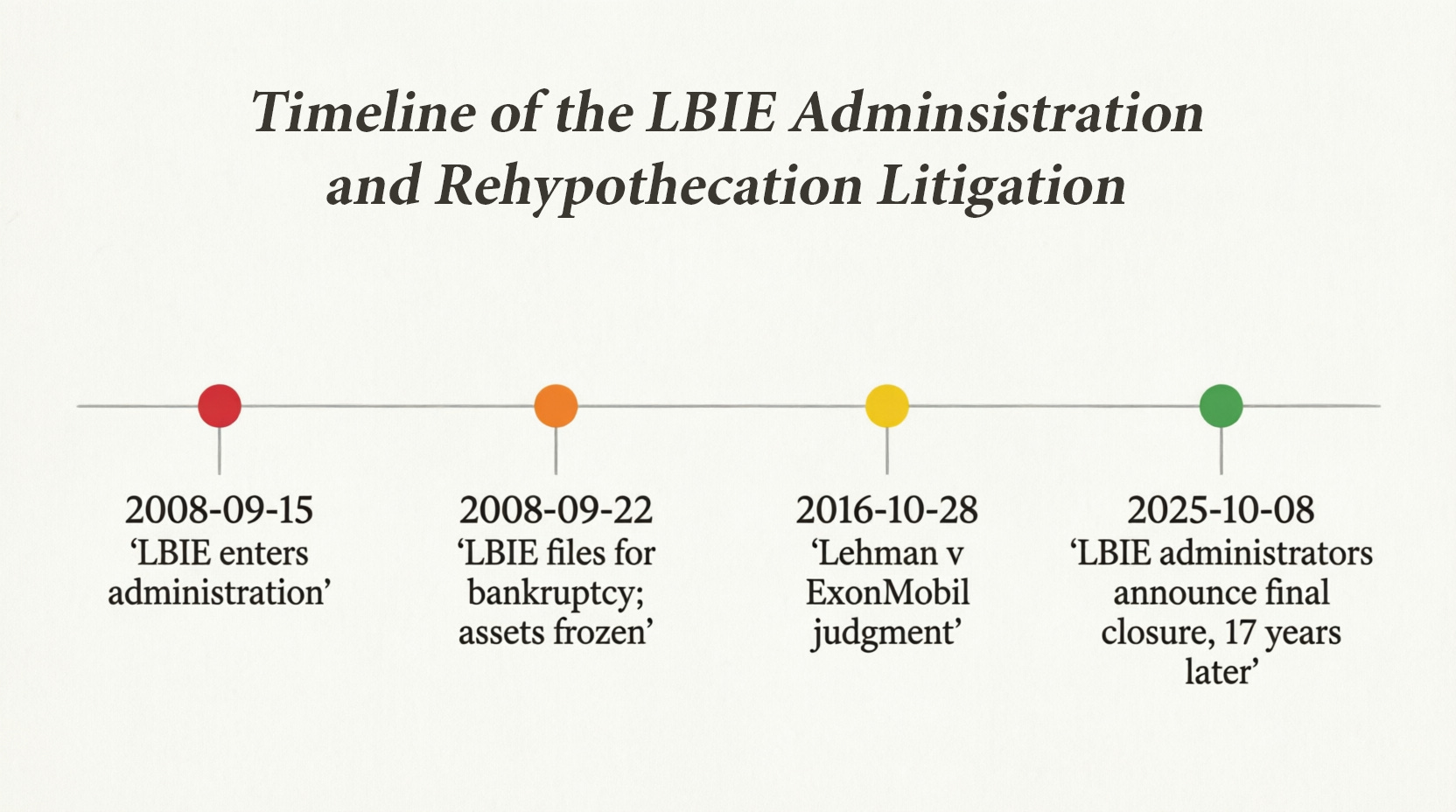

At 7:56 am London time on 15 September 2008, administration proceedings commenced for Lehman Brothers International (Europe), the largest and most complex part of the Lehman empire. At the moment of collapse, LBIE held more than $22 billion of its clients’ securities that had been rehypothecated. When LBIE failed, these clients became unsecured creditors of the LBIE estate. Their assets were frozen; retrieving them became “a long and tortuous process”.

The return of assets to LBIE’s clients took years. PwC, the administrator, was paid £1 billion for its work, with another £489 million paid out in legal costs. The process was still ongoing more than a decade later.

The ExxonMobil Litigation

The landmark case of Lehman Brothers International (Europe) v ExxonMobil Financial Services BV [2016] EWHC 2699 (Comm) became the leading English authority on close-out valuation under the GMRA 2000. The core dispute involved a repo where EMFS had lent US$250 million to LBIE, receiving a diversified portfolio of equities and bonds as collateral. When LBIE defaulted, EMFS sought to close out the transaction under the GMRA.

The court ruled on several key issues that reshaped the GMRA’s interpretation:

The meaning of “close of business”: Lehman argued that “close of business” meant 5:00 pm; Exxon contended it meant 7:00 pm. The court concluded that the term showed “an intention to provide a degree of flexibility”, and that if a definite cut-off time were intended, “this would have been expressly specified in the GMRA”. In the case at hand, a default notice received at or shortly after 6:02 pm was valid.

The validity of service by e-mail: The court confirmed that electronic service was acceptable under the GMRA.

The exercise of contractual discretion: The majority of EMFS’s close-out valuations were vindicated; LBIE’s proposed valuations were not upheld.

The litigation demonstrated that rehypothecation chains create ferociously complex legal disputes that can last for years. But the lesson for the original collateral provider is even starker: LBIE’s hedge fund clients had no claim on the specific gilts they had posted; they became unsecured creditors, receiving only a fraction of their value after a decade of legal battles.

The Lehman collapse revealed the operational reality of rehypothecation: clients think they own their assets, but they own only a claim on their prime broker. When the prime broker fails, that claim becomes worthless. The state could prevent this by requiring asset segregation or limiting rehypothecation. It chooses not to, because the City demands the flexibility. The £1.5 billion in legal costs were not a “market failure”; they were the predictable consequence of a permissive regulatory framework.

Case Study

The 2022 LDI Crisis (Rehypothecation-Adjacent)

The Liability-Driven Investment crisis of September 2022 was not solely a rehypothecation crisis, but rehypothecation and collateral reuse played amplifying roles. LDI funds used interest rate swaps and gilt repos – both involving collateral reuse – to hedge pension scheme liabilities. When gilt yields spiked, margin calls surged. LDI funds’ repo borrowing increased sharply.

The Bank of England’s analysis revealed that “a 1 per cent rise in linker repo exposure prior to the crisis resulted in a 0.49 per cent rise in gilt liquidations between 23 September and 14 October“. Forced sales of gilts – many of which had been rehypothecated – drove yields higher, triggering further margin calls. The Bank was forced to intervene as a buyer of last resort, announcing a temporary £65 billion purchase programme for long-dated gilts and a Temporary Expanded Collateral Repo Facility (TECRF) to ease liquidity pressures.

The LDI crisis demonstrated that rehypothecation chains, when stressed, can collapse suddenly, and that the state must step in as buyer of last resort. The Bank of England’s September 2025 discussion paper on enhancing gilt repo market resilience was explicitly designed to prevent a recurrence by strengthening the plumbing of collateralised lending.

The LDI crisis was not a “market failure” but a policy-created crisis. The state encouraged pension funds to use LDI strategies through regulatory frameworks (Solvency II, pension fund accounting rules). The state permitted extensive rehypothecation through the GMRA and CASS. The state’s own policy announcement (the mini-budget) triggered the yield spike. And when the strategies failed, the state had to intervene. This is the circularity of modern finance: the state creates the conditions for speculative excess, then rescues the system when that excess unravels.

The Debate

Does Rehypothecation Serve the Productive Economy?

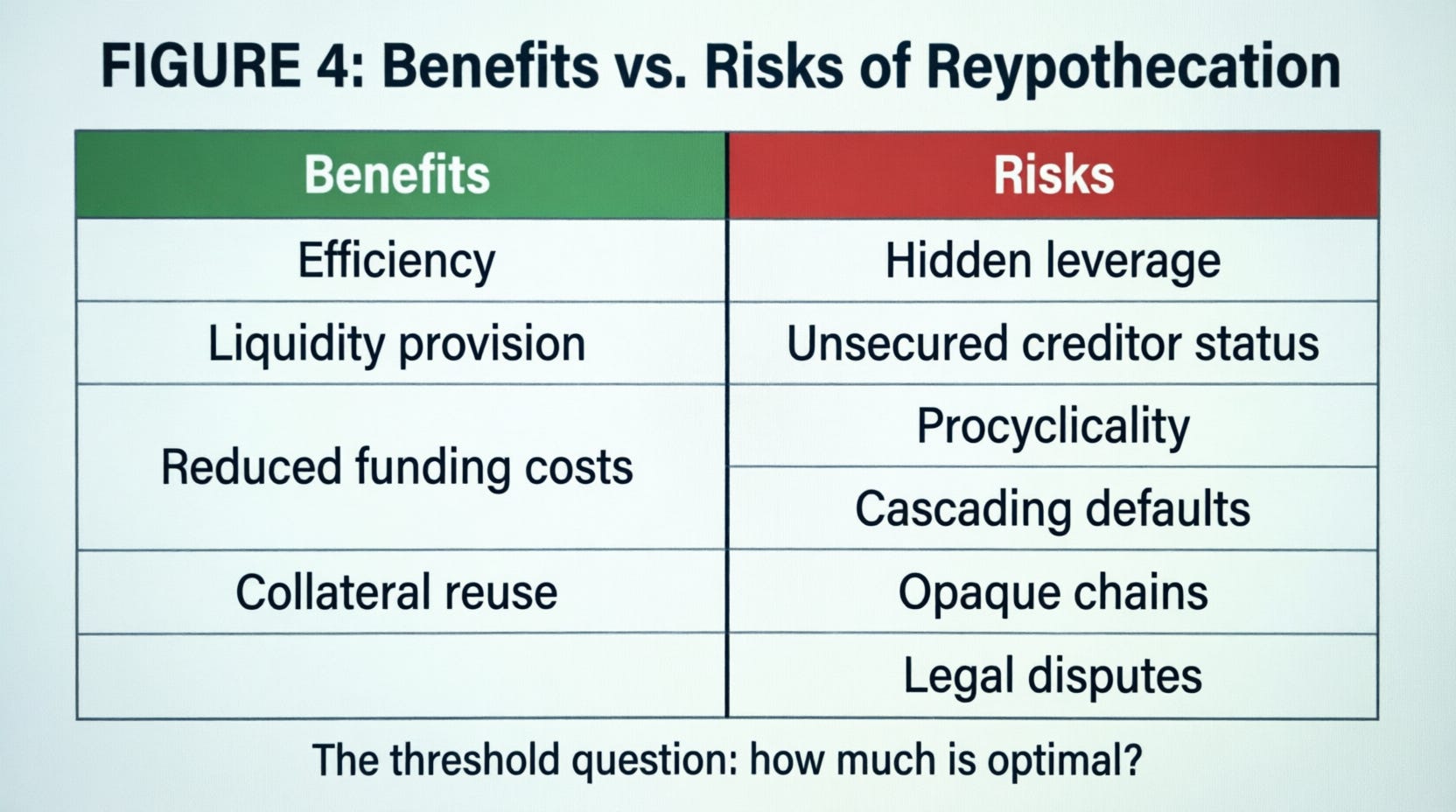

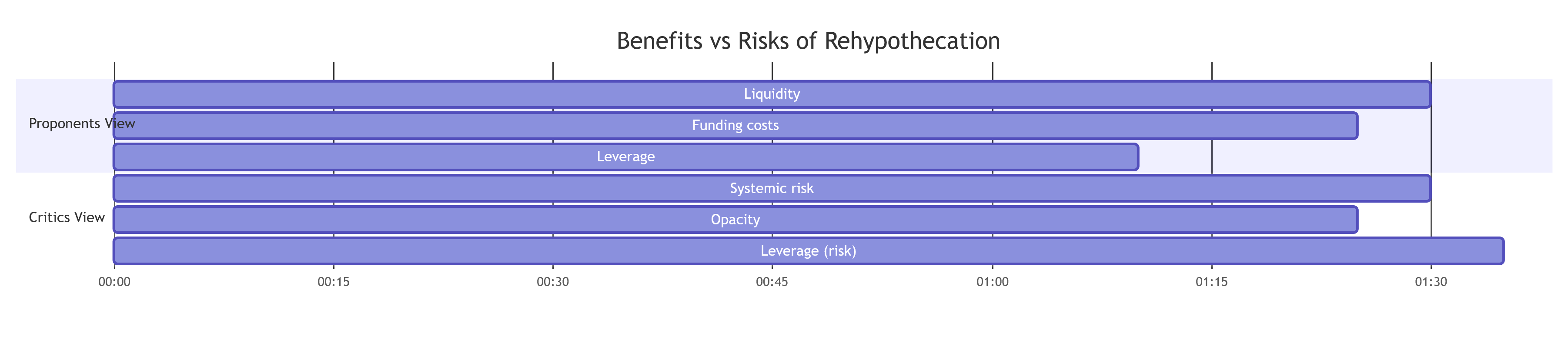

The Efficiency Case

Proponents argue that rehypothecation is essential market lubricant. As one industry observer put it: “Saying that re-hypothecation should be limited by broker/dealers is like saying the grocery store you buy a carton of milk from should be constrained from using the cash you give them to pay the wholesaler”. On this view, rehypothecation reduces funding costs, increases liquidity, and enables the efficient reuse of scarce collateral.

Academic research supports this position. Studies have shown that “rehypothecation improves resource allocation because it permits liquidity to flow where it is most needed”. The liquidity benefits of rehypothecation “are shown to be more important in high inflation (high interest rate) regimes”. Rehypothecation “enhances provision of funding liquidity to the economy” and “economises on scarce collateral”.

The Systemic Risk Case

The opposing view is that rehypothecation creates hidden leverage, opaque chains, and “deadweight cost by misallocating the asset among the agents when counterparties fail”. The Financial Stability Board has warned that “both re-hypothecation and collateral re-use increase the availability of collateral, reduce the cost of using collateral, and consequently reduce transaction and liquidity costs” at the same time as introducing “procyclicality and other financial stability risks”.

The collapse of LBIE is the canonical example of rehypothecation’s catastrophic potential. PwC’s administration of LBIE took 17 years and cost £1.5 billion. The original collateral providers received only a fraction of their assets. The IMF has estimated that global banks’ exposure to non-bank financial institutions, including leverage enabled by rehypothecation chains, stands at $4.5 trillion.

The Threshold Question

Drawing on the IMF’s financial deepening research, the question for rehypothecation is not whether it should exist but how much is optimal. A certain level of collateral reuse is necessary for market functioning. Beyond a threshold, however, additional reuse ceases to improve liquidity and begins to increase systemic fragility. The empirical question – where that threshold lies – remains unresolved.

The “efficiency” argument conflates private efficiency (profitability for financial intermediaries) with social efficiency (benefits for the real economy). Rehypothecation may be efficient for prime brokers, but it creates systemic risks that are socialised when the state intervenes. The IMF’s $4.5 trillion exposure figure is not a measure of economic value; it is a measure of hidden leverage. The MMT question is: what productive purpose does this leverage serve? The answer is: very little. It is speculative churn, pure and simple.

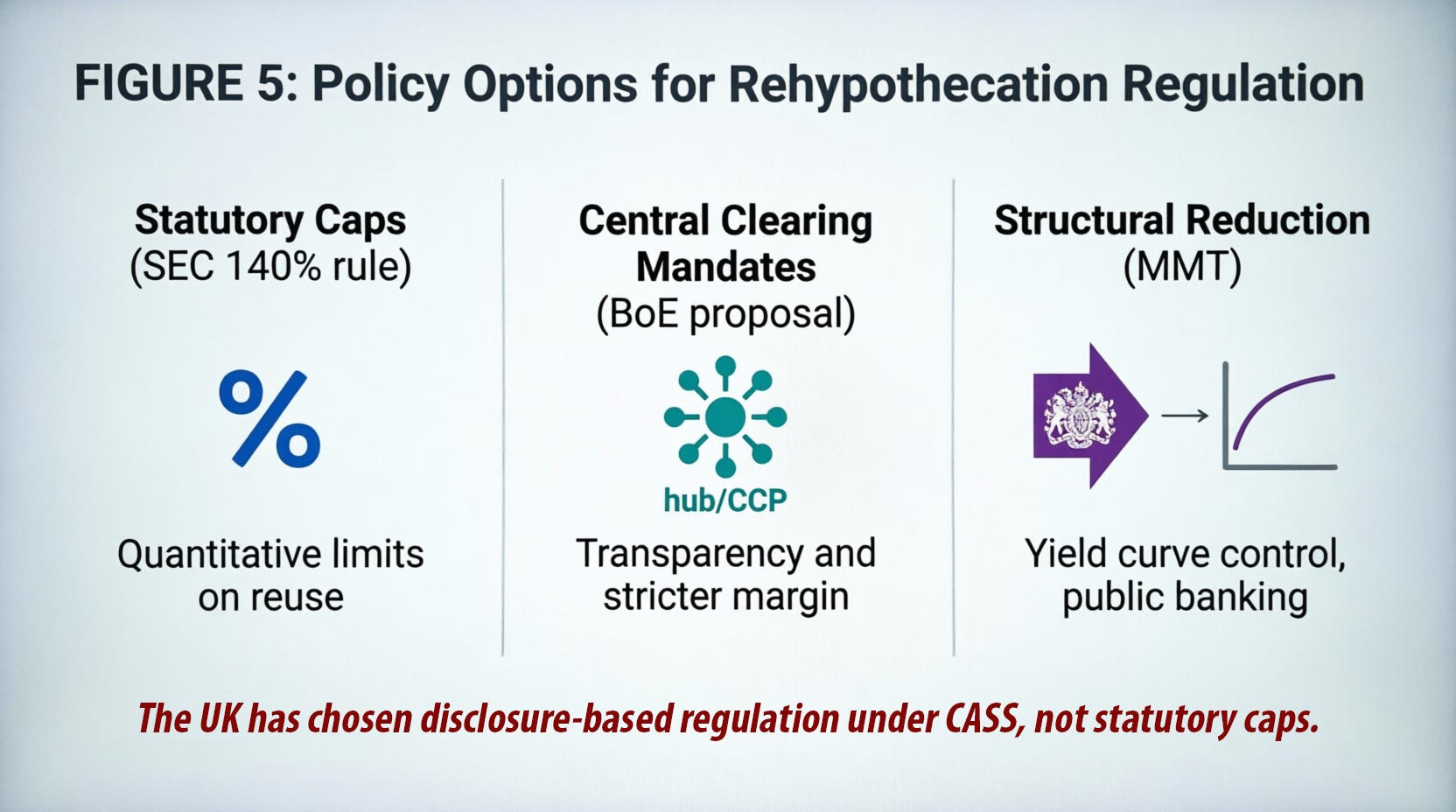

Policy Implications

Restriction, Transparency, or Abolition?

The US Model: Statutory Caps

The SEC’s 140% cap on rehypothecation of customer assets is the most direct regulatory approach. The cap limits the extent to which a prime broker can reuse client collateral. Combined with the SEC’s customer protection rule, it provides a quantitative backstop.

The UK has not adopted such a cap, preferring a disclosure-based regime under CASS. The FCA’s CP25/37 consultation would tighten CASS requirements but stop short of imposing a statutory limit on reuse. There is no indication that the Treasury or FCA intend to adopt a US-style cap.

Central Clearing Mandates

The Bank of England’s September 2025 discussion paper explored mandatory central clearing as a tool to reduce counterparty risk in the gilt repo market. Central clearing would bring repos into a CCP environment with transparent margin requirements, mutualised default funds, and real-time visibility into aggregate positions. This would not eliminate rehypothecation but would impose stricter collateral and haircut requirements, reducing the length of rehypothecation chains and the opacity of leverage.

The industry response has been mixed. ICMA strongly opposes mandatory clearing, arguing that “this would increase costs and restrict access for some participants” and that “clearing should be a commercial choice”. The BoE’s April 2026 Feedback Statement acknowledged this resistance while affirming that “further action is needed to deliver structural improvements to the resilience of the gilt repo market”.

MMT’s Alternative

Structural Reduction of Speculative Finance

Modern Monetary Theory offers a more radical alternative: reduce the scale of speculative finance such that rehypothecation becomes less necessary in the first place. If the central bank adopted explicit yield curve control, eliminating the need for basis trades and other speculative strategies, the demand for collateral reuse would fall. If the government directed credit through a public banking system, bypassing the shadow banking chains that depend on rehypothecation, the financial sector would shrink to a size that serves the real economy.

MMT would argue that the debate over rehypothecation caps misses the larger point: the practice exists because the financial system has been structured to prioritise private leverage over public purpose. Reducing the scale of speculative finance reduces the need for rehypothecation. The question is political, not merely technical.

The policy options are not equally valid. Statutory caps and central clearing mandates tinker with the existing system; they do not challenge it. MMT would go further: if rehypothecation creates systemic risks that require state bailouts, and if the practice serves speculative rather than productive purposes, then the state should restrict or abolish it. The constraint is not “market efficiency”; it is political will.

The MMT Perspective

Rehypothecation as a Policy Construction

The State’s Ultimate Authority

From an MMT perspective, rehypothecation is not an inevitable feature of market economies. It is a policy construction. The practice exists because the state chooses to permit it. The state could choose to restrict it – by imposing a statutory cap, by mandating central clearing for all repos, or by altering the structure of financial incentives that make rehypothecation profitable.

The state’s ultimate authority is demonstrated in moments of crisis. In 2022, the Bank of England stepped in as buyer of last resort, overriding the market’s price discovery. In 2008, the Bank of England and the Treasury intervened to stabilise the financial system. The state is always the backstop.

Rehypothecation as Extractive Rent-Seeking

MMT would argue that rehypothecation, at its current scale, is extractive. It diverts talent and capital away from productive activity. It creates systemic fragilities that require taxpayer-funded bailouts. It transfers wealth from the real economy to the financial sector. The original collateral provider – often a pension fund or an insurer – lends its assets to the shadow banking system and receives only a fraction of the value created by the reuse chain.

The academic literature distinguishes between rehypothecation and securitisation as alternative forms of collateral reuse, but MMT would question why either is necessary at the current scale. If the legitimate purposes of collateral reuse – liquidity provision, funding efficiency – can be achieved with far shorter chains and lower multipliers, then the current system is indeed extractive.

The Tension Between Efficiency and Stability

MMT does not deny that rehypothecation provides liquidity benefits in normal times. But it argues that the trade-off between efficiency and stability is not fixed. The optimal level of rehypothecation is a political judgement, not an economic law. The UK has made a political choice to permit extensive reuse. The US has made a different choice, imposing a statutory cap. The lesson of LBIE is that the permissive choice carries catastrophic risks that can materialise with little warning.

The “efficiency vs. stability” framing is a false dichotomy. The state could have both efficiency and stability by: (1) requiring asset segregation to protect clients, (2) limiting chain length to prevent excessive leverage, and (3) providing public liquidity facilities to reduce dependence on private collateral reuse. The current system prioritises private efficiency (profitability for intermediaries) over public stability. This is a political choice, not an economic necessity.

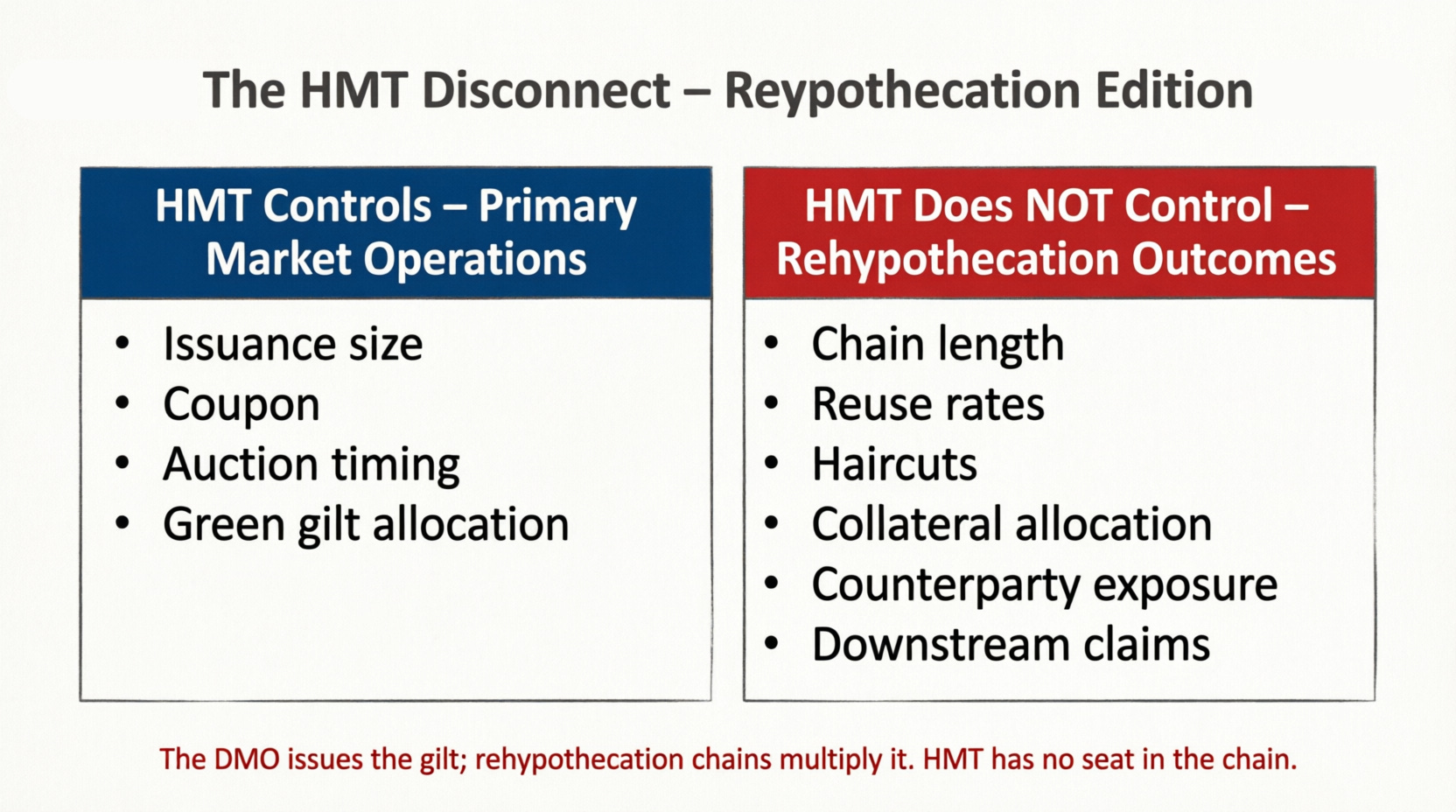

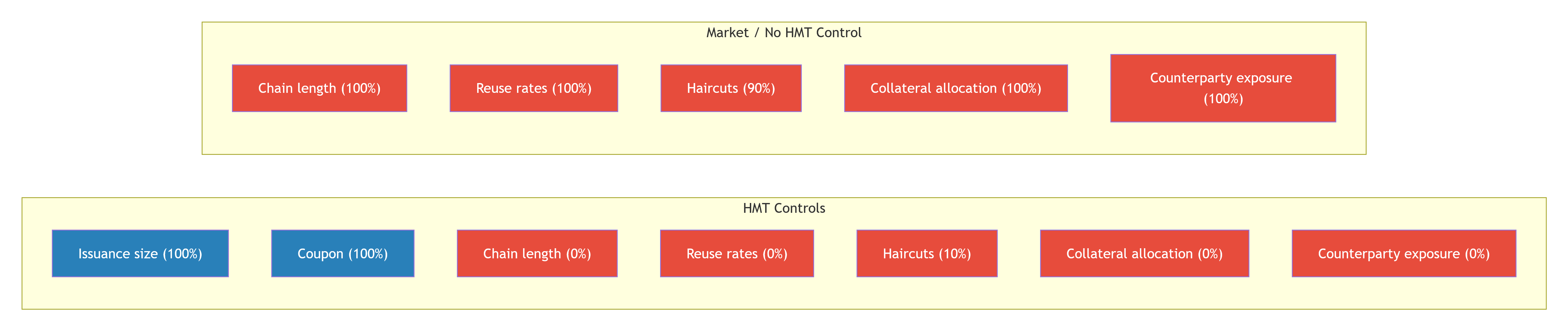

The HM Treasury Disconnect

Why Yields Are Not a Policy Tool

The unifying theme across this series is that HM Treasury does not control the yields that emerge from the secondary market. Rehypothecation is the most vivid illustration of this disconnect.

HM Treasury, through the DMO, issues the gilt. It sets the coupon and the auction price. From that point forward, the gilt enters the secondary market, where it can be rehypothecated multiple times. HM Treasury has no visibility into these chains, no authority to restrict them (beyond general financial regulation), and no influence over the funding conditions that determine the price of the gilt in each subsequent transaction. Yet the yields that emerge from rehypothecation chains affect the government’s borrowing costs, the pricing of corporate debt, and the cost of mortgages.

The DMO does not know – and does not need to know – how many times a particular gilt has been rehypothecated. It does not know which prime broker is reusing whose collateral. It does not know the length of the chain or the counterparty exposure. This opacity is not a failure of the DMO; it is a feature of the market structure. But it means that HM Treasury is governing in the dark.

The question for democracy is whether this opacity is acceptable. If the gilt market is “fundamental to the broader UK financial system and real economy”, should the elected government have any authority over the collateral chains that determine gilt yields? The current answer is no. The Bank of England monitors liquidity; the Treasury issues debt; the DMO manages the portfolio. But the collateral chains are governed by the GMRA, a private contract between market participants. The state is present only at the boundaries – when a default occurs, when a bailout is required, when a crisis forces intervention.

This is not “governing in the dark”; it is choosing not to govern. The state could require reporting of rehypothecation chains, impose position limits, or mandate central clearing. It chooses not to, because the financial sector demands opacity to maximise profitability. The “HM Treasury disconnect” is not an operational constraint; it is a political choice to delegate yield determination to unaccountable private actors.

Conclusion

The Invisible Tower and the Absent Treasury

Rehypothecation is the hidden plumbing of the gilt market. It enables immense liquidity from a finite pool of assets, greasing the wheels of the financial system. But it also builds an invisible tower of interconnected risk where one failure can trigger a catastrophic collapse.

The legal framework is permissive: title transfer under the GMRA gives prime brokers the right to reuse client collateral by default. The UK’s disclosure-based regime, in contrast to the SEC’s statutory cap, has made London a global centre for prime brokerage. The ethical dimensions are troubling: consent is often buried in fine print, and the original collateral provider becomes an unsecured creditor in the event of default. The operational risks are severe: when a chain breaks, collateral can be trapped downstream, and forced selling can cascade.

The Lehman administration remains the cautionary tale. $22 billion of client assets were rehypothecated, the administration took 17 years, and legal costs exceeded £1.5 billion. The ExxonMobil litigation clarified GMRA close-out provisions but did not restore the original collateral providers’ assets. The 2022 LDI crisis, while not solely a rehypothecation crisis, demonstrated the same amplifying mechanism: collateral reuse created chains that, when stressed, required state intervention.

Policy options range from statutory caps (the US approach) to central clearing mandates (the BoE’s preferred path) to structural reduction of speculative finance (the MMT alternative). The UK has chosen none of these, preferring a disclosure-based regime under CASS, with targeted clarifications proposed in CP25/37.

The fundamental constitutional reality remains: HM Treasury does not control rehypothecation. It issues the gilt; the market determines how many times it is reused. The yields that emerge from the secondary market are shaped by these hidden chains. No minister is present when a prime broker decides to rehypothecate a client’s gilts to a clearing bank. The invisible tower governs yields; the Treasury governs the issuance. The question for democracy is whether the market should be accountable to anyone.

The invisible tower is not inevitable. It is built on policy choices: to permit title transfer, to accept disclosure-based regulation, to prioritise City competitiveness over systemic stability. The state could dismantle the tower, brick by brick: by requiring asset segregation, by limiting chain length, by imposing statutory caps, by providing public alternatives to shadow banking. The constraint is not technical feasibility; it is political will. The question is whether we have the courage to subordinate finance to the public purpose, or whether we will continue to permit an invisible tower of risk to govern the cost of public debt.

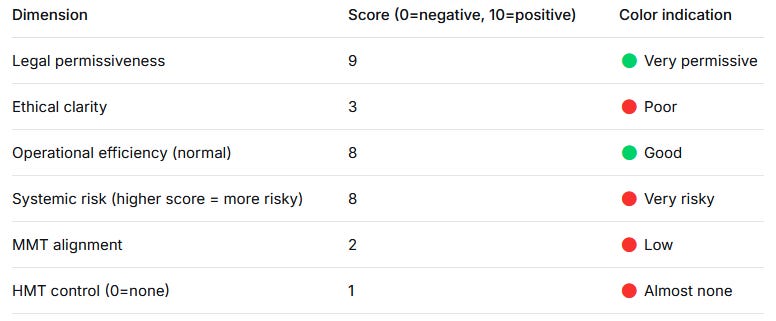

[FIGURE 7: Summary Assessment – Rehypothecation and the Real Economy]

Other Gilt Related Articles

Gilt Derivatives

The yield you see is not the yield you get (and why HM Treasury has no seat at this table)

References

Diversification.com (2026a) Rehypothecation explained: definition, examples, and impacts. Savings Grove, 25 January. Available at: https://www.savingsgrove.com

Diversification.com (2026b) Rehypothecation: meaning, criticisms & real-world uses. Available at: https://www.diversification.com

Financial Conduct Authority (2025) CP25/37: Targeted clarifications of the FCA Handbook. Consultation paper, 9 December. London: FCA. Available at: https://www.fca.org.uk

Financial Stability Board (2017a) FSB publishes reports on the re-hypothecation of client assets and collateral re-use. Press release No. 2/2017, 25 January. Basel: FSB. Available at: https://www.fsb.org

Financial Stability Board (2017b) Re-hypothecation and collateral re-use: potential financial stability issues, market evolution and regulatory approaches. Report, 25 January. Basel: FSB. Available at: https://www.fsb.org

High Court of Justice, Queen’s Bench Division, Commercial Court (2016) Lehman Brothers International (Europe) v ExxonMobil Financial Services BV [2016] EWHC 2699 (Comm). Case No: 2014 FOLIO 1006, 28 October. Available at: https://www.caselaw.nationalarchives.gov.uk

International Capital Market Association (2025a) ICMA publishes 2025 legal opinion updates for the Global Master Repurchase Agreement. News in Brief, 14 April. London: ICMA. Available at: https://www.icmagroup.org

International Capital Market Association (2025b) ICMA GMRA 2025 legal opinions. Securities Finance Times, 2 October. London: ICMA. Available at: https://www.icmagroup.org

InvestorsHub (2025) Lehman Brothers International (Europe) administration concludes after 17 years. 8 October. Available at: https://www.investorshub.com

Leaman Crellin (2025) FCA CP25/37: proposed changes to CASS 6 and CASS 7 and what firms need to do next. 11 December. Available at: https://www.leamancrellin.co.uk

Norton Rose Fulbright (2016) Lehman Brothers International (Europe) v ExxonMobil Financial Services B.V. [2016] EWHC 2699 (Comm). Knowledge publication, October. Available at: https://www.nortonrosefulbright.com

Pinter, G. (2023) The 2022 gilt market crisis: a working paper analysing transaction-level data. Bank of England Staff Working Paper, 3 April. London: Bank of England.

Regulation Tomorrow (2025) FCA publishes CP25/37 on targeted clarifications of the FCA Handbook. 9 December. Available at: https://www.regulationtomorrow.com

Reuters (2022) BoE’s repo facility to ease pension pain is no silver bullet, sources say. Yahoo Finance, 13 October. Available at: https://www.finance.yahoo.com

Securities and Exchange Commission (1972) Rule 15c3-3: Protection of customer assets. As amended 2025–2026. Washington, D.C.: SEC. Available at: https://www.sec.gov

Sidley Austin LLP (2025) SEC amends Rule 15c3-3 to require daily reserve computations for certain broker-dealers. Insights, 24 November. Available at: https://www.sidley.com

UK Parliament, Treasury Committee (2022–2023) LDI crisis evidence. House of Commons. London: HMSO.