The Ghost That Will Not Die

Why the UK Government Is Not a Household (and Why Gilts Are Sleight of Mouth)

A Graphic Novella

For centuries, the language of debt has shrouded the British state’s relationship with its own currency. Gilts are routinely described as ‘government borrowing’, and rising yields are presented as the bond market’s verdict on fiscal profligacy. This article goes further: it argues that even under metal pegs—from the tally stick to the gold standard—what became known as ‘debt’ was always an added means of state provision by fiat. Sovereign liability issuance is, and always has been, an unconditional act of monetary sovereignty, not a loan extracted from private savers.

By tracing the institutional history from the tally stick to the gilt edged bond, and by demonstrating—using the Bank of England’s own operational manuals—that the UK government never borrows sterling, a different picture emerges. The so called ‘National Debt’ is a voluntary savings vehicle for the private sector and a tool of monetary policy. The real constraint on public spending is not the bond market, but the availability of real resources and the risk of inflation. Overturning the borrowing frame is not a matter of theoretical interpretation; it is a matter of reading what the institutions themselves say they do.

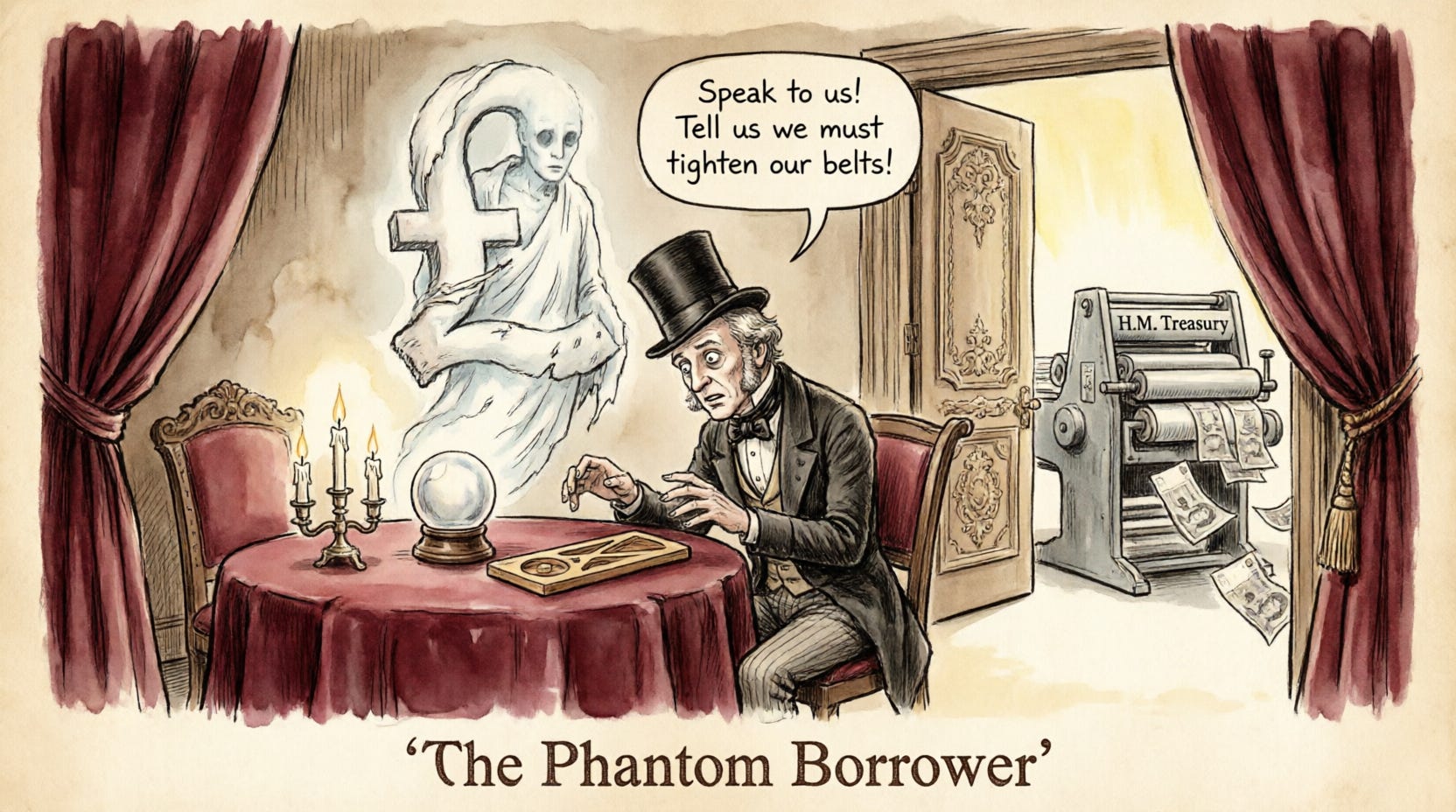

The Phantom Borrower

In the public imagination, a UK government gilt is an IOU—a piece of paper that proves the state has borrowed money from the private sector. When gilt yields rise, newspapers warn that Britain’s borrowing costs are surging. Politicians invoke the spectre of the bond vigilante to justify austerity. Almost every word of this framing, from a modern monetary perspective, is wrong.

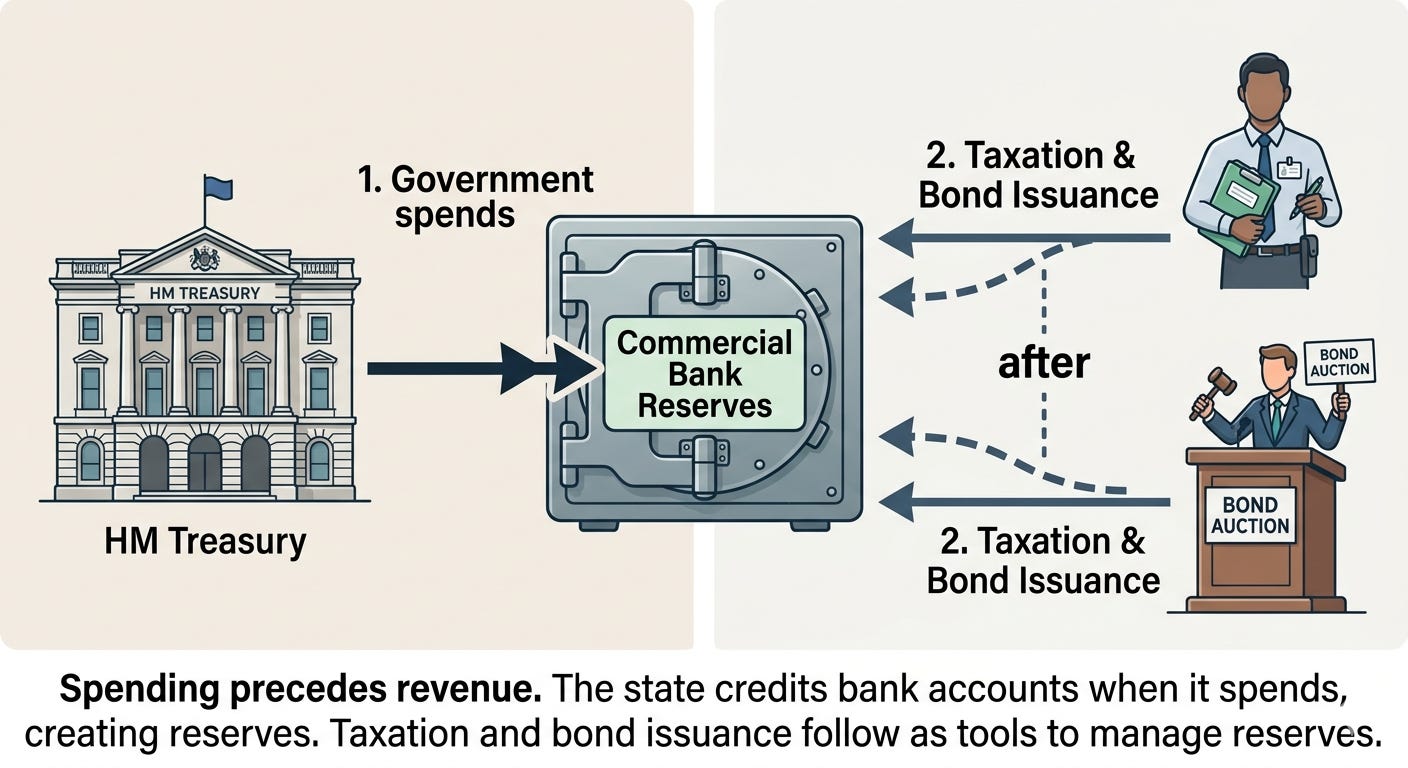

The UK issues its own floating rate, non convertible currency: sterling. It is a monetarily sovereign state. As such, it never needs to obtain its own currency from anyone else before it can spend. The government is not a household; it is the sole manufacturer of the pounds in which its liabilities are denominated. Gilts are not a financing operation but a post spending reserve management tool—an interest bearing alternative to central bank reserves. The persistent misrepresentation of gilts as ‘borrowing’ is not an innocent metaphor. It is a political weapon, wielded to enforce fiscal discipline and protect the interests of asset holders.

This article provides an institutional and historical account of that misrepresentation. It begins with the origins of sovereign liability in the tally stick and the goldsmiths, moves through the gold standard and expeditionary warfare, and culminates in the modern operational architecture of the Bank of England and the Debt Management Office. Throughout, the argument is rooted in publicly available manuals, statutes, and balance sheet mechanics.

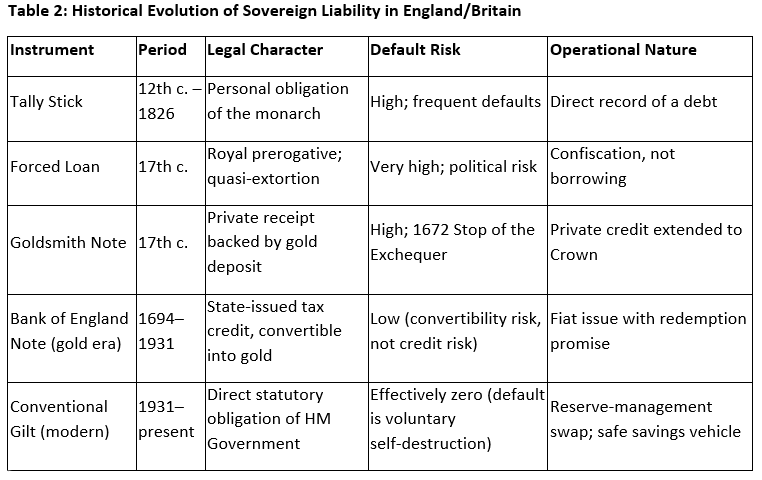

Tally Stick to Gilt Edged Bond: A History of Sovereign Liability

The Medieval Tally and the Italian Bankers

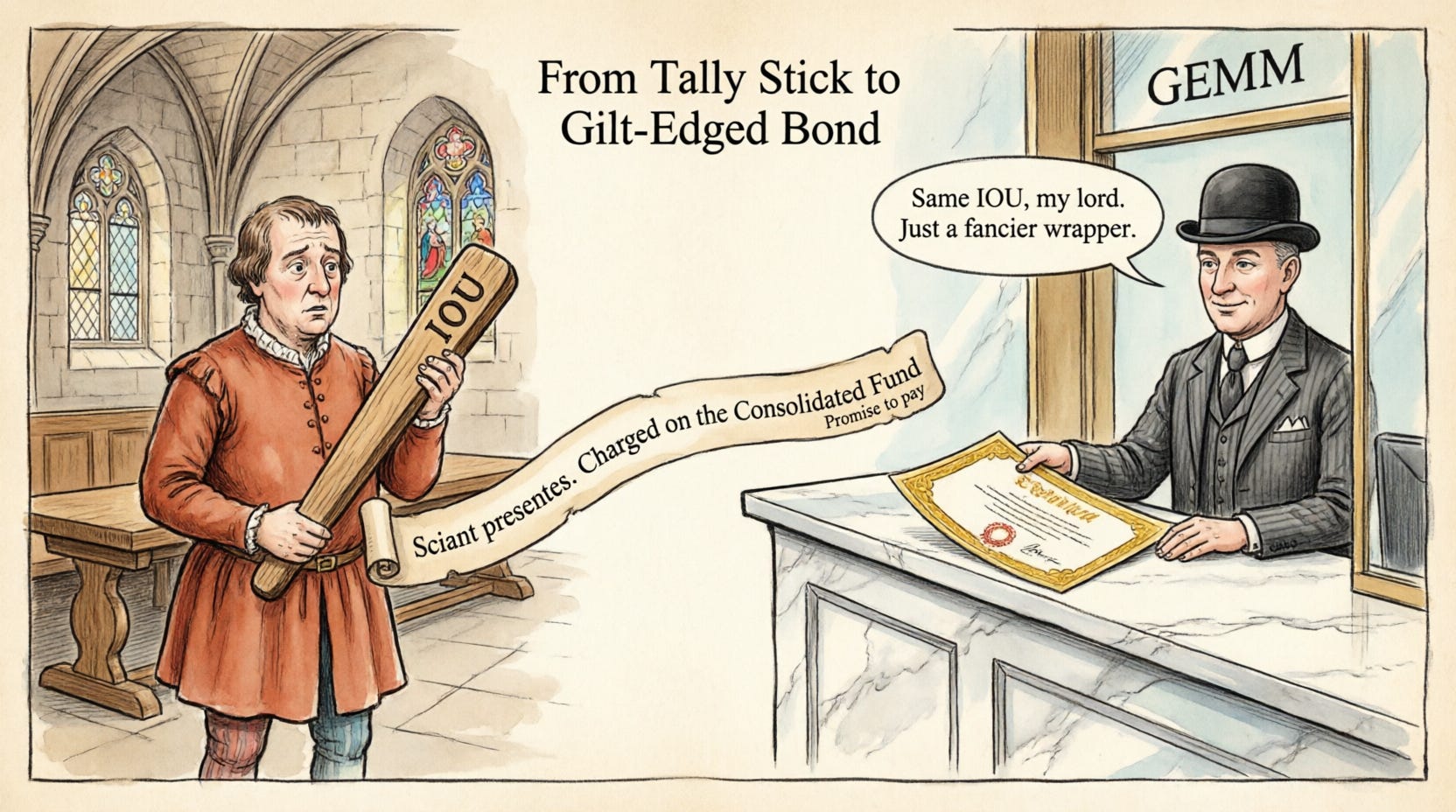

Before the Bank of England’s foundation in 1694, the English Crown’s credit arrangements were precarious. The earliest systematic instrument was the tally stick—a notched wooden stick split in two, with the Exchequer and the creditor each retaining a half as a matching record. Tallies were issued from the 12th century and functioned as a quasi currency, traded at a discount for hard cash. They represented a direct, personal obligation of the monarch.

For larger sums, the Crown relied on Italian merchant societies such as the Riccardi of Lucca and the Frescobaldi of Florence. These firms advanced credit for royal projects, particularly foreign wars. The relationship rested on personal trust in the sovereign, and it frequently ended in default when the Crown found itself unable or unwilling to repay.

The Stuarts, Forced Loans, and the Goldsmiths

Under the Stuarts, the absence of a reliable system of public credit became a source of political crisis. Monarchs resorted to forced loans—demands for money from wealthy subjects that were barely distinguishable from extortion. The Petition of Right (1628) was a direct response, attempting to prohibit the king from raising funds without Parliament’s consent.

In the 17th century, the Crown turned to the London goldsmiths. These craftsmen accepted deposits of gold and silver from the gentry and began lending a portion of those deposits at interest, issuing receipts that circulated as a form of paper money. The goldsmiths became significant lenders to Charles II. The arrangement collapsed in 1672 with the Stop of the Exchequer, when Charles simply suspended repayments. The default ruined many goldsmiths and demonstrated the fatal weakness of a system in which the state’s credit was indistinguishable from the monarch’s personal honour.

The ‘King’s Necessity’: The Fusion of Crown and State

The legal doctrine of the ‘King’s Two Bodies’ meant that a monarch’s personal debts died with them. There was no permanent, impersonal state to stand behind a promise to pay. Yet the vast majority of royal borrowing was incurred for what we would now consider reasons of state—above all, war. The concept of the ‘King’s Necessity’ asserted the monarch’s prerogative to demand extraordinary revenue for the defence of the realm. The debts arising from equipping a fleet or putting down a rebellion were seen as obligations of the person charged by God with the realm’s defence, even though they were patently public in character.

This fusion of the personal and the political made the Crown’s credit abysmal. The monarch could not borrow cheaply without parliamentary backing; Parliament would not grant that backing without greater control over the Crown’s affairs. The result was a negative feedback loop that paralysed state finances and contributed directly to the revolutionary upheavals of the 17th century.

1694: The Depersonalisation of Debt

The founding of the Bank of England in 1694 was a constitutional revolution in public finance. The Bank was a private company that lent to the government, not the monarch, with repayment secured by a specific stream of tax revenues voted by Parliament. The liability became permanent, transferable, and impersonally guaranteed. This transformed a loan to a spendthrift king into a secure, interest bearing asset—the forerunner of the modern gilt.

The term ‘gilt edged’ originated in the 19th century, borrowed from the gilded edges of high quality stationery, to denote a security of the highest credit quality. It referred specifically to the absolute certainty of repayment. That certainty did not arise from prudent fiscal management in the household sense; it arose from an institutional architecture that made the state’s promise a statutory charge on the Consolidated Fund, ultimately backstopped by the Bank of England’s capacity to create sterling.

The Gold Standard and the Fiction of Borrowing

Expeditionary Warfare and the Demand for Gold

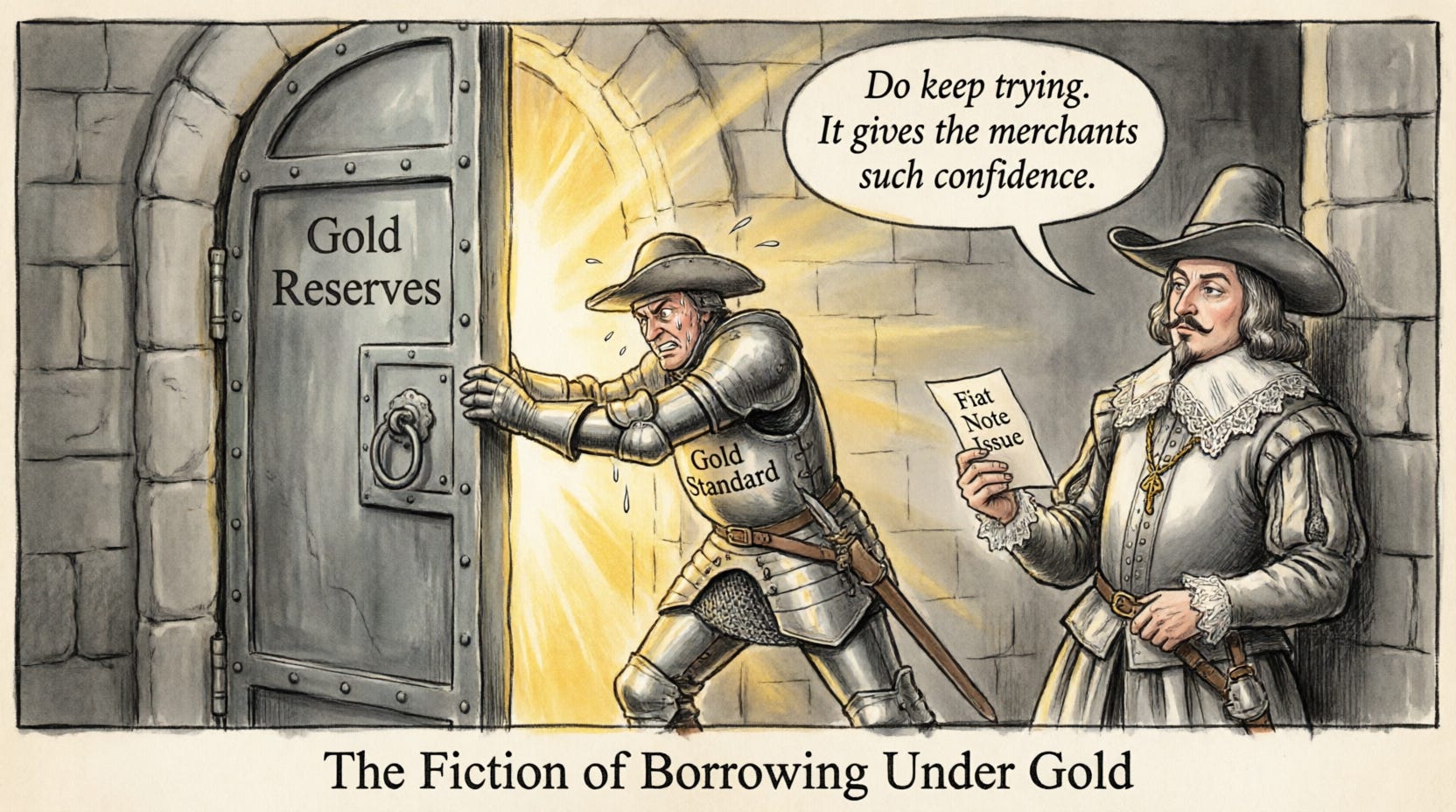

The gold standard, which Britain adopted de facto in the 18th century and formalised in 1821, is often held up as the era of genuine fiscal discipline—a time when governments were forced to ‘live within their means’. The reality is more subtle. Under gold, the government’s note issue was still a creature of fiat. Bank of England notes were state issued tax credits that happened to be convertible into gold at a fixed price. The tax foundation of the currency’s value preceded and underpinned the gold promise, not the other way round.

The real constraint of the gold standard was not a lack of sterling, but the obligation to defend the fixed gold parity. If the government spent too much paper into the economy, it risked inflation and a trade deficit. Foreign holders of sterling could then present their notes for conversion into gold, draining the Bank’s reserves. To stop the drain, the Bank had to raise interest rates sharply, deliberately causing a domestic recession. This is what happened in 1931, when the UK abandoned gold not because it had ‘run out of money’, but because the interest rates required to defend the parity were destroying the domestic economy.

Even Under Gold, ‘Borrowing’ Was a Metaphor

The crucial MMT insight is that even under a gold standard, the government was never operationally dependent on bond markets to fund its spending. It could always issue paper. The gold promise limited how far that could be pushed, but it did not transform the operation into a household style loan. The government was not ‘borrowing’ sterling from the private sector; it was issuing its own liabilities and promising to redeem them for gold on demand. The constraint was real—the gold reserve and the political will to defend it—but it was a self imposed policy constraint, not an operational funding necessity.

This is why, as the Bank of England’s own manuals confirm, the government’s capacity to spend has never been technically limited by its ability to ‘raise funds’ from bond markets. The bond issuance ritual persisted after 1931, but its rationale shifted entirely to reserve management and safe asset provision. The ‘borrowing’ frame is a ghost of the gold standard era—a political metaphor that has long since lost its mechanical foundation.

Fiat Before Gold: Why ‘Debt’ Was Always State Provision

The gold standard tempts even sympathetic readers to make a concession: yes, modern gilts are a monetary operation, but under metal pegs, governments really did borrow. That concession is historically illiterate and theoretically fatal. It accepts the very frame this article seeks to dismantle.

Consider the tally stick. When the Exchequer notched a stick and split it, the Crown did not first acquire wood from the creditor. It declared a liability ex nihilo—a royal promise to deliver value at a future date. The stick was not a receipt for a prior loan; it was the loan, brought into being by an act of sovereign fiat. The same holds for the forced loans of the Stuarts: the Crown did not ask permission to borrow; it demanded delivery, and the ‘debt’ was recorded after the fact as a political concession, not a financial prerequisite. Even the goldsmiths’ notes—private credit extended to the Crown—were denominated in units the Crown itself defined and enforced as lawful money. The gold in the goldsmiths’ vaults was a reserve, not a funding source.

Under the classical gold standard after 1821, the form changed but the logic did not. Bank of England notes were not ‘backed by’ gold in the sense that each note represented a specific coin in a vault. They were state issued tax credits, accepted in payment to the Exchequer, with an additional statutory promise: the Bank would convert them into gold at £3 17s 10½d per ounce. The tax foundation—the fiat requirement that private debts could be settled in notes—preceded and underwrote the gold promise. When the government spent, it issued new notes. When it ‘borrowed’, it issued a gilt—another fiat liability, distinguished only by its term and coupon. The gold reserve was a policy buffer, not a budgetary precondition. To call this ‘borrowing’ is to confuse the existence of a convertibility constraint with the absence of monetary sovereignty.

The persistent misreading arises from projecting private sector logic onto the state. A household cannot issue its own liabilities as final settlement; it must obtain someone else’s liability first. A monetarily sovereign state, even under gold, issues its own liability first and then, if it chooses, promises to exchange it for something else. That promise may bind the state’s policy options. It does not turn issuance into borrowing. The ‘National Debt’ was never debt in the household sense. It was always fiat—an added means of state provision, dressed in the language of thrift.

The Modern Monetary Architecture

The Bank of England as Sole Supplier of Central Bank Money

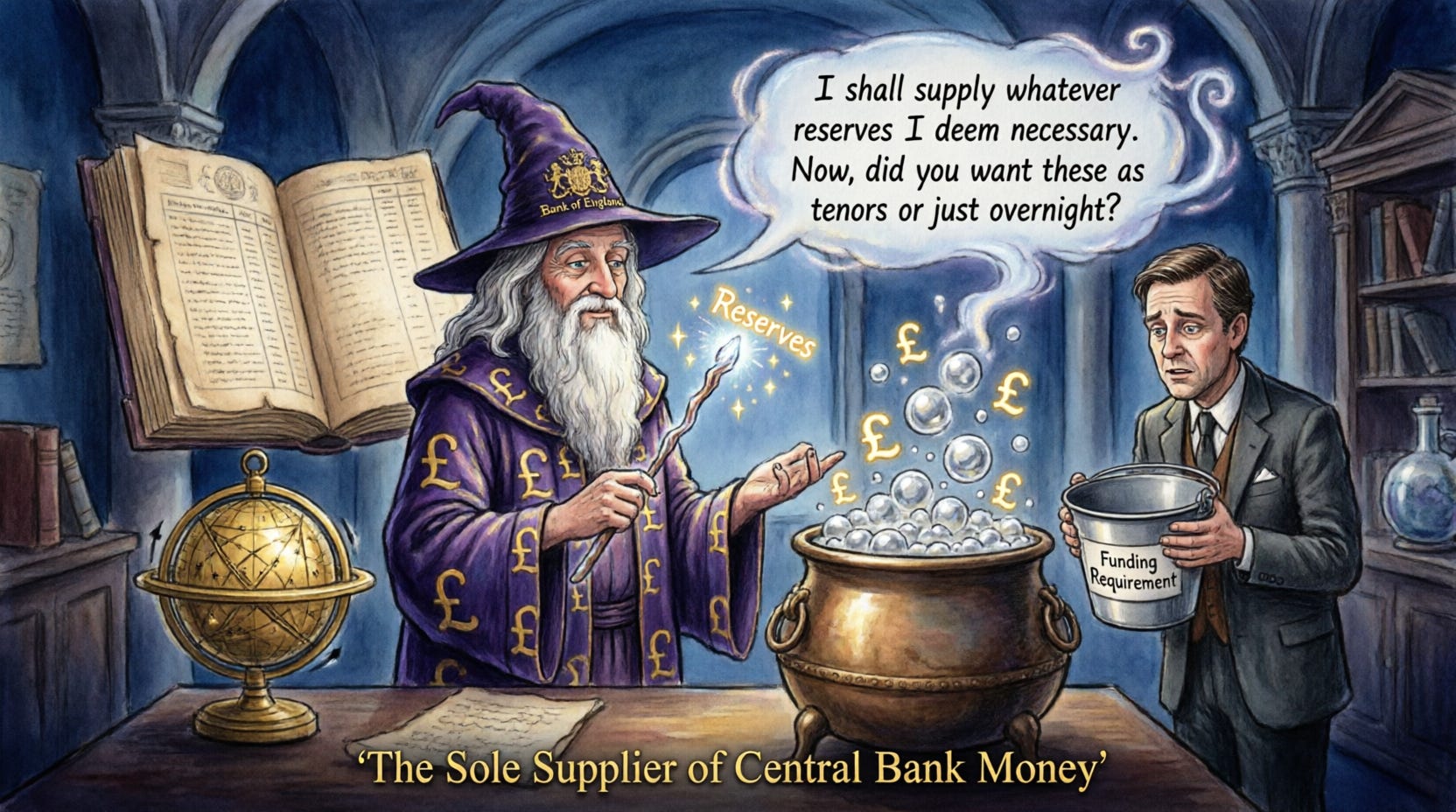

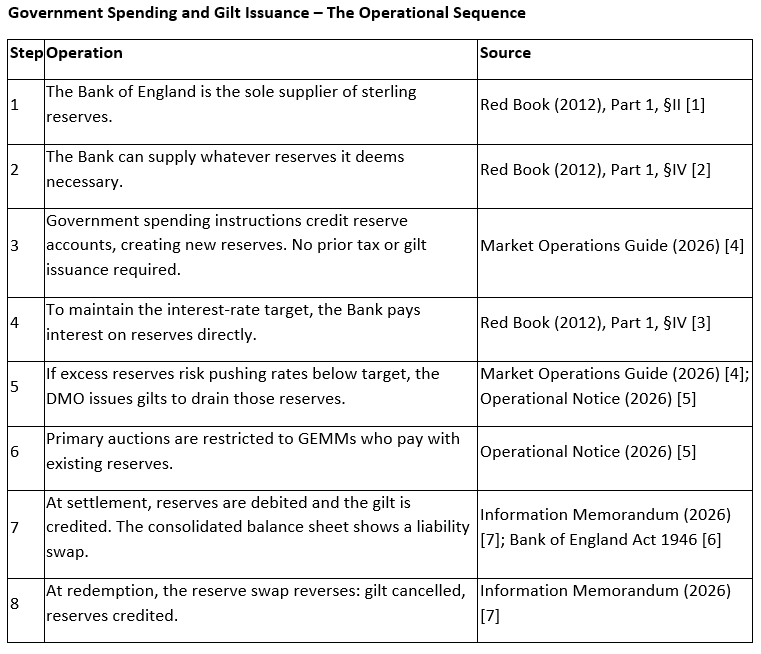

The operational reality of the modern sterling system is set out in the Bank of England’s own documentation. The Bank’s ‘Red Book’ (2012) states:

“The Bank is the sole supplier of ‘central bank money’ in the United Kingdom. Central bank money takes two forms — the banknotes used in everyday transactions and the balances (‘reserves’) that are held by commercial banks and building societies at the Bank.”

No private bank, no bond market, no external entity can create sterling reserves. When the government spends, it instructs the Bank to credit the reserve accounts of commercial banks. That spending creates new reserves. It does not require prior tax receipts or gilt sales. The Bank also confirms that it may

“supply whatever reserves it deems necessary to meet its monetary policy objectives.”

The Interest Rate Is a Policy Tool, Not a Market Constraint

The Bank implements monetary policy by paying interest on reserves, not by adjusting the quantity of reserves in the system. The Red Book states:

“The Bank usually does this by paying interest at Bank Rate on the reserve balances held by commercial banks.”

The overnight interest rate is set by the price the Bank pays on reserves, not by the volume of reserves outstanding. Draining reserves through gilt issuance is a secondary, optional operation to support this framework.

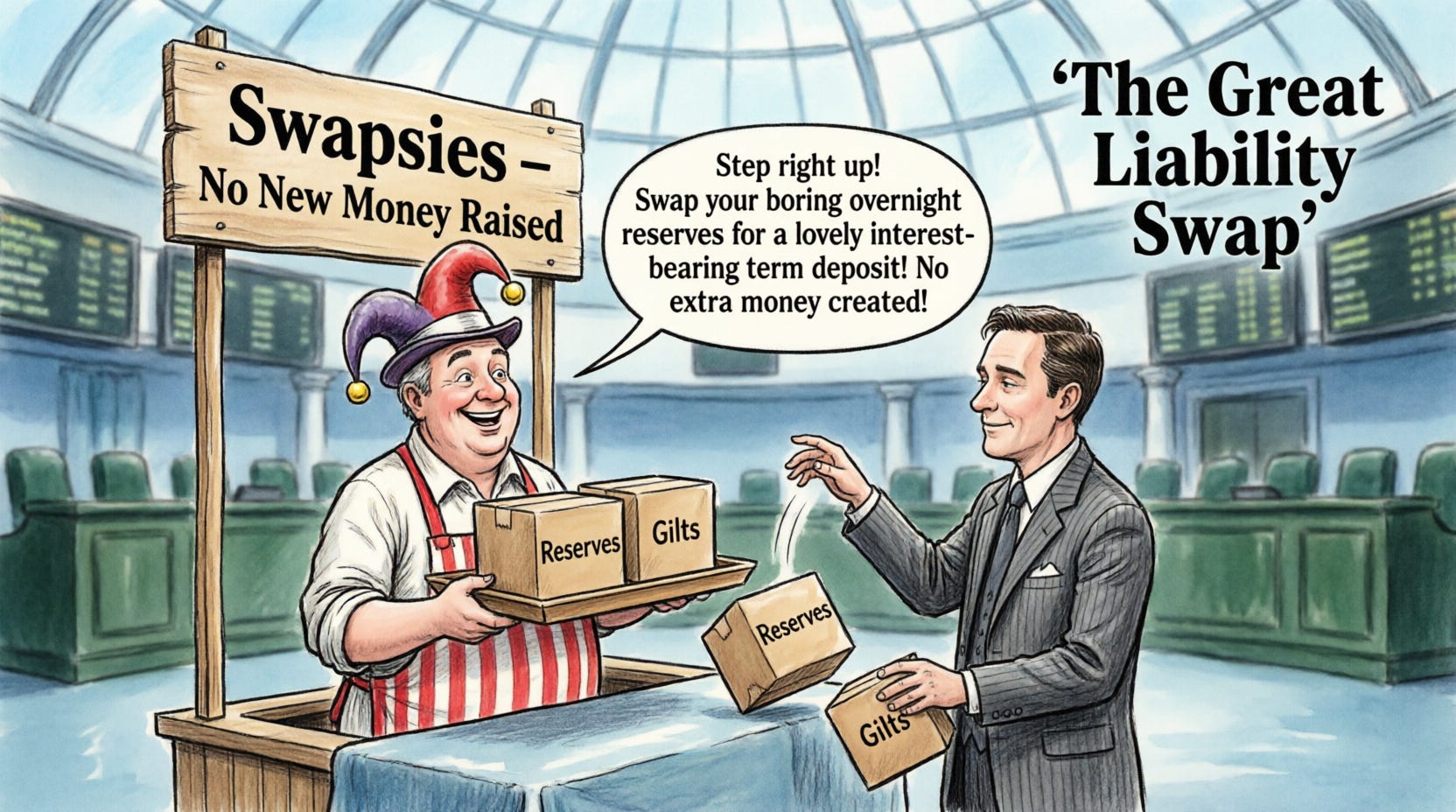

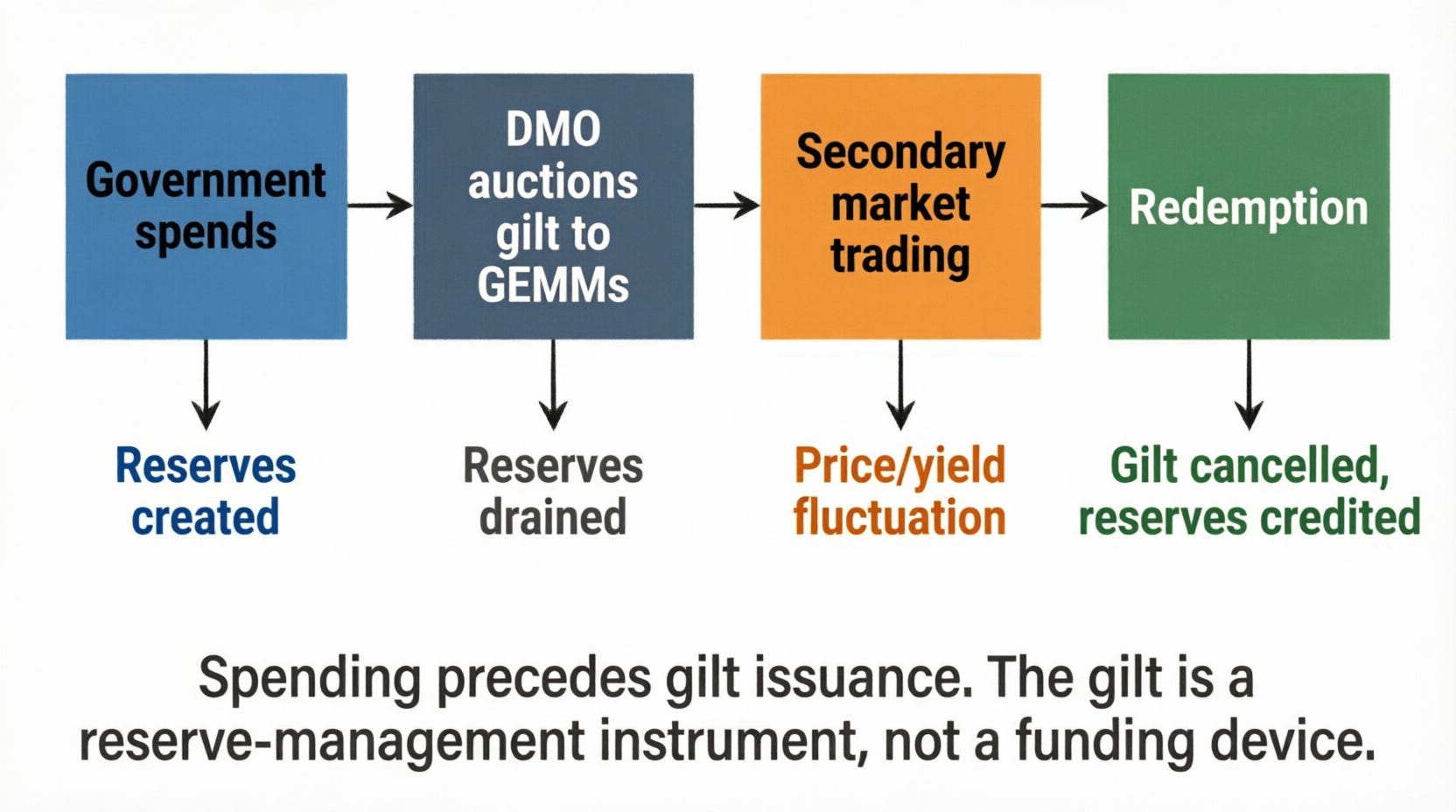

Gilt Issuance as a Reserve Management Operation

The Bank of England’s Market Operations Guide (2026) describes gilt operations explicitly as tools for controlling the supply of reserves:

“Our sterling market operations control the supply of reserves and play a central role in both implementing monetary policy and supporting financial stability. As part of successive policy interventions, the Bank significantly increased the total stock of reserves… Since then, the process of reserves expansion has reversed, and we have begun to reduce the stock of reserves.”

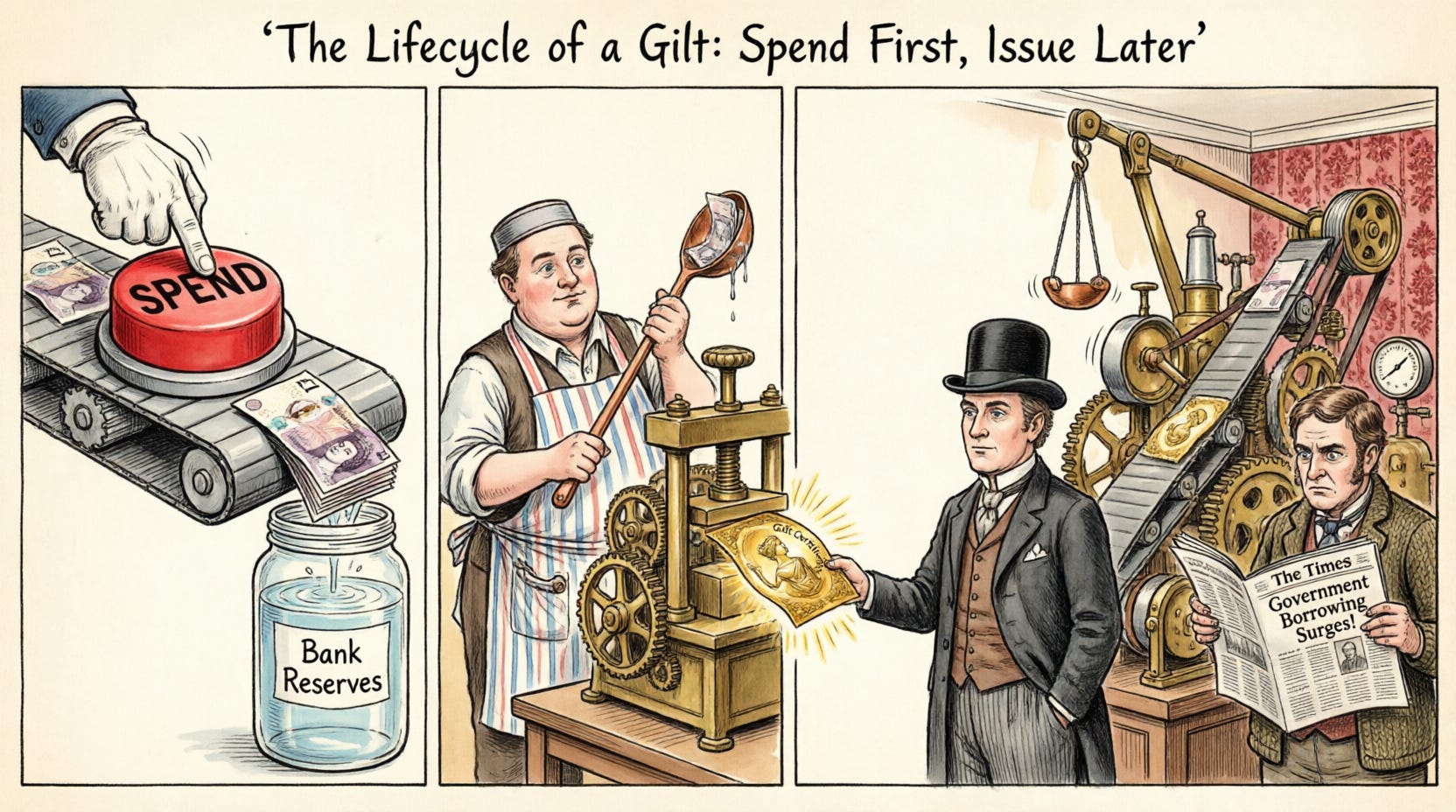

Quantitative easing created reserves and bought gilts. Quantitative tightening sells gilts and drains reserves. In both cases, the operation is a swap of one government liability for another. The spending that created the reserves occurred first.

The Debt Management Office’s own operational notice describes its role as

“the DMO’s main debt management activity.”

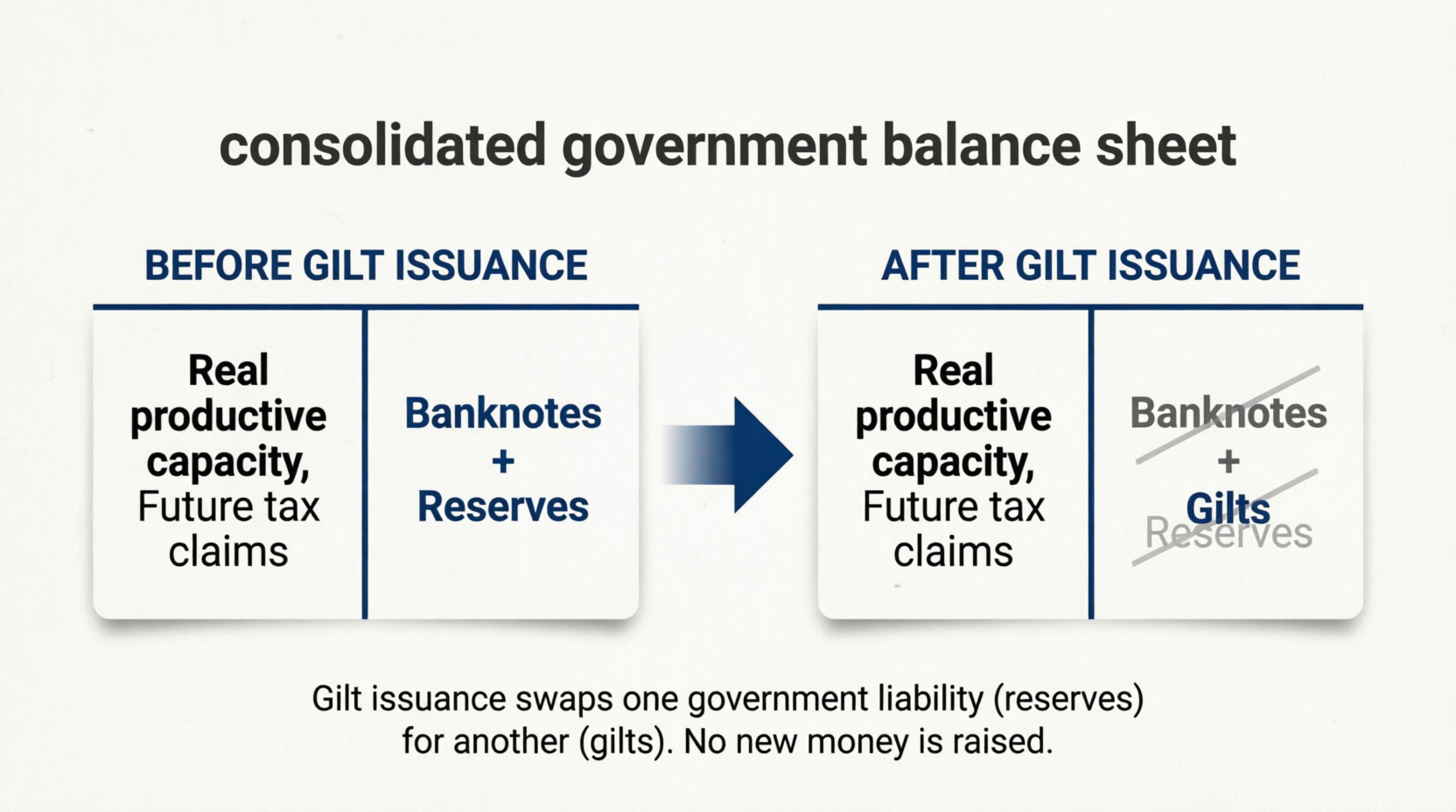

‘Debt management’ here means the management of the term structure of government liabilities—how much is in overnight reserves versus term bonds—not the act of obtaining spending power from external lenders. Only the 18 Gilt edged Market Makers (GEMMs), institutions that hold reserve accounts at the Bank, may bid at primary auctions. They pay with reserves the Bank itself created. At settlement, reserves are debited and the gilt is credited. The consolidated government balance sheet simply shows one liability replaced by another. No new money is raised. The government’s overall net position is unchanged.

The Legal Guarantee

A gilt is not a contingent claim dependent on market conditions. It is a direct statutory obligation. The Bank of England Act 1946, Schedule 1, states:

“The principal of and interest on the Government stock, and any expenses incurred in connection with the issue or redemption thereof, shall be charged on and issued out of the National Loans Fund with recourse to the Consolidated Fund of the United Kingdom.”

The DMO’s Information Memorandum (March 2026) repeats this guarantee for each issuance programme. [7] There is no intermediary risk. The obligation runs directly from the sovereign to the registered holder.

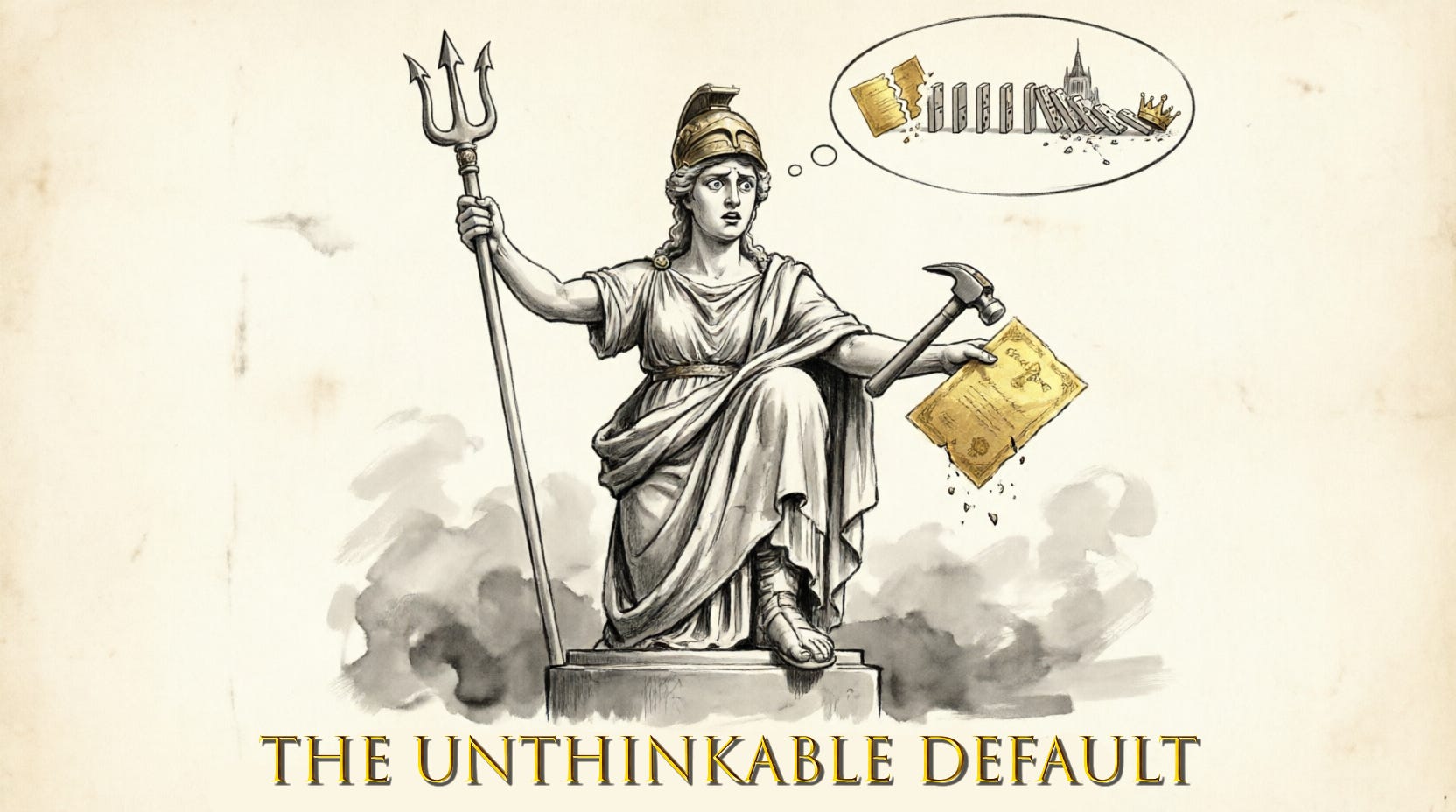

The Absolute Promise of No Default

If the UK government ever chose not to honour a gilt at redemption, that would be an act of deliberate self destruction. It would not be a market enforced event; it would be a voluntary decision by a sovereign that issues the very currency in which the obligation is payable. The entire sterling denominated financial system—pension fund liability matching, bank capital requirements, repo collateral, swap pricing—is built on the assumption that the sovereign’s promise is absolute. A default would vapourise that anchor. Sterling would cease to be accepted as the ultimate settlement medium. The payments system itself would be at risk.

This is why no monetarily sovereign government in modern history has ever defaulted on a domestic currency bond unless forced by a currency peg, a regime change, or a war that destroyed its institutional capacity. The constraint is not financial; it is existential. The bond vigilante fantasy—that ‘the market’ might force such a default—is exactly that: a fantasy. The market cannot force the issuer of sterling into a sterling default. Only the state itself can choose that.

The current ‘Bailey premium’ on gilts—the unnecessary elevation in yields caused by the Bank of England’s quantitative tightening and reserve draining operations—is a vivid illustration. The Bank is actively elevating borrowing costs for the Treasury, creating a multi billion pound fiscal drain, for no compelling operational reason. The policy is a choice, not an economic necessity.

The Operational Sequence in Summary

Table 1: Government Spending and Gilt Issuance – The Operational Sequence

Table 2: Historical Evolution of Sovereign Liability in England/Britain

Abandoning the Household Metaphor

The journey from the tally stick to the gilt edged bond is a story of institutional evolution, not of unchanged fiscal reality. The language of ‘borrowing’ is a relic of an era when the sovereign’s credit was indistinguishable from the monarch’s personal honour. The modern institutional architecture makes the sovereign’s promise absolute. Gilts are not debt in the household sense. They are a component of the UK’s monetary architecture—an interest bearing alternative to central bank reserves, a safe asset for private portfolios, and a variable over which the Bank of England exercises ultimate control.

The persistent framing of gilt yields as a state of national emergency is a political artefact. It serves to naturalise austerity, discipline the labour force, and protect the asset rich. The real danger is not rising yields; it is a public debate that mistakes a self inflicted cost for a tyrant. The Bank of England’s own manuals, the legal architecture of the Consolidated Fund, and 800 years of institutional history all tell the same story: the UK government is never a borrower of sterling. It is the issuer. The phantom of the bond vigilante is a ghost of the gold standard, and it is long past time to lay it to rest.

Bibliography

Bank of England (2012). The Framework for the Bank of England’s Operations in the Sterling Money Markets (the ‘Red Book’). Part 1, Section II. https://studyres.com/doc/14382620/

Bank of England (2012). Red Book. Part 1, Section IV, lines 37–42.

Bank of England (2012). Red Book. Part 1, Section IV, lines 36–39.

Bank of England (2026). Market Operations Guide: Our Objectives. https://www.bankofengland.co.uk/markets/bank-of-england-market-operations-guide/our-objectives

Debt Management Office (2026). Official Operations in the Gilt Market – An Operational Notice. 1 April 2026. https://www.dmo.gov.uk/media/1grjjk40/opnot010426.pdf

Bank of England Act 1946, Schedule 1. https://www.legislation.gov.uk/ukpga/1946/27/schedule/1

Debt Management Office (2026). Information Memorandum – Issue, Stripping and Reconstitution of British Government Stock. 10 March 2026. Page 3, Clause 3. https://www.dmo.gov.uk/media/zj2p0lab/infmemadd100326.pdf

Boy, N. (2015). ‘The Backstory of the Risk‑Free Asset: How Government Debt Became “Safe”.’ Journal of Cultural Economy, 8(3), pp. 292–309.

He, Z., Krishnamurthy, A., and Milbradt, K. (2016). ‘What Makes US Government Bonds Safe Assets?’ American Economic Review, 106(5), pp. 519–523.

Anand, K. and Gai, P. (2015). ‘The Safety of Government Debt.’ Journal of Financial Stability, 19, pp. 139–151.

Jiang, Z., Lustig, H., Van Nieuwerburgh, S., and Xiaolan, M. Z. (2026). ‘Manufacturing Risk‑Free Government Debt.’ Review of Financial Studies, forthcoming.

Bell, S. (2000). ‘Do Taxes and Bonds Finance Government Spending?’ Journal of Economic Issues, 34(3), pp. 603–620.

Fullwiler, S. T. (2016). ‘The Debt Ratio and Sustainable Macroeconomic Policy.’ World Economic Review, 7, pp. 12–42.

Kelton, S. (2020). The Deficit Myth: Modern Monetary Theory and How to Build a Better Economy. London: John Murray.

Mosler, W. (2010). The 7 Deadly Innocent Frauds of Economic Policy. Valance.

Wray, L. R. (2012). Modern Money Theory: A Primer on Macroeconomics for Sovereign Monetary Systems. Basingstoke: Palgrave Macmillan.

For More On Gilts and ‘Borrowing‘…

Secondary Gilt

What Is the Secondary Market?

The primary market does not “finance” spending that has already occurred.

Gilt Derivatives

The yield you see is not the yield you get (and why HM Treasury has no seat at this table)

Rehypothecation

A Tower of Risk

How the reuse of collateral creates hidden leverage, turns clients into unsecured creditors, and illustrates that HM Treasury has no seat in this shadow banking bazaar.